Source: The Critical Investor for Streetwise Reports 03/27/2020

The Critical Investor takes a look at recent actions taken by this gold explorer.

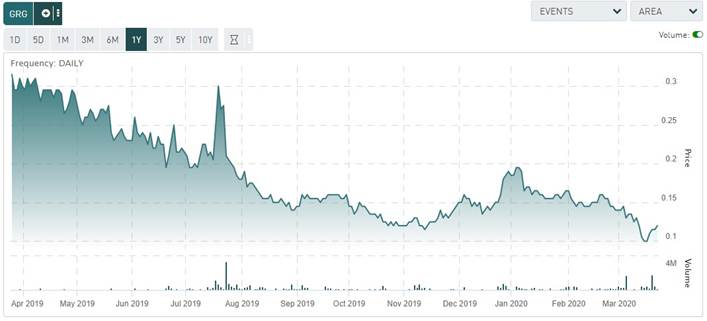

The coronavirus pandemic together with the Saudi Arabia-Russia oil production increase took its toll on the equity markets the last few weeks. The commodity markets in particular got hit too, as main end-user China got hit by a halt in manufacturing plants across the economy. Precious metals like gold rose initially, but after the virus spread globally it got sold off ruthlessly like any other asset class. Golden Arrow Resources Corp. (GRG:TSX.V; GARWF:OTCQB; G6A:FSE), as a gold explorer, didn’t come out completely unharmed either, as the following chart shows:

Share price Golden Arrow Resources 1 year time frame; Source Tmxmoney.com

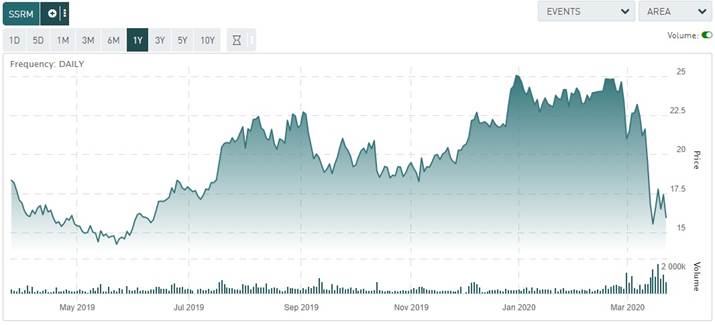

The drop in the share price for Golden Arrow is relatively comparable to that of SSR Mining, the company Golden Arrow holds roughly 1 million shares of (and which are the bulk of tangible assets at the moment):

Share price SSR Mining 1 year time frame; Source Tmxmoney.com

At a current market capitalization of just C$14.3 million, Golden Arrow trades below the value of its SSR Mining holding, which attributes to C$16.2 million. Besides this, Golden Arrow has a modest cash position and its exploration assets among which is the promising Indiana gold project in Chile, so it is safe to say that the company has reached decent support levels technically and fundamentally speaking. Management decided this was the case as well, and came to the conclusion that it was probably easier to buy back shares in order to create accretive value for shareholders instead of trying to create value through the drill bit on its projects.

For that purpose, management announced a normal course issuer bid on March 12, 2020, to purchase up to 10,658,050shares being equal to 10% of the float. This bid commenced on March 17, 2020, and will end on the earlier of March 16, 2021, or when it’s been completed or terminated. The shares will be bought in the open market by PI Financial on behalf of Golden Arrow Resources. Management and the Board clearly think this will be advantageous for shareholders, as they commented as follows:

“The board of directors of the company are of the opinion that the recent market prices of its shares do not reflect the underlying value of its property portfolio and its strong financial position. Accordingly, the purchase of shares through the bid is in the best interests of the company and its shareholders, as it will increase the proportionate share interest of remaining shareholders. The bid will afford an increased degree of liquidity to the company’s shareholders. The directors also believe that there will be long term benefits to the company with fewer shares issued and outstanding.”

