Golden Arrow Resources Sells 25% Interest in Puna Operations to SSR Mining for $44.4M

Source: The Critical Investor for Streetwise Reports 07/29/2019

The Critical Investor looks beyond the headlines to analyze the factors behind the company’s sale of its JV share to its partner.

Golden Arrow Resources Corp. (GRG:TSX.V; GARWF:OTCQB; G6A:FSE) surprised the markets with its sale of its 25% interest in Puna Operations to majority JV partner SSR Mining Inc. (SSRM:NASDAQ), right at a time where precious metals seemed to have left a bear market behind them. The Puna operation just ramped up to full production a quarter ago, and it seemed only a matter of time for high opex to come down, as a new mine always has to fine tune things. When costs would have been normalized, Puna could finally start to bring in cash for Golden Arrow, to finance its exploration efforts. It never got that far, unfortunately.

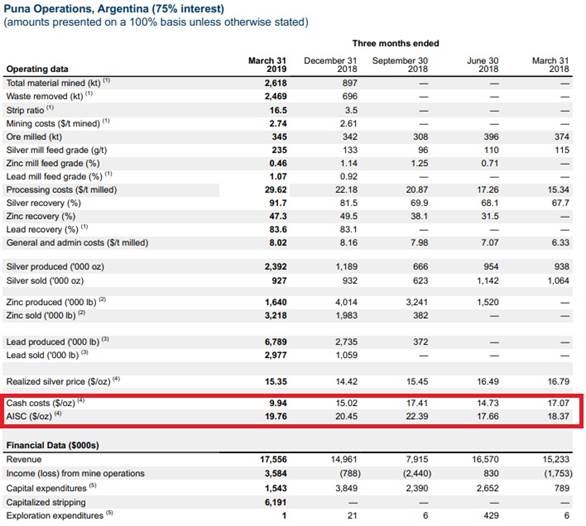

Instead of the pre-feasibility study (PFS) opex of US$9.75/oz Ag, cash costs were hovering around the price of silver itself for a long time (US$14–17/oz Ag), and last quarter (first quarter of commercial production) the All-In Sustaining Costs (AISC) even went beyond that (US$19.76/oz Ag) despite cash cost coming down to US$9.94/oz Ag. These high costs led to an operation making losses, and SSR Mining didn’t hesitate to make cash calls to Golden Arrow, to pay up for its share of losses. This was something I didn’t anticipate, more on this later. First of all, let’s have a look at the deal. These are the highlights per the news release of July 22:

- “C$3.0 million in cash consideration

- C$25.9 million in common shares of SSR Mining

- Approximately C$14.5 million in cash, which amount shall be used to repay in full at closing the outstanding principal and accrued interest owing by Golden Arrow under the credit agreement entered into in July 2018 with SSR Mining

- C$1.0 million through the return for cancellation, for no consideration, of 4,285,714 Golden Arrow common shares currently owned by SSR Mining, which represents approximately 3.4% of Golden Arrow’s issued and outstanding common shares on the date hereof

Payment by SSR Mining of Golden Arrow’s portion of all cash contributions required to be made to Puna Operations under the Shareholders Agreement from July 22, 2019 until the closing date.”

In the end it means that Golden Arrow receives C$3 million in cash and C$25.9 million in common shares of SSR Mining, in total C$28.9 million. Golden Arrow management seemed quite pleased by it:

“The sale of our equity position in Puna Operations is a landmark achievement for the Company. The Transaction allows Golden Arrow to maintain diversified low-risk exposure to the continued success of SSR Mining at Puna Operations in Argentina and across their gold-focused producing portfolio in North America,” stated Joseph Grosso, executive chairman, president and CEO of Golden Arrow. “The Transaction provides Golden Arrow with a strengthened financial position to focus on delivering shareholder returns through the exploration and development of our exciting exploration portfolio in South America.”

