The price of copper weakened again on Thursday amid the worst US factory conditions in a decade and near-record bearish bets on futures markets on the bellwether metal.

In afternoon trading in New York, copper for delivery in December was trading just off its low for the day of $2.538 a pound ($5,596 a tonne), bringing losses for 2019 to more than 5%.

Trade worries have dogged copper price bulls for the better part of a year, but more recently weak data from China, the US and Germany, together responsible for 70% the world’s consumption, have intensified the sell off.

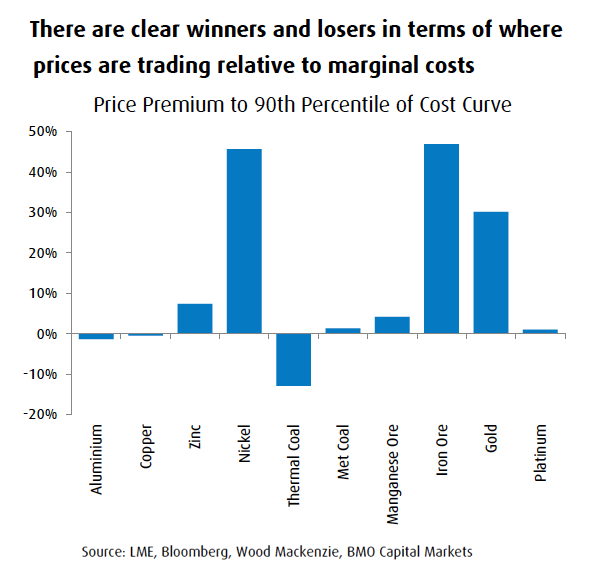

While there is near unanimous consensus that copper’s long term prospects are bright (particularly under a Greta Thunberg scenario), a lower for longer price is likely to cull the industry of marginal producers – those in the 90th percentile of costs.

In a new report, BMO Capital Markets slashed its forecast for the copper price for next year by 9.6% to $2.93/lb ($6,460/t) and by smaller margins through 2023. The investment bank kept its long-term equilibrium price for the orange metal steady at $3.25/lb ($7,165/t).

BMO calculates at current prices, some 10% of copper mines around the globe are operating at a loss (while nickel extractors can’t believe their luck – see graph).

Apart from longer term trends like falling grades at mature mines, metals consultancy CRU estimates weakness in prices for metals mined as a byproduct – particularly cobalt – has added roughly $290 per tonne this year. Without higher gold and silver prices, upward pressure on costs would have been even more intense.