This news release was followed a few days later on March 16, 2020, by a statement of the President, Chairman and CEO Joseph Grosso, of which a few highlights are presented here:

“I believe that today’s market sentiment has resulted in a share price that does not reflect the Company’s asset value, or our future potential value. At this time, our asset value includes:

- An extremely strong treasury of cash and cash equivalent securities.

- 100% control of a large property portfolio in Argentina with substantial geological values and work in progress.

- The yearly compliance fee to hold these properties in Argentina is amongst the lowest in the world.

- Three of Argentina’s most significant metal deposit discoveries had origins in this portfolio: Chinchillas, Gualcamayo and Navidad.

- Golden Arrow has devoted considerable time, expertise and investment into advancing the portfolio to include a pipeline of mineral projects at various stages of exploration.

“In addition, our potential value includes:

- Upside in our stock portfolio.

- The discovery potential of the multiple mineral projects that we are currently exploring in Argentina, Chile and Paraguay. Any of these projects has the geological potential to generate significant discoveries and value in the near future.

“I believe that the current market is creating the significant disparity seen between the share price and the combination of our asset value and exploration potential. This has created the opportunity for management to initiate an economical buyback of up to 10% of the public float of our shares, as approved by the TSX Venture Exchange. This will benefit the shareholders by increasing their proportionate share interest, increasing liquidity provide long-term benefits afforded by a tighter structure.”

After reading this, I wasn’t immediately convinced if this was the best possible action for a junior explorer with a lot of current assets to its disposal, in a bear market. I have several reasons for this.

- For juniors, cash is king in my view, and any available dollar should be guarded with their lives in bear markets, and preferably assigned solely to increase the value of their exploration assets.

- Besides this, in a bear market it often doesn’t matter what you do as a junior mining company, it is very difficult to get rewarded for your actions/results as everything gets dragged down no matter what. On the other hand, a bull market lifts up all boats, as they say, and you get the most bang for your buck, so it seems more efficient to undertake share price enhancing actions during a bull market. Applying the kind of cash being used now for the buyback but instead aimed at, for example, marketing programs and market makers during better times would likely generate more significant results.

- Furthermore, junior mining is a high risk, high reward sector, where share prices and market caps often fluctuate a lot, often based on nothing fundamental, and buyback programs are normally specifically based on enterprise values remaining the same in a more or less reliable and quantitative way, and resembles actions of blue chip multinationals.

Notwithstanding this, because of the current rout for oil companies, even the likes of Shell have halted their share buy back programs to save cash now, for harsh times to come. So, why Golden Arrow management decided to initiate a buyback program at a point where its SSR Mining shares are valued at about 40% lower compared to the highs of a few weeks ago, whereas Golden Arrow lost just 33% and already recovered towards a 20% loss from the share price right before the outbreak (probably caused partially by the buyback program itself), wasn’t really clear to me. If 10% of the float will be bought at an average price of 13c, this means C$1.38 million of precious cash will be gone. Therefore I asked them for more clarity on the subject.

Joseph Grosso commented himself as follows: “Golden Arrow has been trading at a discount to not only value, but to its cash (and cash equivalent) ever since the sale of Puna Operations to SSR Mining. Many investors had purchased Golden Arrow’s shares as a production story; even though we were a fairly passive investor in that project. The recent general market sell-off has exacerbated the discount. I believe that by initiating the repurchase of up to 10% of the company’s public float, we can show to the market that we firmly stand behind the value underpinning Golden Arrow. Since the announcement of our buyback program, the company’s shares are up by 20%. By reducing some of the outstanding shares, Golden Arrow is in effect mopping up excess stock held by investors with different investment objectives, and increasing the inherent value held across all remaining shareholders. As the bull market in gold continues to advance this should provide great leverage to all of our investors.”

One could wonder if investors who were in it for the leveraged production play didn’t already leave, and the sell-off wasn’t connected to a higher degree to the broader market sell-off itself, but let’s see what happens. At least they are buying back at an absolute low, and the leverage is optimized.