Of course, this transaction removes a heavy burden of repayment terms for Golden Arrow, gets a decent package of SSR Mining shares with a lot of exposure to gold; it won’t have to go to the markets anytime soon now, and will be able to focus on its exploration assets now. All good. But there are more sides to this story, and not at least the factors that sent the share price crashing pretty hard after the news came out on July 22, more on this later:

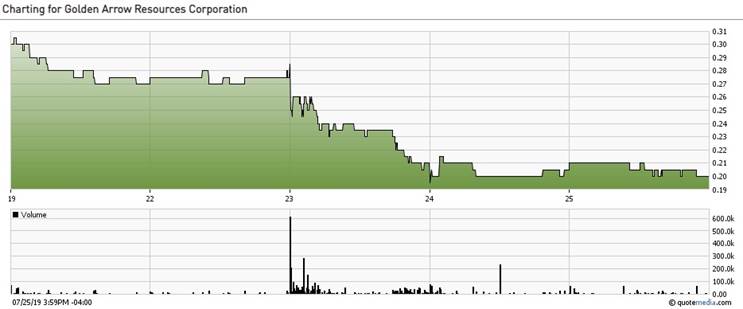

Share price; time frame 5 days

Besides this, just as remarkable was the sudden run-up from July 16 (C$0.205) to July 18 (C$0.30) on large volume, which doesn’t really indicate a tight ship as they say. However, whoever bought these shares, they did so on unrealistic expectations as the news of the transaction was apparently used to host a massive liquidity event.

There were some more transaction details:

“SSR Mining has agreed to loan (the “Contribution Loan”) to Golden Arrow the amount required to fund Golden Arrow’s portion of any cash calls under the shareholders agreement for Puna Operations made as of May 31, 2017 between SSR Mining and Golden Arrow, as amended by an amendment to the shareholders agreement made effective as of April 1, 2019 (as amended, the “Shareholders Agreement”) for the period from July 22, 2019 to the earlier of (i) the closing date of the Transaction and (ii) the termination of Agreement. Upon closing of the Transaction SSR Mining will provide Golden Arrow with an amount of cash sufficient for Golden Arrow to repay the Contribution Loans in full.

“However, if the Agreement is terminated prior to closing, such Contribution Loans shall be due and payable by Golden Arrow within twenty five (25) calendar days of such termination. The Contribution Loans are secured by a pledge of Golden Arrow’s shareholding interest in Puna Operations. The Agreement may be terminated for, among other things, (i) a material breach by Golden Arrow of its representations and covenants under the Agreement; or (ii) if the Transaction is not completed by October 15, 2019, or (iii) if Golden Arrow accepts a superior proposal.”

It sure is in the best interest of Golden Arrow to close this agreement, as in any other event it needs to repay the loans within 25 days, and these loans are secured by the 25% holding position of Golden Arrow in the Puna operation. As the company tried very hard to arrange a refinancing of the $10 million credit facility but failed, this effectively and most likely will mean that Golden Arrow just has to hand over their interest to SSR, unless a suitor pays off SSR.

“The Transaction is subject to the approval of two third of the votes cast in person or by proxy at a special meeting of the Golden Arrow shareholders and Golden Arrow shareholders shall be entitled to statutory dissent rights in respect of such vote. The Transaction also requires approval of Golden Arrow shareholders under the policies of the TSXV, as the Transaction represents the sale of more than 50% of Golden Arrow’s assets. Each director and officer of Golden Arrow and their associates and affiliates have each entered into voting agreements with SSR Mining pursuant to which they have agreed, among other things, to vote their respective shares in Golden Arrow in favour of the Transaction at the Golden Arrow shareholder meeting.

“Approximately 10.6% of Golden Arrow’s common shares are subject to these voting agreements. In addition, SSR Mining has indicated that it will vote the Golden Arrow common shares it holds in favour of the Transaction, representing an additional 3.4% of the issued and outstanding Golden Arrow common shares. It is expected that Golden Arrow will prepare and mail a meeting circular to its shareholders within 30 days, and that the special meeting of shareholders will be held by mid-September. The Transaction is subject to a number of customary conditions including the approval of Golden Arrow shareholders and the approval of the TSX Venture Exchange.”

