![]()

Collin Kettell

Palisades Goldcorp Ltd.

collin@palisades.ca

A Crash Course in Junior Mining – what mining and technology share in common

Last week I spoke about the impending junior mining mania that will soon unfold. This move will be violent, extreme, and in many cases, the gains produced will be life changing.

This week I want to explore how the junior sector operates and how it fits into the overall commodity puzzle. In order to do so, I will draw a direct analogy to the tech space. These two sectors independently represent the two most volatile markets in the world and surprisingly have a lot in common.

Let’s start with tech. In tech, there are a handful of companies that produce a majority of the sector’s profits and represent the lion’s share of the sector’s market capitalization. Think of Google ($GOOG), Apple ($APPL), Amazon ($AMZN), Microsoft ($MSFT), and Facebook ($FB) – the Giants.

Next down the totem pole are companies that operate on solid cash flow, but lack conglomerate status. They are less known and ultimately serve as unsuspecting lunch should one of the top dogs get hungry to acquire.

Further down still are the start-ups – companies built to solve a specific problem. Some of them are known, but generally they are obscure and most fail to produce anything that gains market traction or longevity.

Start-ups serve an indispensable function in the technology space. They feed innovative concepts and ideas that change the world. Almost every technological revolution stems from a start-up. They begin as an idea in the mind of an inventor, but ultimately become capital intensive and rarely generate profit until maturation. The potential monetary prize of these inventions, platforms, or apps is exponential and thus warrants serious attention from the Giants.

The technology ecosystem was not designed like this, but has naturally evolved this way due to market forces. Tech Goliaths like Facebook and Google are constantly investing in R&D, but they simply cannot justify allocating the resources to create 2,000 startups in hopes of finding one gem. And even if they did, start-ups are organic concepts – a result of an inventor solving a problem they often times personally encountered.

For these reasons, tech giants are forced to sit back and watch with a checkbook in hand. When a start-up emerges that they deem to be critically important, they are willing to pay massive premiums to acquire that technology. Think of Google buying YouTube or Facebook’s purchase of Instagram. In both cases, these acquisitions cost $1B and were thought ludicrous at the time due to a lack of profit. They now contribute as massive profit centers for both companies. Investors trying to value technology start-ups on cash flow, or lack thereof, possess a fundamental misunderstanding of the sector.

There is of course the rare case where a start-up makes it through the maturation phase on its own. Facebook was famously offered $1B by Yahoo, but declined the offer. Uber ($UBER) has not had a credible takeout offer and is now public, but a sustainable cash flowing model has yet to be demonstrated.

Moving to mining, there similarly exist a handful of companies that make up the majority of production and lion’s share of the sector’s market capitalization – Barrick ($GOLD), Newmont ($NEM), Zijin, Kirkland Lake ($KL.TO) are some of the names that come to mind. These are the Majors, analogous to the Giants of technology.

A Major’s core competency rests in mining gold from the ground. They do occasionally perform grass roots exploration, but for the most part, are focused on development and extraction. A Major’s share price acts as a direct lever to the underlying commodity. Higher gold prices equate to better operating margins, and translate into a higher share price.

A bit further down the ladder are the mid-tier producers. They effectively perform the same duty as the Majors, but on a smaller scale and as witnessed time and time again, they are lunch for a hungry Major. Last week’s acquisition of Detour Gold ($DGC.TO) by Kirkland Lake is a prime example.

At the bottom of the hierarchical pyramid are the juniors, loosely defined as companies with less than a $250M market cap (often times below $10M). Juniors are focused on exploring for the mines of tomorrow.

These companies are the lifeblood of the mining business – without them there would be no ounces to replace the depleting reserves at operating gold mines. Just like technology start-ups, most of them fail. As the saying goes, 1-in-3,000 targets becomes a viable deposit. Ultimately those are pretty bad odds and why the majority of juniors fail. It is also why most Majors cannot justify grass roots exploration – it would bankrupt their operations.

