Source: Peter Epstein for Streetwise Reports 04/23/2020

Peter Epstein of Epstein Research discusses the macro picture for precious metals prices and one junior who he believes will benefit from higher prices.

Timing is everything. Precious metals are up when almost everything else is down. Gold has soared 38% from last year’s low. This is a big move, but few investors seem to appreciate its significance. Earlier this week, Bank of America announced a gold price target of US$3,000/oz by the end of 2021. While that might sound too aggressive, today’s price of US$1,740/oz. = ~C$2,463/oz. is already quite strong.

The current price is more than enough for well managed juniors, with attractive projects, in safe and prolific jurisdictions, to thrive. Right now, some of the best precious metal jurisdictions, as measured by low-costs plus ample exploration upside, include parts of Mexico, Canada and Australia.

In an April 13, 2020, Myrmikan Research investment letter, manager Daniel Oliver made strong arguments that gold and silver prices are headed higher, perhaps much, much higher. Mr. Oliver has been published in Forbes, The Wall Street Journal, The Washington Times, Real Clear Markets, National Review, among others. He has a J.D. from Columbia Law School and an MBA from INSEAD.

Most important for the purposes of this article, Oliver is a director of tiny silver-gold junior Vangold Resources Ltd. (VGLD:TSX.V; VGLDF:OTCQB). {corporate presentation} In his commentary, he unveils three potential paths or scenarios for precious metals.

In the first scenario,

“…the magnitude of the dollar debt overhang is so large—tens of trillions—that policy makers cannot practically prevent the inverted credit pyramid from tipping over. The result is a panic more intense by magnitudes than 2008 or 1929. Gold does well on a relative basis, but falls in nominal terms.”

In the second scenario,

“….trillions of dollars does little to help local businesses and the working class. Wall Street, however, is not just saved, but levers up bailout largess to create spectacular increases in asset prices. Gold spikes in nominal terms as it did from 2009 to 2011 under similar conditions. Gold mining equities soar….”

Finally, in the third scenario,

“….the Fed’s helicopter drop of dollars precipitates a currency crisis. Gold bullion rockets toward $10,000 per ounce. Gold miners (especially marginal, higher risk players) have breath-taking increases, last experienced from 1978 to 1981.”

Oliver believes the first scenario is by far least likely to unfold, an end-of-the-world type of event that we need not focus on because the world would be over…. The remaining two paths are bullish, and extremely bullish, respectively for physical gold and silver and precious metals juniors.

Make no mistake, just because Dan Oliver and a growing cadre of investment experts are talking up precious metals doesn’t guarantee the price will shoot to the moon or even rise from current levels. However, giant hedge, mutual and generalist funds are looking closely at precious metals and the companies that explore for, develop and mine them.

Relative value funds have plenty of industry sectors to avoid, but only a few that offer potential upside combined with low correlation to, and diversification from, the overall market. Glowing reports of precious metals’ fabulous future are a lot more palatable given that a tsunami of global debt obligations will be issued, with no end in sight.

As bad, or perhaps even worse, is governments’ willingness, in a blink of an eye, to direct their central banks to print absurd amounts of money out of thin air. Combined, debt plus unfunded and under-funded liabilities will explode much higher. Not by tens or hundreds of billions, but by trillions of dollars. It’s no longer just a theory (ongoing unbelievably large and unsustainable debt), the pandemic has made it a certainty.

Vangold Mining has many positive attributes. Its 100%-owned silver-gold project is in a safe and desirable location in central Mexico, the state of Guanajuato. At its peak in the 18th century, the mines of Guanajuato, especially the world famous Valenciana mine, were considered the largest and richest on the planet. In the 50 years from 1760 to 1810, Guanajuato (mostly from Valenciana) often accounted for 20% of global silver production, primarily from a single extraordinarily rich vein. {corporate presentation}

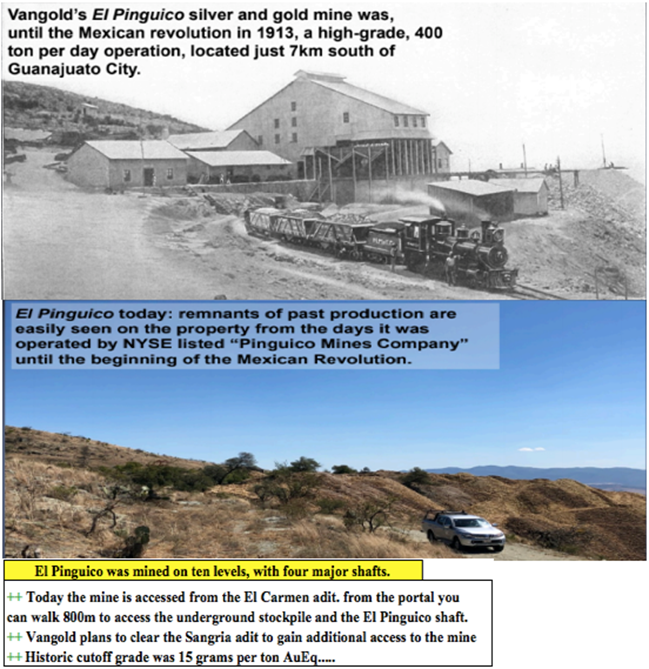

The company’s flagship property hosts the high-grade, past-producing El Pinguico mine that was only shut down due to the Mexican Revolution in 1913 (it wasn’t mined out). The mine operated on ten levels with four major shafts. From the early 1890s until 1913, El Pinguico was one of the highest grade mines in Guanajuato.