So mid-September will be the moment of truth. Keep in mind that a lot of current shareholders weren’t too happy with proceedings and sold, so it wouldn’t surprise me if there are still a significant number of unhappy shareholders. And of course, their hired financial advisor PI Financial thinks this transaction is “fair,” otherwise they would miss their fees:

“The board of directors of Golden Arrow has determined that the Transaction is fair to the shareholders of Golden Arrow and in the best interests of Golden Arrow. The board of directors of Golden Arrow have received a fairness opinion from its financial advisor, PI Financial Corp., as to the fairness of the Transaction from a financial point of view to the shareholders of Golden Arrow, other than SSR Mining, which opinion was based on and subject to the assumptions made, matters considered and limitations and qualifications on the review undertaken.

“The Agreement provides for among other things, a non-solicitation covenant on the part of Golden Arrow (subject to customary fiduciary out provisions). The Agreement also provides SSR Mining with a right to match any competing offer which constitutes a superior proposal. A termination payment of US$1.36 million will be payable to SSR Mining in certain circumstances.”

This reminds me, I didn’t see a break fee for SSR Mining mentioned anywhere, which would be about 10–15% of the transaction fee of $44.4 million. But buying the remaining 25% makes a lot of sense for SSR Mining (I always wondered why it didn’t do it in the beginning) so I guess that would be the reason. As SSR Mining is more and more gearing toward being a gold producer (it calls it precious metals producer), I don’t rule out the possibility that it would like to sell Chinchillas/Puna now it has consolidated it to 100% ownership.

A thing I found pretty remarkable here were the cash calls of SSR Mining to its minority nanocap junior JV partner, knowing this company didn’t have an exactly full treasury. As a result, Golden Arrow Resources surprised the market with another raise in June, as consensus was that the earlier C$4.74 million financing would be enough to carry the company through most of 2019. C$1.2 million was raised at 20 cents with a full 3 year warrant (exercise price 30 cents), oversubscribed (from C$750,000), and closed at June 20, 2019.

As I was curious why management decided to do so, I contacted them at the time to find out. It appeared that the JV with SSR Mining was organized in such a way that Golden Arrow Resources had to participate in the losses as well, and since the Q1 AISC came in again at US$19.76/oz Ag when silver was selling around US$15/oz Ag, it was beginning to dawn on me where the cash call from SSR came from (table from the Q1 MD&A of SSR Mining):

The Q1 financials (p. 12) describe this in a summarized way (POI means Puna Operations Inc.), and key here was of course “capital expenditures and working capital purposes”:

“On March 31, 2017, SSRM exercised its option on the Chinchillas project and on May 31, 2017, SSRM and the Company formed POI for the development of the property. The jointly owned company, holding the Pirquitas and Chinchillas properties is owned 75% by SSRM and 25% by the Company with SSRM as the operator. The Company is liable for contribution of 25% of the required funding for capital expenditures and working capital purposes of POI when requested by POI.”

My earlier understanding was that capital expenditures in this agreement only meant initial capex, to build the mine, and not sustaining capital expenditures or losses on the operation.

According to the MD&A (Management Discussions and Analysis), these were the highlights of Q1, taken from the financials of SSR Mining:

“Highlights of Puna’s first quarter 2019 production and financial results as reported by SSRM included:

- Produced 2.4 million ounces of silver, double the silver production in the fourth quarter of 2018, with lead and zinc production of 6.8 million pounds and 1.6 million pounds, respectively.

- Processed ore in the first quarter of 2019 contained an average silver grade of 235 g/t.

- Silver recoveries quoted at 91.7%

- Ramp up at the Chinchillas mine was substantially completed during the quarter.

- Doubled silver production with lower costs at Puna Operations.”

These are, of course, the highlights, so I looked at the reporting of SSR Mining itself to get the whole picture.