Exploration

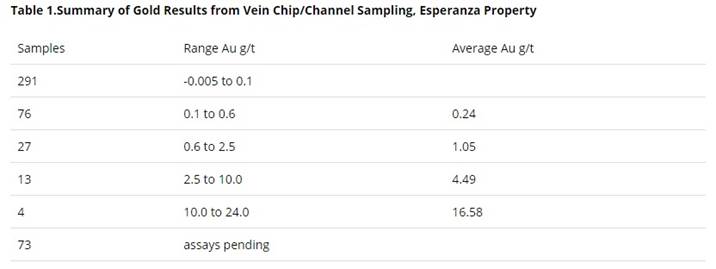

In the meantime, Golden Arrow progressed on its ongoing exploration programs, and the one at the Flecha de Oro project in Argentina delivered the first sampling results at the Esperanza and Puzzle properties. Sampling and mapping continued throughout the month of January at the Esperanza property, identifying high-grade and visible gold hosted in epithermal quartz veins. Especially the results at Esperanza were encouraging in my view, as shown here in this table:

Everything topping 1 g/t Au at surface is showing high potential in my view, so if about 40 of 500 samples show these results, the sampling program was successful in my opinion. Several samples also involved visible gold, as can be seen at these pictures (in green):

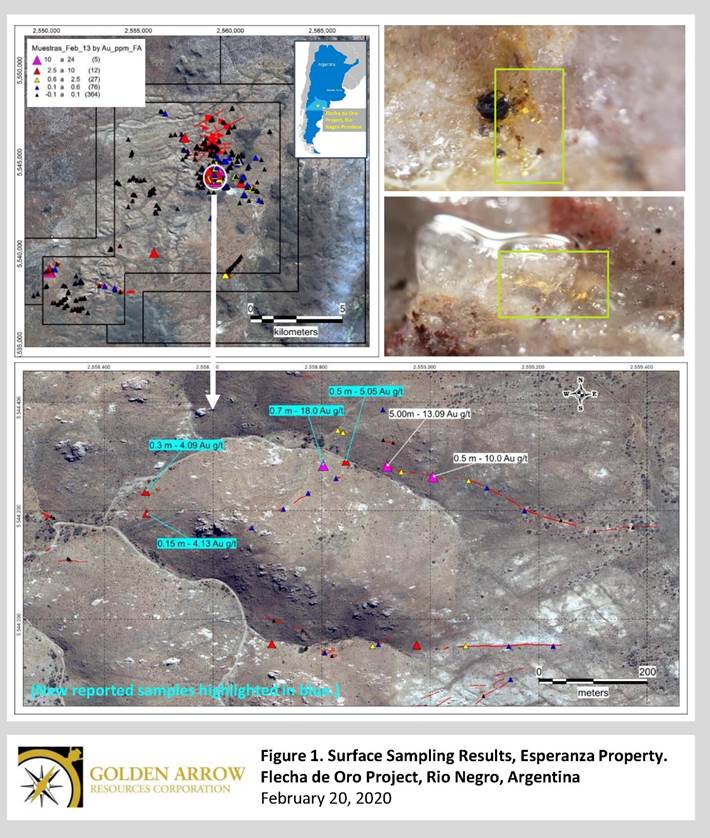

At Esperanza, Golden Arrow’s target is to define high-grade mineralized zones within the 16 kilometers of identified quartz and chalcedony veins that display epithermal textures. The mapping program is continuing to gain greater understanding of the structural plumbing system and distribution of classic epithermal vein textures that can provide formation temperature information, which are both important in targeting thicker and higher-grade zones.

The company is using the Cerro Vanguardia district as an exploration model for the Esperanza property. There are geological similarities between the two areas, in particular the presence of swarms of low sulphidation epithermal quartz veins in an area of approximately 100 square kilometers. The Cerro Vanguardia district is located in Santa Cruz province in southern Argentina, and includes over 100 gold and silver-bearing epithermal veins. The district has a cumulative exposed vein strike extent of more than 240 kilometers, and has produced more than 4.5 million ounces of gold over the last 20 years.

