It’s official: Donald Trump has become only the fourth president in U.S. history to be the subject of a House impeachment inquiry.

I won’t say much on this, as the details of the inquiry are still unfolding. Plus, it’s an extremely divisive topic.

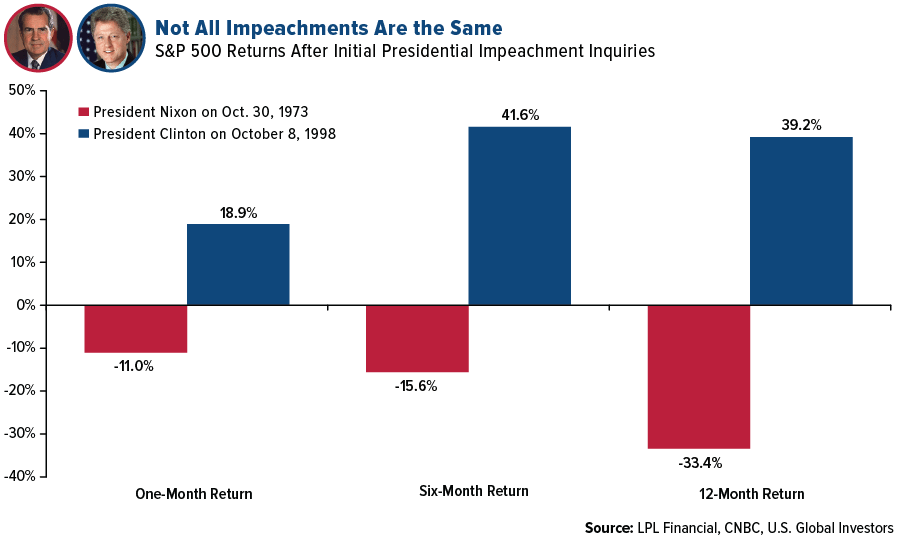

I will say one thing. If history is any guide, it’s highly unlikely that Trump will be convicted of any impeachment charges, especially with Republicans in control of the Senate. The only two presidents who have ever faced such charges, Andrew Johnson and Bill Clinton, were both acquitted. Richard Nixon, as you know, resigned before articles of impeachment could be drawn up.

I don’t believe investors have too much to worry about in the short term, despite Trump’s warning that “markets would crash” if he were impeached. “Do you think it was luck that got us to the Best Market and Economy in our history,” he tweeted last week. “It wasn’t!”

The sample size is small, but history shows that impeachments have had minimal impact on markets, and outcomes have been inconsistent. Stocks slid in the months following the start of Nixon’s impeachment inquiry, but far more important factors were at play, including the collapse of the Bretton Woods monetary system, the 1973 oil crisis and the start of the 1970s recession. In Clinton’s case, stocks ended up nearly 40 percent 12 months after the House announced its plans to impeach. But again, context matters. The U.S. economy was strong in the late 90s, and we were at the tail end of one of the longest equity bull markets in history.

The scenario today looks very much the same. The U.S. economy—though it may be showing some cracks—is still going strong. Stocks have so far shrugged off threats of impeachment. Going forward, I would place the blame of any potential market weakness on other factors, from the global economic slowdown to ongoing trade tensions between the U.S. and China.

Germany on the Cusp of Recession

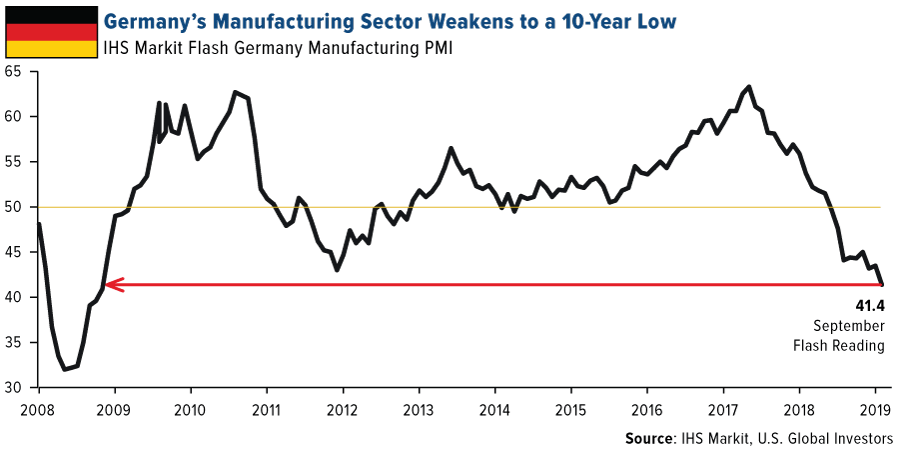

Indeed, if we look overseas, there’s much more that could rattle markets than U.S. political theater. Germany, for instance, may be on the cusp of recession, if it has not already entered one. The preliminary purchasing manager’s index (PMI) for September shows that the manufacturing sector in the world’s fourth largest economy is contracting at its fastest pace since the depths of the global financial crisis a decade ago. The flash PMI registered 41.4, an alarming 123-month low.