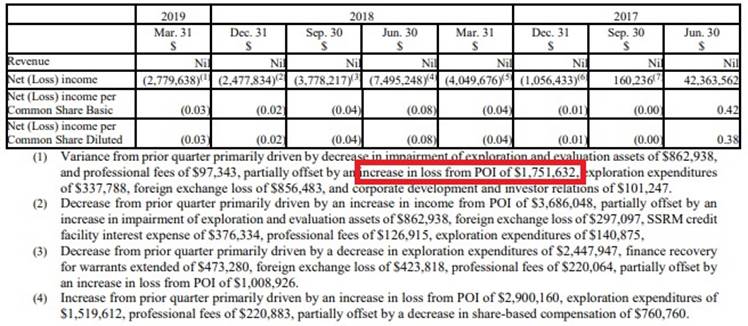

And there it is, the unintended loss at commercial production.

Back to the MD&A of Golden Arrow:

“The Company’s continued operations, as intended, are dependent upon its ability to raise additional funding to meet its obligations and commitments and to attain profitable operations. Management’s plan in this regard is to raise equity financing as required to further fund its share of planned capital expenditures for its investment in POI and working capital. Management’s plan in this regard is to raise additional funding as required.”

These cash calls came at the end of each quarter, to the tune of $1-2 million. Of course this is an unsustainable situation for a small junior like Golden Arrow.

What I found even more strange were the high opex numbers produced by SSR Mining as the operator, and one with a very good reputation to go with that as well. These numbers deviated from the PFS numbers by 50–100%, way higher than the usual margin of error in a PFS (although 35% as used is pretty high for a PFS, usually it is 25%, and 35% is more for a PEA). Therefore I contacted management again, for some answers on this topic.

According to them, SSR thought this situation of high costs would last well into 2020, meaning Golden Arrow had to raise C$1–2 million each quarter. This was the primary reason for Golden Arrow to sell its 25% interest, as the needed cap raises were almost undoable, also with the repayment of the US$10 million credit facility coming up in a year. The company tried very hard to refinance this facility, and looked at all other options, but with no luck being a minority JV partner, very dependent on SSR Mining as the operator who came up with a year of high opex from now.

These opex overruns revolved primarily around the stripping costs, where SSR Mining had to strip much more than planned. There were also heavy rains and severe lightning, causing problems for hauling ore to Pirquitas. Especially the stripping issue got my attention, and more specifically the extent of the resulting higher opex because of it. For answers on this issue, I got redirected to a director of Golden Arrow Resources, Alf Hills, who also sits on the BoD of Puna Operations Inc. for Golden Arrow. We had an interesting conversation.

Alf pointed out that the main difference in costs appeared to be in Processing, as reported in the SSR Mining Q1 news release, since these almost doubled compared to the PFS figures for Q1, stripping, however, wasn’t out of the ordinary as it was planned to be (very) high the first commercial quarters in the PFS.

It all seems to revolve around the AISC here. Point is the PFS isn’t providing AISC figures per production year, just a LOM average, so it is hard for me to reverse engineer this number. When looking at PFS table 16.3, the stripping for Y2Q1 (Y2 is 2019) and Y2Q2 is indeed very high (16.51 and 14.42) but also as planned, but coming down fast in Y2Q3 and further (5.90, 4.32, 3.75, 5.7).

When looking at silver production (as mentioned AISC is net of byproducts no need to use AgEq figures here) for the first year (2019) and more specifically the quarters, I get for Y2Q1 a silver production of 478 Koz, Y2Q2 of 436 Koz, Y2Q3 of 1.22 Moz, Y2Q4 of 1.8 Moz.

When I look at table 21.1, sustaining capital seems to be geared mostly toward mining equipment, mining support equipment, freight, contingency, and just $5.25 million (LOM) is reserved for Other sustaining capital cost. Note 3 states that sustaining capital is exclusive of capitalized stripping, so I don’t see how stripping costs could attribute to the AISC as much as management thought it does. Table 22.4 shows Sustaining capex of $15 million over Y2 (or 1 in this particular table), this means $15 million / 3.93 Moz Ag = $3.8/oz Ag sustaining cost on average for Y2, but I have no clue what the sustaining costs per quarter in Y2 would be, or even better the AISC per quarter.