For argument’s sake, a 1-in-3,000 success rate might be applicable to not just the juniors, but also tech startups. Success in achieving that pinnacle of discovery (or market relevance in the case of tech) will translate into serious profit for investors.

But, aside from market/discovery success, there is a force at play that is equally as important and that is the cycle itself. In technology today, the start-up ecosystem is robust. Across the board, companies have access to capital on terms that are not terribly dilutive. This has led to the ‘unicorn’ nomenclature, reminiscent of the dot-com bubble in 1999.

During the dot-com bubble, money rushed into the sector without prudence or precision. The value of tech companies rose in tandem regardless of quality, and investors made a fortune. This created an epic market bubble. The sector overcapitalized, capital was misallocated, and the market ultimately burst. It took a few years to come back, but money did ultimately return. The next cycle peak occurred in 2008. Today, tech appears once again in the euphoric portion of the cycle.

Mining is even more predictably cyclical. Following the Bre-X scandal in 1996, mining began a precipitous decline. The tides turned in 2000 and began an eleven-year bull market (minus the 2008 crash). Then in 2011 the mining market shifted into bear market territory, steered by the underlying commodity prices. In 2016, as a reaction to extremely depressed prices, the mining stocks rallied. Today, they remain depressed. But, positive indicators have emerged such as a rally in commodity prices, matched by moves in the Majors.

I cannot stress enough how important this cyclicality is to the ecosystems for both technology and mining. In a speculative market where valuations of companies are not based on profit, but instead derived from anticipation of future results, extreme cycles will always exist. When a lack of solutions are being invented to aid in technological issues, money will eventually pour in to fix this. When a lack of ounces exists in reserve in the gold market, money will ultimately rush in.

Conversely, when technology start-ups reach ‘unicorn’ valuations across the board, it only takes one WeWork moment to scare investors away – a not so subtle reminder that the risk they are taking on no longer can be met with the asymmetrical gains their capital deserves.

In mining, when an abundance of ounces are put into reserves due to discoveries and higher commodity prices, investors will achieve smaller returns for taking on greater risks. Major mining companies begin to overpay for ounces. The value of all juniors reaches extreme heights. And at some point, investors shy away.

Differences between technology and mining do, of course, exist. And they are valuable to examine in the context of this discussion as well.

I once asked a well-known industry titan why someone with such a sharp mind would subject himself to the junior sector? Why not venture into oil & gas for example? He responded that competition is a lot lighter when you are scraping along the bottom of the junior mining barrel. Harsh words – but not far removed from the truth.

People often times lament the junior mining sector with its inefficiencies and lack of intellectual capital. But there is good reason for this phenomenon and it is not going to change anytime soon – 1) the size of monetary reward and 2) the lack of predictability.

In technology, the prize for a successful start-up can directly translate into a $10B or $20B cash take out. This can happen in a very short period of time – a couple years. Facebook bought WhatsApp for $19B in stock and cash with only 55 employees on staff and five years into operation. Ownership of technology companies tend to remain quite concentrated in the hands of the founders, meaning the prize is really, really big.

In mining, it is rare for a discovery to yield over $1B on a takeout. $10B is unheard of. These acquisitions happen a couple times per cycle, not a couple times per month like in tech. Furthermore, the mining business is far more capital intensive in context of the value created in the market and therefore the founders receive a much smaller slice. Money owns the mining exploration space, not the geologists.

All this translates into smaller monetary rewards. Since money attracts talent, it is no wonder intellectual capital concentrates in technology rather than mining. Geologists can spend a lifetime in search of a discovery to call their own; when they find it, they rarely own enough to build serious wealth.