“The manufacturing numbers are simply awful,” commented Phil Smith, principal economist at IHS Markit, which produces the monthly report. “All the uncertainty around trade wars, the outlook for the car industry and Brexit are paralyzing order books.”

Car sales have been slowing across Europe for months now, as I’ve written about before. In August they were down a whopping 8.4 percent year-over-year, according to the European Automobile Manufacturers Association (ACEA). This has been a drag on Germany’s important automotive manufacturing industry, Europe’s largest and the world’s fourth largest by production.

Suppliers are feeling the pain as well. Continental AG, the Hanover, Germany-based manufacturer of auto parts, said this week that as many as 20,000 jobs were at risk over the next decade as plants will be closed not only in Germany but also Italy and the U.S.

Nervous investors have run for cover in the German bond market, where yields across the entire yield curve are currently trading in negative territory.

Helicopter Money Ahead?

A record $17 trillion in global debt now carries a negative yield, which is equivalent to about 20 percent of world GDP, according to a recent report by the Bank for International Settlements (BIS). The bank notes that the growing acceptance of negative yields has become “vaguely troubling.”

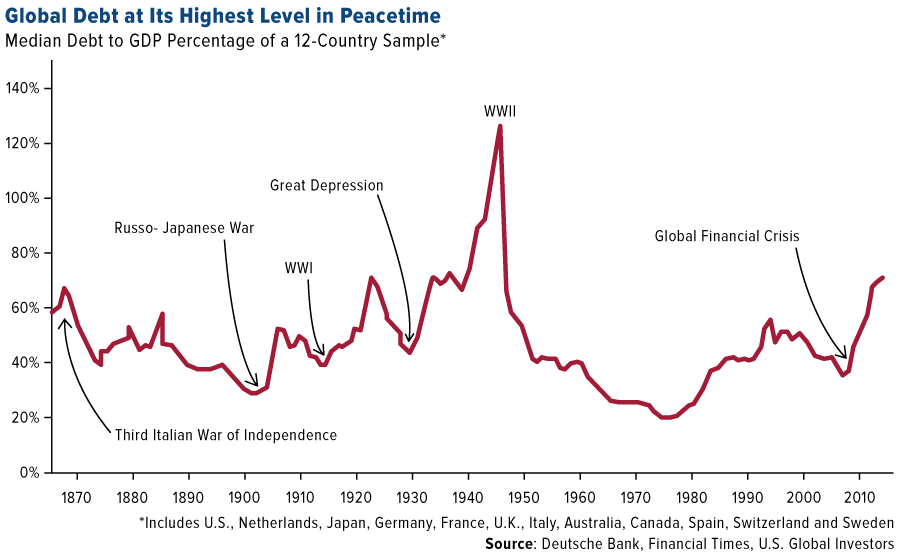

Just as troubling is the expanding level of global debt, which is now the highest it’s ever been in peacetime, according to Deutsche Bank’s recent analysis of 12 major economies. These dozen economies collectively have an average debt-to-GDP of 70 percent, the highest level in 150 years outside of a world war.

Jim Reid, the report’s lead author, warns that we may see central banks continue the sort of unconventional market interventions that have propelled record levels of borrowing in the first place.

“The multi-trillion dollar question is whether governments can successfully and consistently issue the holy grail of funding—zero-coupon perpetual bonds. If they can do that, spend the money, and central banks buy the bonds, then that is pure helicopter money,” Reid writes.

In its simplest terms, “helicopter money” refers to a rapid surge in money-printing, the hope being that it will spur economic output.

An inevitable consequence to this, of course, is runaway inflation. See: Weimar Germany, Zimbabwe and, more recently, Venezuela.

WGC: Gold Is Still Under-Represented

I see gold as a solution to many of the issues I’ve laid out, whether it’s recessionary spillover from Germany, high debt levels or helicopter money.

