Source: Peter Epstein for Streetwise Reports 07/11/2018

Peter Epstein of Epstein Research speaks with the CEO of a lithium explorer that plans to release a PEA on its Nevada project soon.

The following interview of CEO Bill Willoughby, Phd, PE of Cypress Development Corp. (CYP:TSX.V; CYDVF:OTCQB; C1Z1:FSE) was conducted by phone and email over about a one week period ended July 11th. I’ve written several articles about this Epstein Research website sponsor—so far management has delivered on promises. In June, the company delivered a maiden lithium resource estimate of 3.3 Million tonnes (Mt) Lithium Carbonate Equivalent (LCE) in the NI 43-101 Indicated category, plus 2.9 Mt LCE Inferred.

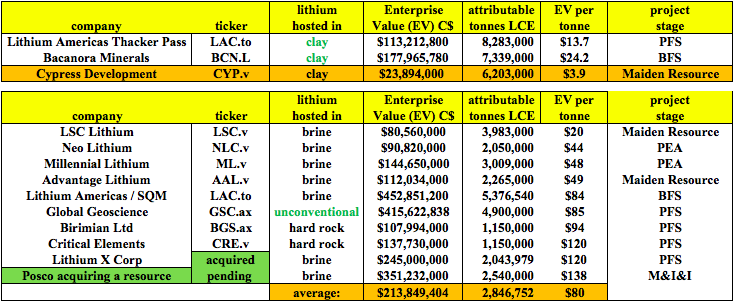

Cypress has the third largest lithium resource in North America, but the lithium is hosted in clay, and no clay-hosted lithium projects have reached commercial production. However, that’s very likely to change as Bacanora Minerals’ (BFS-stage) Sonora, Mexico, clay project is expected to start production in about two years and unconventional/clay projects owned by Global Geoscience and Lithium Americas, (both at PFS stage, both in Nevada), could commence production within three to four years.

Cypress is just weeks away from reporting key metrics of a PEA. Lithium Americas recently delivered key PFS metrics on its Thacker Pass clay project, including an after-tax NPV(8%) of ~C$3.4 billion and IRR of 29.3%. That’s based on a two-stage production ramp up reaching 60,000 tonnes per year LCE in 2026.

Cypress is contemplating less than 60,000 tonnes/year in its upcoming PEA, but if it can demonstrate attractive op-ex with relatively moderate cap-ex needs, a NPV well into the hundreds of millions of Canadian dollars seems likely. Compare that to Cypress Development’s market cap of ~C$22 million.

Without further preamble, here’s the exclusive interview with CEO Bill Willoughby.

There’s been a lot of good news at Cypress Development Corp., a maiden lithium resource estimate and rapid progress on a PEA (expected in next several weeks). Let’s start with the maiden resource; what are the key takeaways?

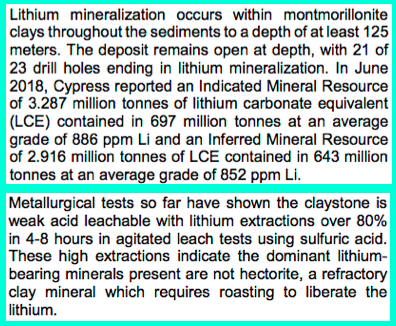

We have a very significant resource. It’s been a little over a year since Cypress started drilling and we have an NI 43-101 compliant Indicated resource of 697 Mt at 886 ppm lithium. This alone equates to 3.3 Mt Lithium Carbonate Equivalent (LCE). And, we have another 2.9 Mt LCE in the Inferred category, making our overall project (we believe) the third largest lithium resource in North America.

Most drill holes ended in mineralization, so additional drilling could grow the resource, and well placed holes could increase overall grade and improve the proportion of Indicated vs. Inferred tonnes.

The technical report shows what we’re calling a “preliminary pit,” where our consultants at GRE outlined nearly 200 Mt of clay around some of the higher-grade holes. So, it looks like there will be room in the PEA to optimize grade by selective mining.

In the chart below, a cut-off of 900 ppm Li generates an average Li grade of 1,126 ppm and ~36 years of production at 20,000 tonnes/yr. from the Indicated category only (i.e., not including Inferred). This gives us substantial tonnage as a starting point for our PEA.

A resource estimate by itself is not an economic study, but it does contain an economic basis in the form of a third-party (GRE) selected cut-off grade. The economic premise for our project depends upon metallurgy, and specifically that the lithium is in an acid-leachable clay. So far, we’ve done metallurgical bench tests on material from three drill holes, two of which are within the preliminary pit shell.

Tests show that lithium can be leached rapidly with relatively low acid consumption. If this were not the case, it’s doubtful we would be moving ahead at the pace we are.

While it’s exciting that a PEA is expected within weeks, what’s the rush to get it out? Aren’t there a number of open questions on metallurgy and the process flow sheet that need to be answered?

We see a good project and the steps ahead include more drilling and environmental studies. While we don’t need these steps to complete the PEA, we need the PEA to define the scope of the project so that we can keep it moving in these other areas.

As for metallurgy, we already have enough information in hand for the PEA. We know our flow sheet, which includes agitated tank leaching using sulfuric acid. We know our options on how to treat leach solutions and arrive at an end product, whether lithium carbonate or hydroxide. We know we have more work to do and questions to answer.

Cypress is sitting on a “clay-hosted lithium” project. There’s no meaningful lithium production anywhere in the world from clay. Why have clay-hosted projects been so difficult?

The process we are planning—agitated tank leaching—is quite conventional. We’re talking about lithium, which doesn’t have a long history in mining. The world’s very first lithium brine operation started just 50 years ago, and that was next to us in Clayton Valley, Nevada, at Albemarle Corp.’s Silver Peak.

It’s very true that clay-hosted deposits have been very difficult to exploit. The deposit you’re probably thinking about is Kings Valley, in northern Nevada. That deposit is very good grade but contains the clay mineral hectorite, which requires heating to high temperatures to leach the lithium. Until the recent rise in prices, the economics for a hectorite project weren’t there.

Lithium Americas, owner of Kings Valley, just in the last year announced a very large resource at Thacker Pass that is not hectorite and is acid leachable. A company working west of Silver Peak, Global Geoscience, is also pursuing acid leachable lithium at its unconventional deposit, Rhyolite Ridge.

As far as processing goes, the idea of acid leaching clay is quite common. For Clayton Valley we are …read more

From:: The Energy Report