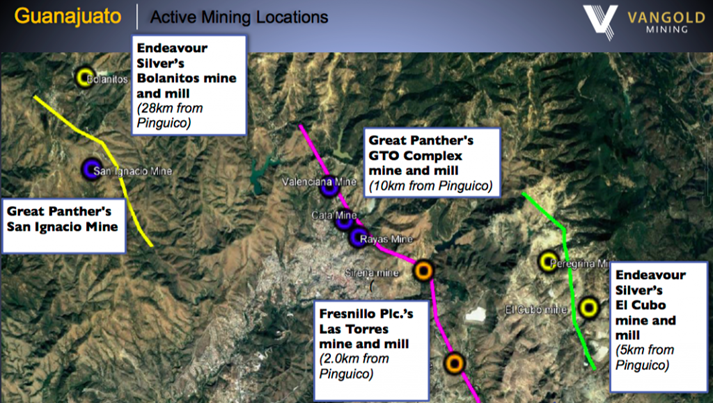

The cut-off grade was reportedly 15 g/t (0.48 oz./t) gold equivalent. Mining was done exclusively at the El Pinguico and El Carmen vein systems, which are thought to be splays off of the Mother Vein. El Pinguico is surrounded by well-known players, including Fresnillo PLC, Endeavour Silver, Great Panther and Argonaut Gold.

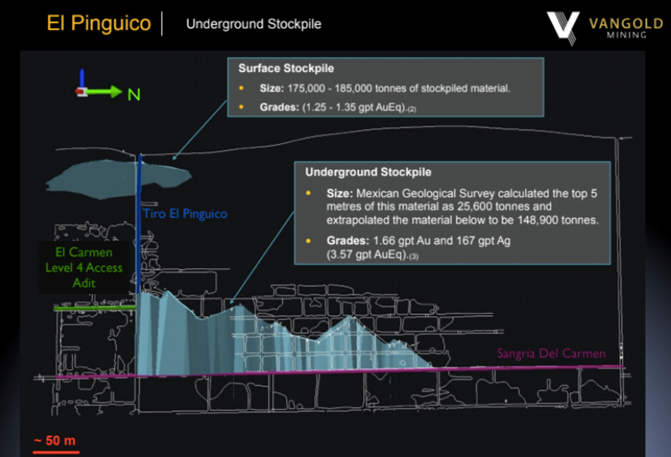

Modest near-term cash flow is possible from exploiting a surface stockpile this year, but more meaningful profit potential exists from extracting (and getting toll-milled) meaningful underground stockpiles grading ~3.6 g/t Au eq in 2012, the Mexican Geological Society estimated there were ~174,500 tonnes of material stockpiled underground. Assuming an 85% recovery, that equates to about a 20,000-ounce Au eq opportunity.

The plan is to reinvest net cash flow into new exploration and development activities at El Pinguico. It’s critical for readers to understand that Vangold has substantial exploration upside above and beyond monetization of stockpiles. Interestingly, the company stands to benefit from at least three things due to the global pandemic.

First, significantly lower energy costs, second, a favorable move in FX rates (weaker CAD$ and Mexican peso vs. the US$), and third, lower project costs (drilling, mining equipment and services, labor) as people will, presumably, be anxious to get back to work. Globally, unemployment rates are likely to remain elevated for an extended period.

Vangold has a substantial database of valuable exploration data including historical underground channel sampling and drilling. Samples from around the year 1909 include blockbuster grades. The best were; 0.7m @ 23.0 g/t Au + 3,858 g/t Ag, {~61.6 g/t Au Eq.}, another one of 0.8m @ 16.7 g/t Au + 3,054 g/t Ag, {~47.2 g/t Au eq}, and a third, 0.7m @ 15.7 g/t Au + 1,793 g/t Ag, {~33.6 g/t Au eq}.

As mentioned, prior mining at El Pinguico was from two vein systems (El Pinguico and El Carmen) thought to be offshoots of the Veta Madre (“Mother Vein”). The Veta Madre has been, and continues to be, incredibly important to the region. It stretches at least 25 km and has reportedly produced upwards of 1.2 billion ounces of silver.

From Endeavour’s website, “Silver was originally discovered by Spanish explorers in 1548 and subsequently at Guanajuato in 1552. Guanajuato is considered one of the top three historic silver mining districts in Mexico, having produced an estimated 1.0 to 1.2 billion ounces silver, plus 5 to 6 million ounces gold.”

The Veta Madre is also highly prospective for Vangold as it is known to extend to within 250 meters of the company’s border. Management believes it likely crosses through their property at between 400 and 600 meters depth. Importantly, Vangold is not the only company chasing the Mother Vein.

With a much higher gold price, silver not so much (yet), especially in Mexican peso terms, the region has become one of the hotter mining jurisdictions in North America. C$10 billion Fresnillo PLC is reopening a prolific (1970’s to 2002) mine that will bring additional workers, equipment and mining services to the area. The mine reopening is happening next year, just 2 km from Vangold’s project.

In addition to director Daniel Oliver, Vangold has a tremendous team for a company with a market cap of just C$2.7 million. Led by the highly experienced and well-connected James Anderson, who’s been working hard for the past year to revitalize this story, the company’s ship may have just come in. And, I should add, a rising (gold-silver) tide lifts all boats!

Readers should strongly consider taking a few minutes to review Vangold Mining’s (TSX-V: VGLD) / (OTCQB: VGLDF) brand new corporate presentation. Please visit the last two pages which extoll the considerable talents and experience of the management team.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Disclosures / disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Vangold Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Vangold Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned stock and warrants in Vangold Mining, and the Company was an advertiser on [ER].

While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Streetwise Reports Disclosure:

1) Peter Epstein’s disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Graphics provided by the author.

( Companies Mentioned: VGLD:TSX.V; VGLDF:OTCQB,

)