Building resilience is the top priority for the mining and metals industry in H2 2020, while market weakness is the top risk, a survey conducted by global law firm White & Case with 67 senior decision-makers revealed.

The 2020s are set to be a serious transition period for the mining industry, they say.

After two decades of supercharged Chinese growth and omnipresent concerns about a global slowdown, other issues, such as resource nationalism and trade pressures, compliance and ESG considerations are taking center stage for investors and throughout the value chain.

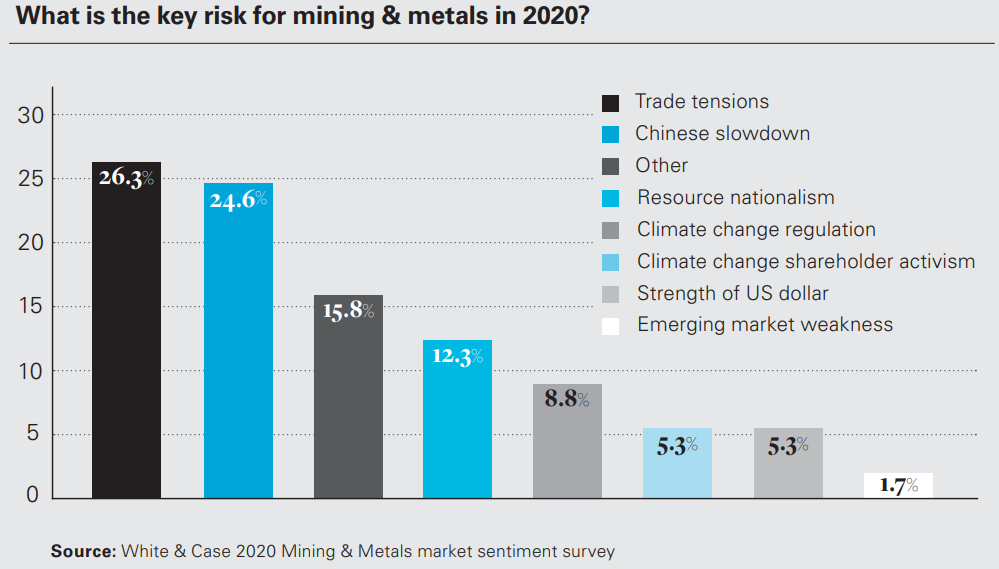

While 39% of those surveyed cite global market weakness as the key risk in Q3 and Q4 2020, trade tensions—which had been deemed the biggest risk in January after US and Chinese governments signed a preliminary deal — has dropped from 26% to 5%.

Supply chain disruptions are seen as a key risk for the sector by 16% of the respondents

Respondents expect tensions to drag as the two countries worked their way through a “phase two” deal in an election year.

A similar decline was seen in the proportion of those selecting a slowdown in the Chinese economy—consumer of about half of the world’s commodities—as the biggest risk. Just 5% see this as the biggest concern, down from 24% in January, and even higher in 2019, when it polled as the biggest risk.

Supply chain disruptions are seen as key risk for the sector by 16% of the respondents and commodity prices by 14%.

Majors

The big diversified miners entered 2020 in the best shape they’ve been in for many years. While the pandemic was obviously an unexpected shock, the industry had better prepared balance sheets and recent experience to lean on in a way many other sectors did not.

As soon as covid-19 spread globally, several mines around the world were forced to slow or temporarily close as governments sought to contain the spread of the virus. The top ones, Rio Tinto and BHP, announced plans to review or lower capital spending, halting development projects to maximize cash, while Glencore reduced its capex forecast for the year by up to $1.5 billion.

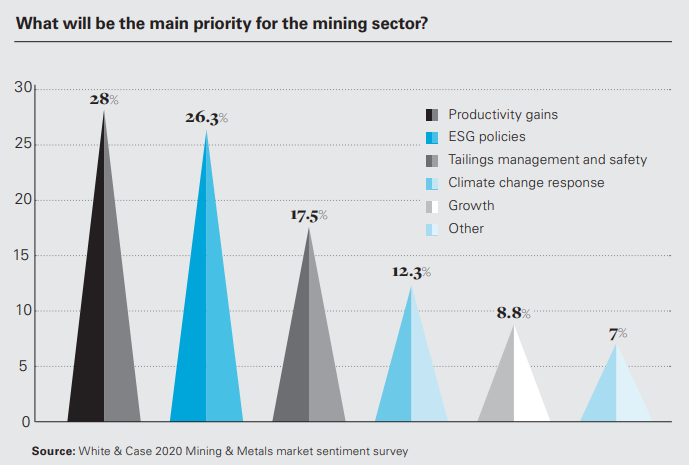

“These actions mirror the thoughts of our respondents, with more than a quarter stating that building resilience would be the main priority for the sector in the second half, with efficiencies second at 18%.

ESG

Of the surveyed, 14% expect improved ESG performance to lure generalist investors to allocate capital to the sector, up from 9% in January. The majority (80%) think ESG will play a greater part in investors’ decision making, too.

It is clear that although shareholder returns are clearly crucial to attracting investors, ESG remains an important driver

White and Case

“Yet, 65% expect long-term sustainability initiatives to conflict with the need to cut costs, and this is borne out in the questions discussed above, with responses considering ESG to be a main priority for the sector, halving from 26% to 13%,” White & Case reports.

Just 2% think shareholder activism is a key risk this year, down from 13% in January.

In addition, 22% of respondents to the survey see ESG as a means of building greater resilience for the future, second only to supply chain excellence.

Survey also shows exposure to the battery minerals supply chain is expected to be a significant factor, doubling from January to 18% in June.

