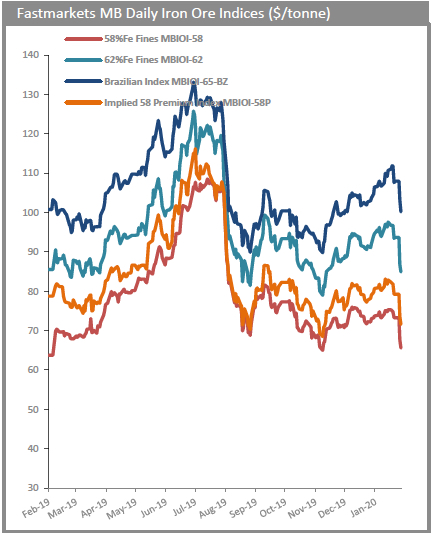

Benchmark iron ore prices fell again on Thursday as China, responsible for more than 70% of the world’s seaborne iron ore trade, struggles to control the novel coronavirus outbreak.

The Chinese import price of 62% Fe content ore dropped sharply after the resumption of activity following the Chinese lunar new year break yesterday and continued to decline on Thursday to $84.94 per dry metric tonne, according to Fastmarkets MB. Declines over the two days not total 9.4%.

A key difference to SARS is that many factories and other workplaces have been closed indefinitely.

The number of confirmed cases were approaching 8,000 while the death toll climbed to 177 on Thursday. Infections are outstripping the figure in mainland China during the SARS outbreak of 2002–2003 and the death toll is likely to be exceeded over the weekend.

In a research note Capital Economics said at this stage the economic impact of the outbreak is due to Beijing’s measures limit transmission, notably in transport passenger numbers over the holiday which have declined at a rate similar to that seen during SARS of some 30% (kilometres travelled per person).

Capital Economics says after SARS, consumer demand rebounded rapidly as households spent the money they had saved and the economy recovered strongly as a result:

A key difference now is that many factories and other workplaces have been closed indefinitely. This did not happen on a large-scale during SARS. If closures continue, the impact will spread through supply chains, threatening job losses and prolonged weakness.

Another potential channel for domestic economic dislocation is inflation. This could result from stockpiling or disruption to distribution networks.

Stimulus response

BMO Capital said in a research note on Monday that the Beijing’s response to the outbreak, assuming it can be brought under control, could be significant.

The investment bank believes the Chinese government ~6% growth target for 2019 “is likely non-negotiable in order to meet the doubling of per capita GDP promised by President Xi in 2020 versus 2010”:

And with consumption weaker, this will likely involve more fixed asset investment-heavy government spending.

As a result, we may see another push into infrastructure projects into mid-year, while property restrictions could be further eased.

For metals and bulk commodity demand, we see a slightly weaker Feb-March than may have been anticipated, but limited changes to expectations for the year as a whole.

Furnaces are blasting

Last week economic data showed the country’s steelmakers produced just shy of 1 billion tonnes in 2019, the second record-breaking year in a row.

China produces more crude steel than the rest of the world combined, reaching 996.3 million tonnes in 2019, up 8.3% over the prior year, according to government figures. During December, steelmakers churned out on average 2.7m tonnes per day, 12% higher than December 2018.

Production of steel products in China grew by nearly 10% from a year earlier to 1.2 billion tonnes in 2019. The China Iron and Steel Association said last week it expects domestic demand for steel to grow modestly in 2020, to roughly 890m tonnes.

Imports top 1 billion tonnes

Chinese imports of the steelmaking raw material topped 1 billion tonnes for the third year in a row as Beijing’s efforts to stimulate the economy pay off.

China’s iron ore purchases in December totalled 101.3m tonnes, up nearly 12% from July and 17% from last year customs data showed, marking the highest level of imports since September 2018.

Full year iron ore imports were the second best on record at 1.069 billion tonnes, up 0.5% from last year and within shouting distance of 2017’s record 1.075 billion tonnes.