I’m not alone in thinking this. In a September report, the World Gold Council (WGC) calls the yellow metal “the most effective commodity investment,” adding that “allocations of 2 percent to 10 percent in a typical pension portfolio have provided better risk-adjusted returns than those with broad-based commodity allocations.”

However, the WGC says, gold is under-represented in most commodity indices, meaning investors are underexposed.

“Investors who access commodities via a broad-based index often assume they have an appropriate allocation to gold. In fact, most broad-based commodity indices have a very small allocation,” the WGC analysts write.

Consider the S&P GSCI, which tracks 24 commodities. West Texas Intermediate (WTI) oil and Brent oil make up nearly half of the index with a combined weighting of 45 percent. Gold, meanwhile, represents only 3.73 percent of the index.

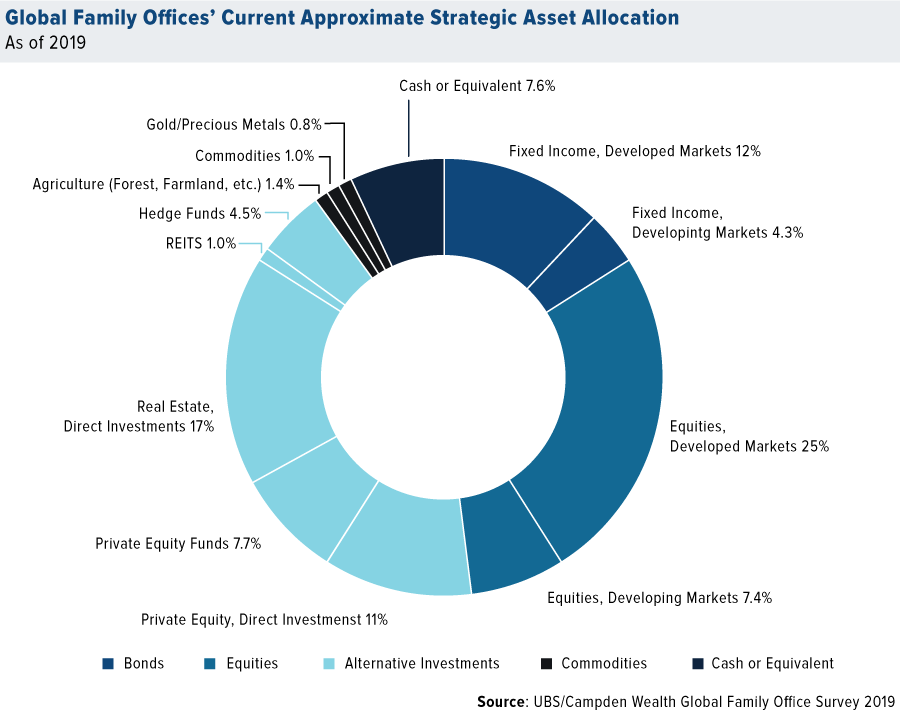

This underexposure can be seen in a recent review of global family offices’ asset allocations. UBS’ Global Family Office Report 2019, released this week, shows that gold represents as little as 0.8 percent of portfolios on average. Equities in developed markets are the top position, representing a full quarter of portfolios, but some managers say they are trimming their exposure in preparation for a potential recession. A full 55 percent of family offices believe a recession will make landfall by 2020, according to the study.

The good news is that, of the 360 family offices surveyed—which collectively manage approximately $5.9 trillion—17 percent said they were planning to increase their gold position in 2020. More than three quarters said they were keeping it the same. Only 5.3 percent said they would be decreasing their exposure.

Increasing their gold exposure, I believe, would be rational and prudent at this time. As I told Kitco News’ Daniela Cambone at the Denver Gold Forum (DGF), the longer yields stay negative around the world, the better the chances are of gold rocketing up to $10,000 an ounce. You can watch the entire interview by clicking here.

Congratulations to the U.S. Global Marketing Team!

On a final note, I wish to congratulate our marketing team for the recognition they received last week from the Investment Management Education Alliance (IMEA), which promotes knowledge-sharing and investor education among marketers who work in the financial industry.

At this year’s event in Chicago, our team picked up two STAR awards, for Best Newsletter and Best Product Education Campaign, as well as special recognition for its community volunteering. U.S. Global now has 88 STAR awards to its name.

These accolades would not be possible without you, our readers and subscribers, so thank you!

If you’re still not subscribed to the weekly Investor Alert, you can do so by clicking here.