Resource nationalism

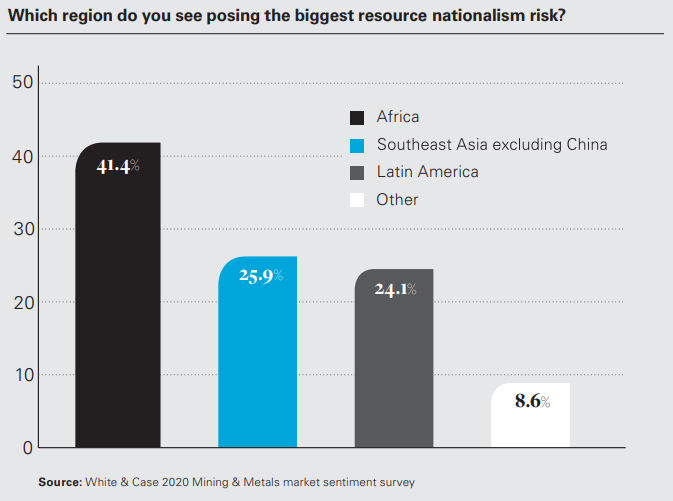

The survey shows that Africa is the hotspot for resource nationalism, with half of respondents expecting the continent to account for the most action, up from 44% in January.

Almost half of respondents see increased taxation as the way resource nationalism is most likely to manifest itself in the wake of covid-19.

Big deals

Mega M&A deals will be few and far between and opportunities are expected to involve distress situations, according to the survey.

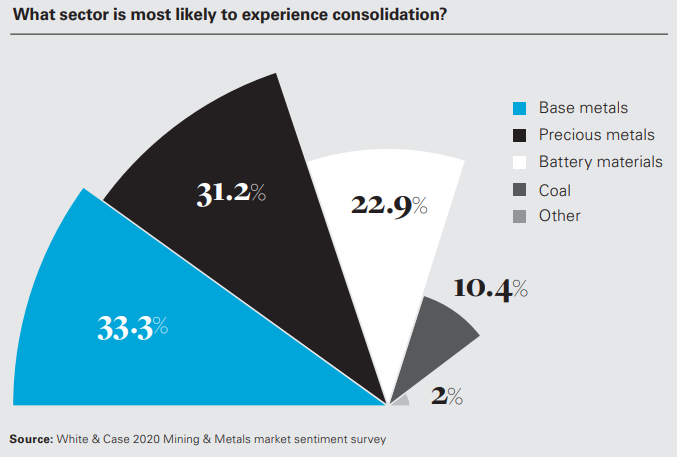

“Precious metals is where our respondents think activity is most likely, attracting 49% of the vote, up from 30% at the start of the year. Notably, base metals has declined to six percent from 33%, with battery minerals rising one place into second.”

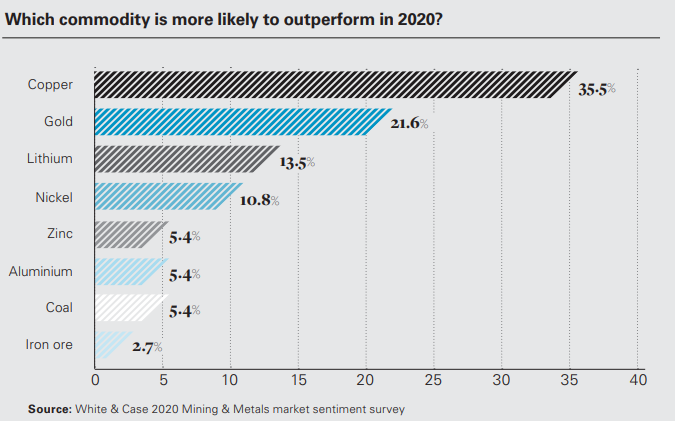

The positive sentiment surrounding base and precious metals is also reflected when it comes to picking the metals expected to perform best this year, with 35% saying copper and 21% choosing gold.

It’s a different story for battery materials after another difficult year: while 13% expect lithium to be a standout performer in 2020, no respondents chose cobalt.

Battery material markets remained under sustained pressure in 2019, as the full scale of new production capacities dawned on the market.

Cobalt plummeted to $30,000 a ton after almost reaching $100,000 a ton at its peak in mid- 2018.

Technology

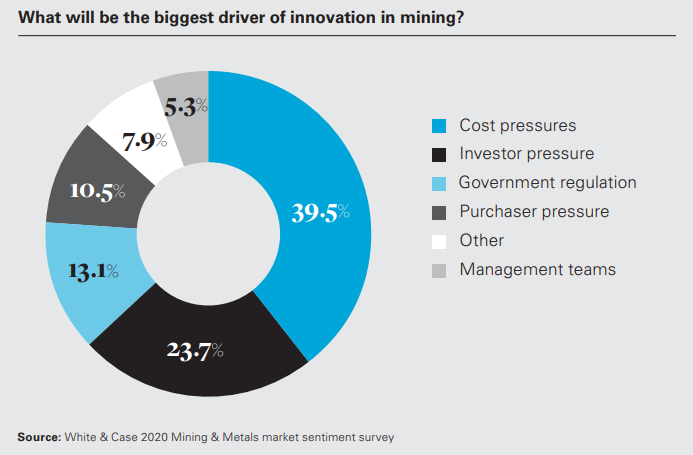

All major miners are increasing the spend and rollout of data analytics to improve their mining and exploration activities. White & Case’s survey suggests this will continue, with cost pressures being the biggest driver for innovation for a second straight year.

The survey highlights that the experts are still split on how blockchain will be best implemented, but ultimately its use in managing supply chains and logistics had the most support, with an increased share from the previous year.