More importantly, I don’t see how the stripping deviates from the PFS, and Alf agrees on this.

It seems all planned and clear to me from the start, so it seems GRG and SSR must have been aware when commercial production started at these low silver prices, they were already at increased risk of these cash calls, as without the processing cost increase, basically nothing could go wrong just to break even.

Of course, the silver price is significantly lower than what was assumed in the PFS. However, when the AISC goes over the assumed PFS silver price anyway, it doesn’t matter anymore, you lose money. According to the PFS, stripping costs should come down a lot. However, it is hard to draw conclusions on AISC as there is no info on this, just bits and reverse engineered pieces, and even more important, why does SSR say the AISC would remain high for another year? Will the processing problems (I would like to call double processing costs a problem) not be solved in a year?

Alf couldn’t elaborate on these high processing costs: “As I mentioned I don’t have visibility on the high processing cost reported by SSR Mining in its Q1 News Release, and suspect it has some legacy components to it. To my knowledge the mill did not have any material operating issues in Q1.”

As a result, on-going cash calls from the operation, the maturity date of the SSRM loan (this was July 2020 but with no payback schedule), low silver price compared to the PFS base case, and on-going challenging funding environment for junior companies were all substantial considerations for the company to sell its 25% interest, according to him.

To me it all seemed like a risky operation, to start production at this lower silver price. Everything had to go right as the margins weren’t substantial to begin with at US$19.50/oz Ag base case. Alf had the following comment: “I think it is fair to say the project was committed on the basis of the results of the Technical report—the low silver price environment means the margins are squeezed even more. 2019 was seen and reported by SSRM as a transition year from project to routine operation and that is generally in line with what was planned in the PFS.”

Another detail Alf found is the fact that SSR produced more ounces in Q1 than it sold. He finds the reason for the high AISC/oz largely due to the use of ounces sold rather than produced, and this is a decision SSR Mining as the operator and majority owner has made.Over time, SSR will sell these stockpiled ounces for sure, and figures will even out. But I can’t imagine this being a reason for GRG to sell, as it is just a temporary thing.

According to management, they had a much more simple motivation to all this: “The main reason to sell now is because we have a buyer now.”

But this doesn’t tell the whole story of course.

So whatever the reason and the trajectory was, it appeared that Golden Arrow was with its back against the wall, and simply had to accept the offer of SSR Mining, at a time precious metals sentiment was turning unfortunately. Who would have thought this a few years ago, certainly not me. In my mind I still find it remarkable to see a non cash flowing junior being partly responsible for potential losses of a ramping up operation, operated by a majority JV partner. An important thing to consider is the fact there are no bonuses to be paid to Golden Arrow management this time, contrary to the sale of the first 75%.

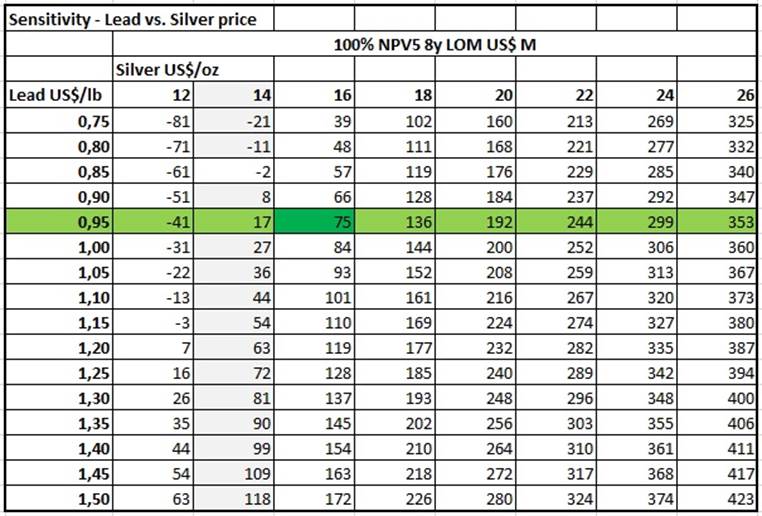

If C$44.4 million is a good price for Chinchillas/25% of Puna Operations is a good question. With silver at US$16.42, and lead at US$0.94, the sensitivity I calculated in my first article comes up with an estimated 100% NPV5 of about US$89 million:

