By analyst

By Frik Els

Last week the price of lead spiked on the London Metal Exchange hitting the highest level since August 2011 at just over $2,600 a tonne.

The price of the metal used mainly in automobile and motorcycle batteries has since softened but is still trading up 27% year-to-date.

News from top producer and consumer China may provide further upside for lead. In a sign that already tight primary lead supply is getting tighter, Chinese smelters just lowered their treatment and refining charges to as much as half the average over the first half of 2017.

TC/RCs paid by mining companies to turn concentrate into metal are a good indication of conditions in the spot market. Platts News reports spot TCs for imported lead concentrates in China fell to $20–$30 per tonne in October down from $30–$40 in September.

According to metals consultants Beijing Antaike, TCs averaged $40.80 during the first six months of the year but compares to charges as high as $130–$150 per tonne in June 2016:

China’s mined lead demand is forecast to hit 3.478 million mt in 2017, up 12% year on year, with its mined lead output this year seen at 2.03 million mt, down from 2.23 million mt last year, due to domestic environmental controls, Antaike data showed.

China’s mined lead imports in 2017 are estimated to be 1.236 million mt, higher than 705,000 mt last year, with the domestic mined lead deficit seen at 211,000 mt this year, widening from deficit of 170,000 mt last year, Antaike said, noting that the above estimates did not consider the lead contained in imported zinc concentrates.

Reuters reports that deficits on the global lead market are narrowing however. In August the lead shortage shrunk to 4,600 tonnes from 31,900 tonnes in July, data from the Lisbon-based International Lead and Zinc Study Group showed on Wednesday.

For January to August, the lead market had an output deficit of 119,000 tonnes compared with a surplus of 49,000 tonnes in the same period last year.

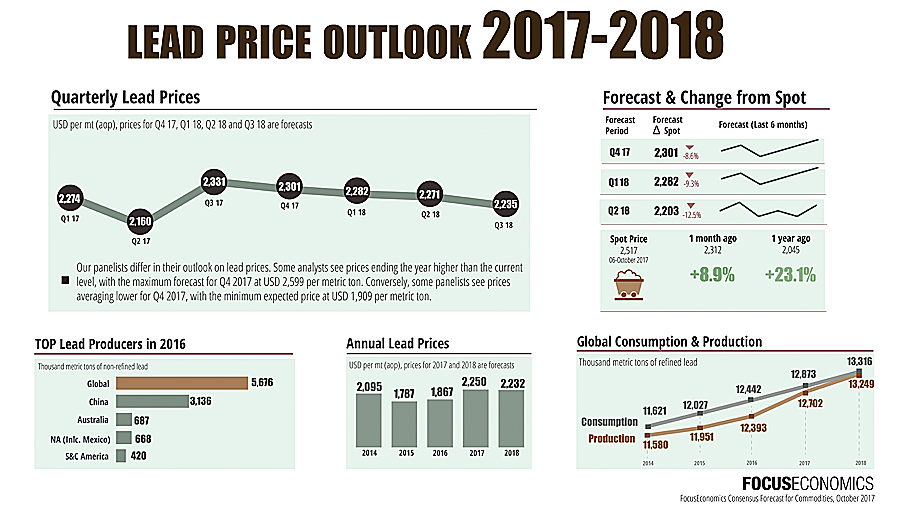

Analysts polled for October’s FocusEconomics Consensus Forecast estimate that the lead price will average just over $2,300 per tonne during the final quarter of this year and moderate further through 2018.

This month, six panelists left their forecasts for lead unchanged for Q4 2017, three made downward revisions while eight raised their forecasts.

Macquarie analysts are the most bullish – predicting price to average $2,600 this quarter and add another $50 through the first half of 2018. Deutsche Bank considers lead overpriced at the moment and forecasts the metal to dip below $2,000 in H2 2018.

The post More good news for lead price as market tightens further appeared first on MINING.com.

Source:: Infomine

The post More good news for lead price as market tightens further appeared first on Junior Mining Analyst.