The second point is regarding a lack of predictability. In the start-up world, guessing what is going to be successful and what will not is no easy task. But there are venture capitalists out there that demonstrate an ability to pick the right horse time and time again – Peter Thiel, Andreessen Horowitz, etc. In mining, this is almost non- existent. Robert Friedland has had two multibillion-dollar discoveries to his name. He is the only person alive with such good luck. For those who will debate me on this point, I will further clarify that he is the only person to ever do it and remain the majority shareholder.

The reason for this is that mining is a game of odds. You have to buy enough lottery tickets to get a winning hand. If you ever wonder why billionaire Eric Sprott invests in hundreds of companies, it is not for lack of discipline. He understands the game innately. First, he takes educated guesses, planting seeds with the right teams and right projects. Then when the sniff of a discovery comes along, he is first in line to deploy as much as he can. Wallbridge Mining ($WM.TO) is a textbook example.

This is the only systematic way to play the discovery game and why Eric is bound to go from billionaire to multi-billionaire status when the next cycle hits.

Conversely, technology requires concentrated bets. Typical venture capitalists in Silicon Valley make very educated bets and will deploy into just a dozen companies over a few years period. This ability to predict the next tech success with some level of accuracy attracts intellectual capital away from an unpredictable sector like exploration and towards the world of tech. This fundamental difference in concentration of bets and associated risks is why technology start-ups exist in the private space, while mining is almost exclusively in the public sphere.

The bottom line is technology and mining are capital intensive and they require a constant flow of new ideas and new reserves. Without the start-ups and without the juniors, the ecosystem is broken.

The relevance of a technological innovation depletes over time in the face of new ideas, different needs, and faster processing capabilities. A mining project’s lifespan depletes very literally as every ounce mined is one less left in the ground.

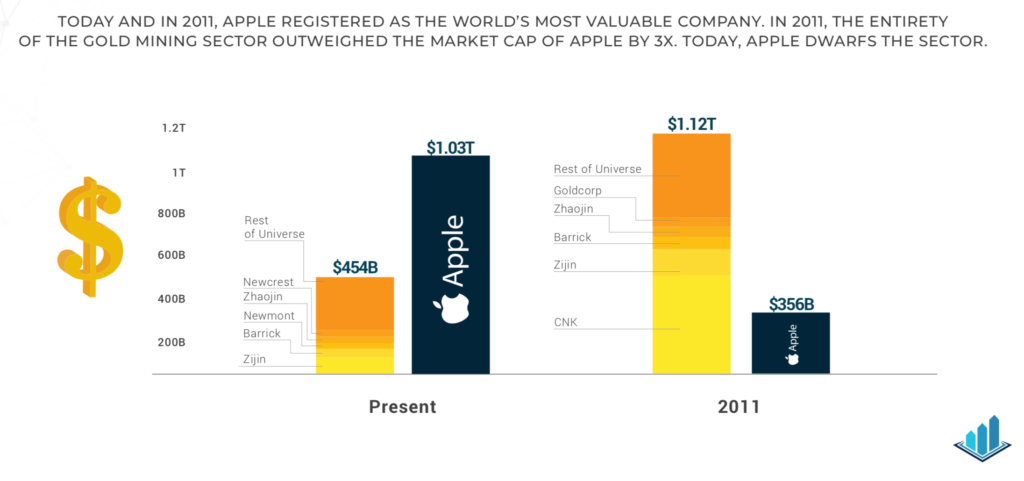

These two sectors – tech start-ups and junior miners – lack traditional methods of valuation that are based on cash flow. And for that reason, cycles will always exist to reflect human nature – too much capital, too little capital, but always in search of a balance. Ironically, both sectors are currently out of whack. Mining is experiencing a lack of capital while technology is facing the opposite problem – too much money can result in an imprudent idea like WeWork being given a $40B valuation. The below graphic nicely depicts the discrepancy in relative valuations between the two sectors.

This is why I said last week that in some way, shape, or form, an impending junior mining mania is coming and it is going to be exactly the same this time!

Until next week,

Collin Kettell

Founder & Executive Chairman

Palisades Goldcorp Ltd.