When divided by 4, the 25% ownership of Golden Arrow attributes to US$22.25 millin, which is C$29 million. The 25% ownership of the Pirquitas plant break up value could be estimated at C$11.5 million midpoint based on the estimate I did in my first article. Usually this value is included in the NPV5, but since the NPV5 is so low because of metal prices being very low, I view it as fair to assign separate value to it. This brings the total value of the 25% interest in Puna Operations at a globally estimated C$40.5 million, which isn’t too far off from the C$44.4 million transaction fee. I can live with it, but remember SSR Mining buys it right at the time silver prices are cautiously following gold in its footsteps. There is no question in my mind SSR Mining hardly pays any premium for potential upside here, whether it is a longer mine life or a rising silver price or both.

Golden Arrow management is very pleased with the transaction, as it was their only way out of upcoming financial obligations, and sees the significant package of SSR shares as solid exposure to gold, which is doing well nowadays. Silver is still lagging, but has got a pulse. I have a slightly different view, to me this means the end of Golden Arrow as one of the best leveraged plays on silver in the entire industry. The beauty was it was a one producing asset pure play on silver, supported and operated by a very good operator, and hovering a long time around break even or small losses. Ideal for a leveraged play as the effect of a rising silver price would be optimal. And even better, with incoming cash flow it could self-fund its exploration ventures without having to go back to the markets, and get the upside here as a wild card. Unfortunately, all this was not to be. It appears many investors were invested in Golden Arrow for the same reason, as the share price lost 24% in one day on big volume (about 20 times normal volume) after announcing the transaction.

If the transaction gets approved, which could mean a challenge if the silver price rises substantially before the upcoming special AGM in September, Golden Arrow is no longer a producer, but a pure explorer again. It will have substantial current assets, to the tune of C$29 million (current market cap is C$25 million) with a lot of exposure to a very solid producer with lots of gold exposure, a few exploration assets, and is actively looking for new assets at the moment. Management indicated to me there will be significant news coming in a few weeks’ time, so my guess is they found something interesting in this regard, which will undoubtedly help them by creating a new direction.

Conclusion

Considering the financial hardship Golden Arrow was in, the selling of its 25% was the only realistic option after management did everything they could to avoid this, but I didn’t know the situation was this dire, and would be relatively long lasting, intensifying financial risks. Lessons learned in analyzing JV structures, and minority partners are not to be envied, this much is clear again from this development. It will be interesting to see which new asset(s) Golden Arrow will find in order to cement its soon to be newfound role as a pure-play explorer. Chances are the company will focus on quality gold assets this time around, as gold seems to be a better market proposition. I am curious to find out, with the kind of compensation it will get from SSR, the company should potentially be able to buy very good assets, possibly with significant historical, potentially economically viable deposits. But I am totally speculating now, of course. Let’s wait and see, to be continued.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu to get an email notice of my new articles soon after they are published.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

The Critical Investor Disclaimer:

The author is not a registered investment advisor, currently has a long position in this stock, and Golden Arrow Resources is a sponsoring company. All facts are to be checked by the reader. For more information go to www.goldenarrowresources.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor’s disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Golden Arrow Resources, a company mentioned in this article.

Charts and graphics provided by the author.

( Companies Mentioned: GRG:TSX.V; GARWF:OTCQB; G6A:FSE,

)

Golden Arrow Resources Sells 25% Interest in Puna Operations to SSR Mining for $44.4M Read More »