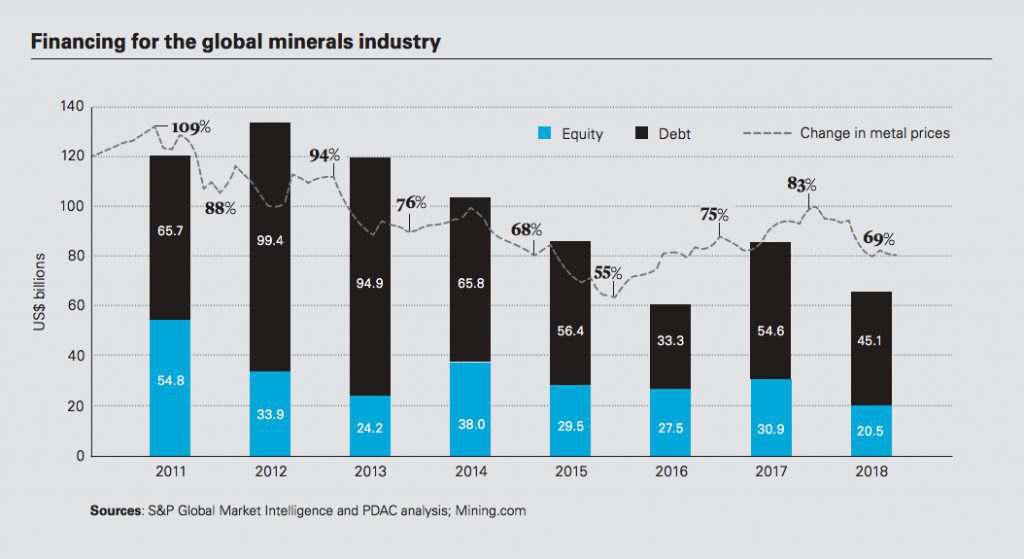

The mining and

metals sector is certainly facing challenges, one of the biggest being raising

capital to fund the projects needed to bring the minerals of the future to

market to fuel the electric era.

In an industry known for being typically slow to adopt technology innovations, some miners, especially cash-strapped juniors, are needing to explore new financing structure options.

Cynthia Urda Kassis, head of Mining and

Metals at Shearman and Sterling, said that or the past several years at least

one of the biggest challenges facing the junior miners in particular is raising

capital.

“I think that in the market at the moment there’s a lot of different ways of raising capital in terms of not just the traditional commercial banks, Expo-credit agencies, multilaterals, streamers and royalty companies. You have a whole bunch of new sources together with the old… but the equity side has lagged behind,” Urda Kassis told MINING.com.

Urda Kassis said streamers and private equity houses have created the hybrid instrument which has tried to narrow that gap but at the end of the day there is still minimum amounts of true equity and that is the biggest challenge.

An STO is a digital asset that is structured to comply with applicable securities regulations. It is the same as a regulated investment, wrapped in a digital token structure

A success story which

Urda Kassis was involved in arranging alternative financing for is Nevada

Copper’s Pumpkin Hollow project.

In 2017, Nevada entered into a $378 million construction financing and recapitalization package, including a $70 million precious metals stream, $80 million senior secured loan and $53 million debt to equity conversion.

In May 2019, Nevada Copper inked a $115 million credit agreement with Germany-based KfW IPEX-Bank and also announced a public share offer and concurrent private placements to raise $30m, two off-take agreements with European metal companies Aurubis and Concord Resources and a working capital facility worth $35m.

In October, Nevada

Copper announced remains on target to commence production in Q4

2019 and to complete within its project cost estimate.

Blockchain-based solutions

For an industry known for being typically slow to adopt technology innovations, miners are increasingly adopting blockchains and smart contracts, a study by global law firm White & Case shows.

Mining royalty and metal streaming financings, the authors of Rise of digital finance: Tokenising mining assets and metal streams, Rebecca Campbell and Andrzej Omietanaski say, have been particularly popular with miners in the last decade as an alternative financing source for growth projects, allowing access to early-stage capital without diluting equity ownership.

Rapid advances in blockchain technology are reinventing the way companies operate and deliver products and services to their clients, according to the authors.

“Tokenized mining royalties combine a traditional royalty instrument like an instrument that pays out by reference to actual mineral production or revenue derived from a mine site with an STO structure,” Campbell told MINING.com.

An STO, — a security token offering — is a digital asset that is structured to comply with applicable securities regulations. It is the same as a regulated investment, wrapped in a digital token structure.

STO’s emerged in 2018, evolving from the ICO — introductory coin offering — a blockchain-based fund-raising mechanism in which new cryptotokens are created and sold to purchasers by the project itself in exchange for fiat and/ or cryptocurrencies, typically Bitcoin or Ethereum.

“Another way to think of it is that mining companies are able to securitize individual royalties via the STO — this contrasts to the current model where in most cases the counterparty to royalty instrument is a private mining fund or a listed royalty company,” Campbell said.

She added that an STO

can be backed by any form of asset. In the case of tokenized mining royalty,

they are backed by the royalty instrument itself – to the extent the royalty

pays out, the token benefits.

While some see blockchain-based structures as a kind of

financing revolution, Campbell sees it as an evolution.

“It is trendy to describe various aspects of digitalization and automation of the mining industry and of the capital markets as ‘revolutionary’. We think the opposite — it is quite a natural evolution of the existing capital raising techniques employed by the sector, especially in this case where the underlying asset is quite a traditional instrument.”