This post QE Is Much Closer Than You Think appeared first on Daily Reckoning.

Today we hazard a thumping prediction:

The next round of quantitative easing — official, actual quantitative easing — is fast approaching.

Yes… the Federal Reserve will soon be clearing for emergency action.

When precisely can you expect it? And why the urgency?

Answers shortly. Let us first squint in on Wall Street…

The Bears Win on Points

The Dow Jones took a 28-point flesh wound today. The S&P lost but three points; the Nasdaq, five.

Gold gained $4 today, while 10-year Treasury yields rose ever so slightly — to 1.83%.

A humdrum performance altogether, this day put in.

But when can you expect the next round of authentic quantitative easing… and why so soon?

We must first distinguish between official quantitative easing and its junior shadow, “QE-lite”…

The Difference Between QE and QE-lite

Quantitative easing had a strategic vision. That is, it was intended to stimulate.

And so it stomped mercilessly upon long-term interest rates… and battered them down to nothing.

QE-lite — conversely — lacks all strategic vision.

It is workaday… and technical. It simply fills a leakage somewhere within the financial plumbing.

It consists of mere “open market operations” the Federal Reserve has always conducted.

And it fixes upon short-term rates — unlike quantitative easing. Its mission is therefore limited.

The Birth of QE-lite

The Federal Reserve initiated QE-lite in September, when liquidity ran dry in the short-term lending markets.

The Federal Reserve’s New York crisis management team rounded into action, unfurled the hoses… and gave these markets a good thorough drenching.

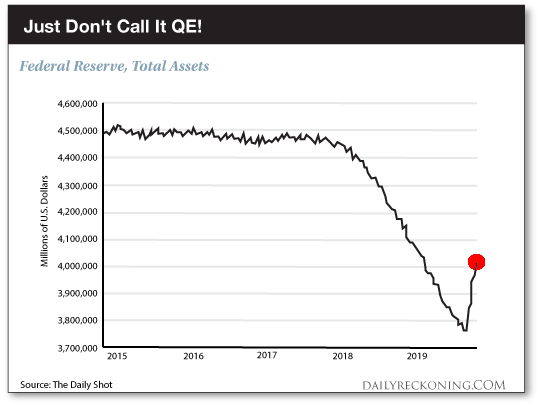

They are still hard at the business — and inflating the balance sheet beautifully.

The Federal Reserve’s balance sheet came in at $3.8 trillion in September. Yet it presently expands to $4.07 trillion.

Yesterday alone the New York crew emptied in $81.4 billion of liquidy credit.

Yet we are assured none of it has seeped into the central water lines of the stock exchanges.

Morgan Stanley’s interest rate strategist Matt Hornbach thus informs us:

There is little debate that the Fed is increasing the quantity of money, or Q. However… the additional money lacks a direct transmission mechanism to the equity markets or other long-duration risk assets.

Just so. QE-lite nonetheless expands the Federal Reserve’s balance sheet, as shown. And the balance sheet is the central scene of action.

Is it coincidence the major indexes have established fresh records recently?

“Like a Fourth Rate Cut This Year”

As we noted last week:

The S&P turned in only one negative week these past two months. That was the same week — and the only week — that the balance sheet contracted.

QE-lite is “like a fourth rate cut this year,” affirms Matthew Miskin, John Hancock co-chief investment strategist.

Meantime, Jerome Powell claims QE-lite has patched the financial plumbing. All leaks are wrenched shut.

Yet independent inspectors are far from convinced. Some see not patched leaks — but ongoing hemorrhagings…

Broken

James Bianco of Bianco Research:

The big-picture answer is that the repo market is broken. They are essentially medicating the market into submission. But this is not a long-term solution… This is now far bigger than anyone thought this was going to be. I think they’re hoping the market will magically fix itself. I don’t see why it would.

Nor do we.

The Federal Reserve is currently three months deep into these “temporary” open market operations.

And they will run “at least into the second quarter” of 2020… by Mr. Powell’s own admission.

We bet high they will go into the third quarter of 2020. And likely the fourth.

But why have the Federal Reserve’s heroic floods of liquidity failed to fill the pipes?

Here is the likely answer:

It can pump in its liquid. And it has. But it cannot guarantee it sloshes on through to its intended destination.

Clogs may bottle it up.

The Clogs in the System

We first must understand the repo market piping. Explains Reuters:

In a repo trade, Wall Street firms and banks offer U.S. Treasuries and other high-quality securities as collateral to raise cash, often just overnight, to finance their trading and lending. The next day, borrowers repay the loans plus what is typically a nominal rate of interest and get their bonds back. In other words, they repurchase, or repo, the bonds.

Twenty-four banks — or “primary dealers” — run direct lines to the liquidity taps.

That is, they transact directly with the Federal Reserve. From these primary dealers the liquidity goes sluicing out through the repo market.

Yet these banks have evidently chosen to sit on their supplies… rather than lend them to thirsting recipients.

Our minions inform us that over 70 financial institutions presently go without.

Hence the liquidity shortage.

The Bank for International Settlements (BIS) has reached the same conclusion.

BIS fingers four banks in particular. Yet it failed to identify the culprits… for what it is worth to you.

But why are these bloated and hoggish banks refusing to lend as needed?

Bloated and Hoggish Banks

Here is why they decline to put loanable funds on offer:

They can store their hoards at the Federal Reserve instead — where they earn a superior interest.

Bryce Doty, is a senior portfolio manager at Sit Fixed Income. From whom:

The big banks are just hoarding cash. They told the Fed they have more than enough cash in excess reserves to meet regulatory issues, but they prefer having money at the Fed where they can still earn 1.55%, rather than in the repo market.

In addition, elevated post-crisis capital requirements incentivize banks to pile up reserves rather than loan them.

So concludes our brief canvas of the repo market… and its present woes.

Yet we promised a prediction at the outset… that the Federal Reserve will soon undertake the next official round of quantitative easing.

But when?

We now gaze into our polished, haze-free crystal sphere for the answer…

Prepare for Imminent “Official” QE

The Federal Reserve will initiate the next official round of quantitative easing — QE4 — before this year runs out.

That is, before Jan. 1, 2020.

This is actually the near-prediction of Credit Suisse analyst Zoltan Pozsar.

Here is the hinge upon which it rests:

Whether or not the Federal Reserve loses control of overnight rates in the weeks ahead.

Mr. Pozsar has toiled for both the New York Federal Reserve and the United States Department of Treasury.

Thus he is exquisitely familiar with the financial plumbing. And this fellow believes the Federal Reserve’s patchwork has failed to plug the leaks.

Repo market funding remains unequal to requirements, he insists. Meantime, regulatory burdens on the primary banks are “shaping up to be a severe binding constraint.”

And so this Pozsar detects a main pipe groaning, rattling and giving… ready to rupture.

He believes the weeks ahead are “shaping up to be the worst in recent memory.” Moreover, he concludes “the markets are not pricing any of this.”

“If we’re right about funding stresses,” he concludes, “the Fed will be doing ‘QE4’ by year-end.”

But let us take this near-prediction, strip its escape clause, challenge its manhood and put steel in its spine:

The Federal Reserve will be doing “QE4” by year-end.

That is our prediction, presented with a wry grin. Let the countdown begin…

Regards,

Brian Maher

Managing editor, The Daily Reckoning

The post QE Is Much Closer Than You Think appeared first on Daily Reckoning.