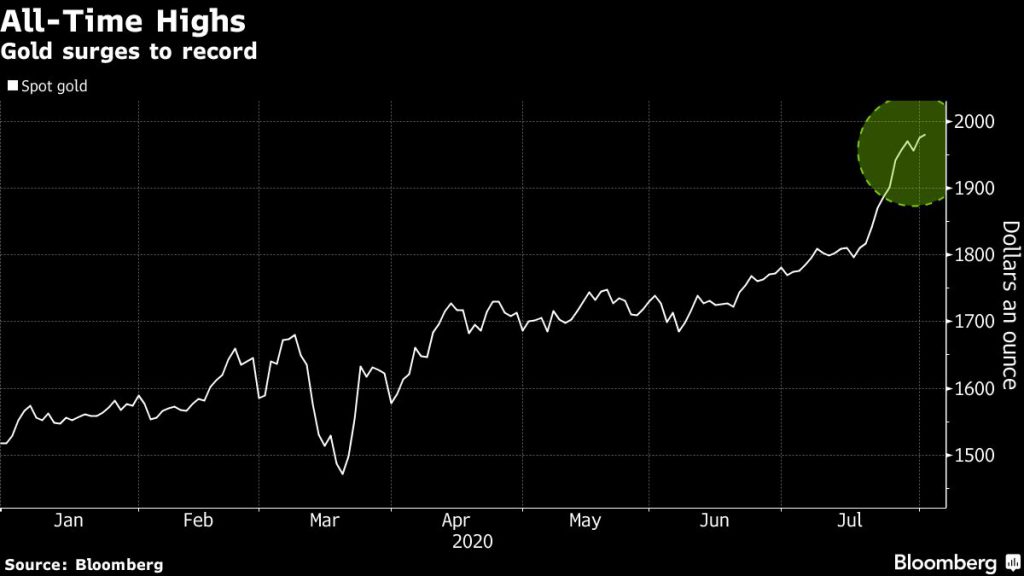

Gold prices retreated from a record high on Monday as US and European equities rose on positive economic data and the dollar climbed. However, concerns over rising coronavirus cases and its impact on the global economy still remain, limiting bullion’s losses.

Spot gold fell 0.4% to $1,967.97 per ounce by noon EDT, after reaching an intraday high of $1,984.70 per ounce. Gold futures edged 0.5% higher at $1,986.90 an ounce on the Comex in New York.

“Over the past two weeks we’ve had such a climb in gold, it’s going up so fast that you’re going to see people wanting to digest or take some profits,” Michael Matousek, head trader at U.S. Global Investors, told Reuters, adding that a rising dollar was also weighing on prices.

“We have definitely seen a loss of momentum over the past several sessions where only modest, even marginal new highs are being made, which has likely driven shorter-term players to take some profit and trade it, rather than simply holding long positions,” said Tai Wong, head of metals derivatives trading at BMO Capital Markets. “It suggests a deeper albeit still modest correction is possible.”

While the rally appeared to pause, analysts who say gold is overvalued are not expecting a substantial decline. A correction probably will be measured, thanks to the weak dollar and chronic turmoil in the global economy, BNP Paribas SA said in a note.

Bullion has surged about 30% so far this year, supported by lower interest rates and widespread stimulus measures by global central banks to ease the economic blow from the pandemic.

“We see a lot of people anticipating once that (stimulus) comes out, more bids will come into gold,” Matousek said.

(With files from Bloomberg and Reuters)