By Zach Scheidt

This post 550 Credit Score, A New Mustang, And A Collapsing Economy appeared first on Daily Reckoning.

“Last week, we put a driver into a brand new Mustang. He had a 550 credit score and we got him zero percent financing!”

That’s the story I heard on the radio yesterday afternoon as I took my daughter to cheer practice.

The commercial kicked off a great conversation with Rebekah about debt, interest rates, credit scores, and how our economy works.

Unfortunately, my explanation got us both thinking about just how dangerous debt levels have become, and how many consumers and savers will suffer because of the level of debt in our nation…

Debt and the U.S. Economy

To say that debt fuels the American economy would be the understatement of the century.

Corporations borrow vast sums of money to fund their businesses. Sometimes the debt is put to good use and helps to grow profits. And sometimes that debt becomes an insurmountable challenge in which interest expense erodes profits and causes companies to declare bankruptcy.

Individual Americans are hardly any better.

We borrow money to fund just about any expense.

From college educations, to home purchases…

From refrigerators to big screen TVs…

We finance vacations and remodel projects…

Don’t forget about your car loan (or multiple car loans for the 2 or 3 car garage)

Even clothes, groceries and frivolous purchases are paid for with credit cards… Cards that may or may not be paid off at the end of the month. And of course those cards typically carry hefty interest rates that eat away at what we could be spending next year at this time.

And all of this debt pales in comparison to the $19.9 trillion (and counting) in debt carried by the U.S. government. That’s more than $165,000 worth of debt for every single taxpayer!1

Yes, the United States economy now rests heavily on a foundation of debt. And this level of debt has enormous implications for investors who want to grow and protect their wealth for retirement.

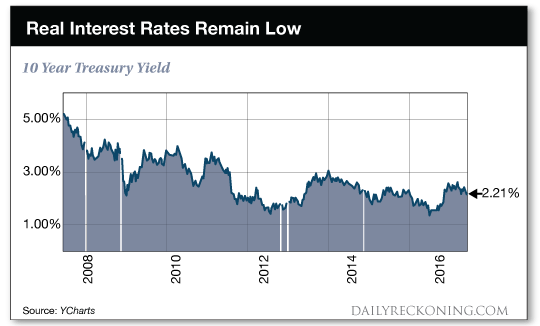

Why the Fed Can’t (and Won’t) Aggressively Hike Interest Rates

My debt conversation with Rebekah was particularly timely because of the Fed interest rate decision this week.

As you’ve probably heard, the Federal Open Market Committee has been holding its regularly scheduled meeting this week. Today at 2:00, the Fed will release its statement on target interest rates, and Chairman Janet Yellen will follow the statement with a press briefing.

Investors and economists have priced in a near 100% chance that the Fed will increase its target interest rate to a range of 1.00% to 1.25%.

CNBC commentators, Wall Street Journal authors, and plenty of other “talking heads” have been telling investors what to expect in this era of “rising interest rates.”

Well, I’m here to tell you that these commentators are dead wrong.

We’re actually NOT in an era of rising interest rates, and we will NOT be seeing materially higher rates any time soon. Perhaps not in my lifetime — and maybe not even in my children’s lifetime.

That’s because interest rates cannot rise without causing tremendous damage …read more

Source:: Daily Reckoning feed

The post 550 Credit Score, A New Mustang, And A Collapsing Economy appeared first on Junior Mining Analyst.