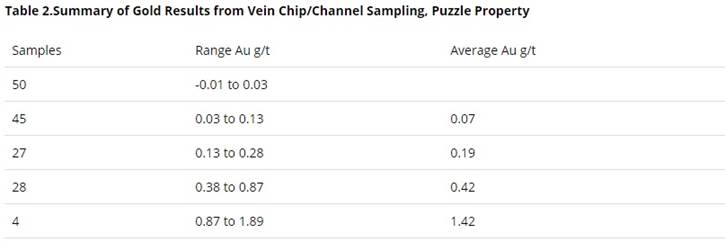

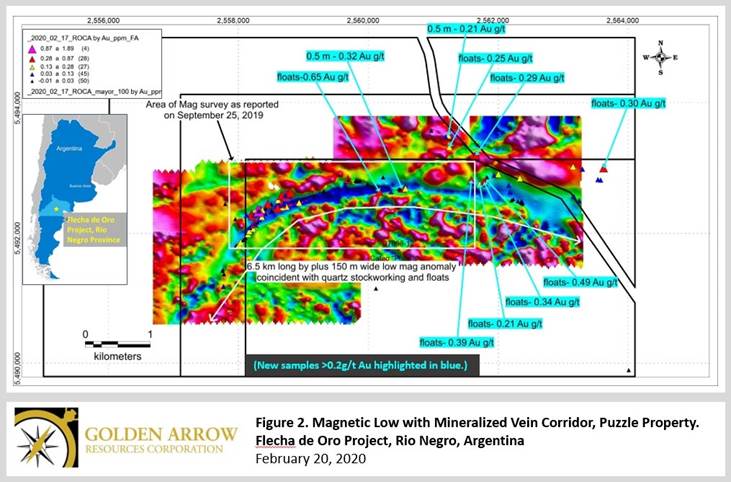

Golden Arrow Resources also received sampling results for the Puzzle property, but these were, despite establishing a trend of 6.5km, of much lower grade, and therefore of lower interest/potential in my view, especially since it is not heap leachable potential:

The trend can be seen here:

Despite these low-grade sampling results at Puzzle, the company made applications for additional concessions around both the Esperanza and Puzzle properties.

I also wondered if the corona pandemic had any influence on the ongoing exploration programs, and VP Exploration and Development Brian McEwen had this to say about this subject: “The Corona pandemic is a global phenomenon. Our first priority is the safety of our staff and personnel. Our organization is abiding by all the local regulations in every jurisdiction to keep our people safe. Although our exploration programs have been placed on a temporary holding pattern, we expect to pick up when this pandemic has passed us. We will provide updates, as appropriate.”

Conclusion

The share buyback program of 10% of the Golden Arrow Resources float came a bit as a surprise for me, as this is unusual for junior mining companies. After contacting Joseph Grosso, the reasoning became more clear, as they figured there were still investors with the objective of holding a (leveraged to silver) production play selling their shares, and they wanted to clean those up. The coronavirus seems to have a delaying impact on operations, according to Brian McEwen, as they paused their exploration programs in order to comply with all pandemic related regulations. It seems investors have to wait out the pandemic and its fallout, but in the meantime these share price levels trading below cash seem an interesting time to entry (or re-entry).

I hope you will find this article interesting and useful, and will have further interest in upcoming articles on mining. To never miss a thing, please subscribe to The Critical Investor’s free newsletter, http://www.criticalinvestor.eu, in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclaimer: The author is not a registered investment advisor, currently has a long position in this stock, and Golden Arrow Resources is a sponsoring company. All facts are to be checked by the reader. For more information go to www.goldenarrowresources.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor’s disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Golden Arrow Resources, a company mentioned in this article.

Charts and graphics provided by the author.

( Companies Mentioned: GRG:TSX.V; GARWF:OTCQB; G6A:FSE,

)