Source: The Critical Investor for Streetwise Reports 09/25/2019

The Critical Investor delves into this lithium firm’s recovery method for its Arkansas project and why it may succeed when other companies’ have not.

1. Introduction

Usually, when I hear about companies pursuing new recovery methods necessary to make uneconomic specialty metals projects economic, I’m very skeptical about their chances of success. The simple reason for this is that developing such methods are very capital intensive, and very difficult to scale up from bench scale (laboratory scale) to commercial scale pilot plants. In the lithium space there are several examples of junior mining companies with similar initiatives, backed by giant chemical companies providing tech and pilot plants for many years, but unsuccessful in proving up commercial production. So when I was introduced to Standard Lithium Ltd. (SLL:TSX.V; STLHF:OTCQX) and its story, I was skeptical at first as well.

However, when I heard about the successful testing so far, the concept of recovery, the knowledge and experience involved, the JV partner and its ability to raise significant amounts of cash during the latest downturn in venture and lithium sentiment, it dawned on me that this might be a company with above average chances of success, and actually making it into commercial production. It is progressing pretty fast as well, which I also regard as a good sign. In this analysis I will discuss several important aspects, the economic potential of the Lanxess project, and the potential impact on valuation if things go as planned.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. The company

Standard Lithium (SLL.V) is a publicly traded technology and project developer advancing its lithium brine project in Arkansas, U.S. The company is currently focused on the development of its flagship 150,000-acre Lanxess Project located in southern Arkansas. The region is home to North America’s largest brine production and processing fairway. The location has significant infrastructure in place, with easy road and rail access, abundant electricity and water sources and is already permitted for extensive brine extraction and processing activities.

Standard Lithium isn’t a traditional venture mining company, which are usually mostly focused on exploring and developing mineral resources. This company is more about applying new direct extraction technologies at the project level, and leveraging the core competencies and investments of strategic partnerships to reduce capital and execution risk. Standard Lithium is focused on applying these modern extraction methods on existing large-scale U.S.-based brine resources that have the potential to be quickly brought into production for battery quality lithium materials. As the eventual construction of this type of project would be very capital intensive for a relatively small junior, Standard Lithium has partnered up with Lanxess AG (LXS:DE), a global Germany-based specialty chemicals company, which is listed in Germany and has a market cap of US$5.12 billion.

Lanxess has a very large brine based bromine extraction operation in southern Arkansas, and Standard Lithium aims through a JV to test and prove the commercial viability of the extraction of lithium from brine (“tail brine”) that is a byproduct of the existing bromine production facilities of Lanxess.

Standard Lithium has two projects; the flagship Lanxess project is located in Arkansas, but unfortunately there is no mention of it in the most recent Fraser Institute Survey of Mining Companies. The second project is the Mojave project, and is located in California. This article will be about the flagship Lanxess project only. Talking about jurisdictions, California doesn’t have a very good reputation for permitting, and therefore is ranked only 49 out of 83 in the latest survey, but Standard Lithium isn’t teaming up with existing and fully permitted operators in both locations for no reason. After extensive consultations with regulators, governments and community spokesmen in Arkansas, Standard Lithium believes there is no reason to believe that permitting additional facilities at the much larger Lanxess processing site will be a problem.

Standard Lithium is basically led by two men: CEO Robert Mintak and President and COO Andy Robinson, PhD. Mintak is a pioneer in the lithium space, has a powerful global network, and has been CEO of Pure Energy from 2013 into 2016 before he switched to Standard Lithium. He has been largely responsible for raising over C$40 million for Standard in the past few years, brings in deals like Lanxess and tells the story tirelessly across the world. Robinson is the technical brain behind Standard; as a geoscientist he has more than two decades of experience in geochemistry and groundwater-focused projects. He worked alongside Mintak as COO of Pure Energy and joined him at Standard Lithium.

Another key figure is Non-Executive Chairman Robert Cross, who founded B2Gold and currently still is the chairman of this company, which is approaching an annual production of 1 Moz gold. On top of this, Standard Lithium has a very interesting technical team of advisors, among them very experienced global thought leaders like Chemistry Nobel prize winner Prof. Barry Sharpless, Prof. Jason Hein who specializes in applying AI in reaction optimization, and other longtime specialists in the field of solvent/ion-exchange, flow sheets, pilot plants, process engineering, etc., who all have very active roles in the development of the new recovery process of Standard Lithium. As a result, Standard is working together with three different universities, having the best and brightest minds working on the new recovery method, and COO Robinson believes this approach enabled Standard Lithium to be successful so quickly, in relative terms.

Standard Lithium has its main listing on the main board of the TSX Venture, where it’s trading with SLL.V as its ticker symbol. With an average volume of about 60,778 shares per day, the company’s trading pattern is reasonably liquid at the moment, and I expect this to improve when positive demonstration plant results start coming in.

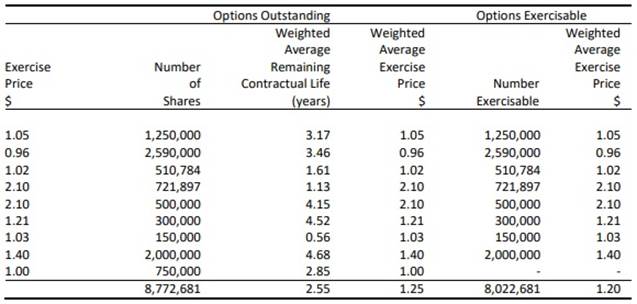

The company currently has 87.59 million shares outstanding (fully diluted 111.2 million), 14.85 million warrants (of the warrants outstanding, 3,125,000 are exercisable to acquire one common shares at $0.25 expiring May 10, 2021; 5,156,411 are exercisable at $2.60 per share, expiring on February 16, 2020; 5,695,250 are exercisable to acquire 1 common share at $1.30 expiring February 21, 2022; 656,675 are exercisable to acquire 1 common share at $1.00 expiring on March 21, 2021; and 213,000 are exercisable to acquire 1 common share at $1.30 expiring on April 10, 2022) and several option series to the tune of 8.77 million options in total, details are shown here:

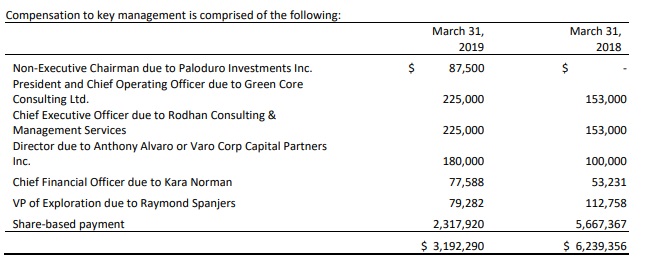

A current share price of C$0.81 results in a market cap of C$70.9 million. Management has decent skin in the game, as Mintak, Robinson and Cross each hold 1–1.5 million shares, and each over 1 million options. In total, management and BoD hold about 4 million shares, which is 4.5%. Significant holders are Commodity Capital (9.9%), Global Lithium ETF, Fosun International, National Chloride and Tetra Technologies, which in total hold 9%, which means roughly 23% is in relatively tight hands. I also looked into the compensation of management, and noticed pretty high share-based compensation numbers at first sight.

CEO Mintak had the following explanation, which sounded reasonable, as this compensation wasn’t shares or even close:

“Share-based compensation in 2018 included total of 721897 compensation options priced at 2.10 from our Feb 2018 $21M raise that expire Feb 2020 so we need to move the share price higher than 2.10 in 6 months for those to be in the money or they expire, also included an RSU compensation plan total of $2.1M at $2.10 that was subsequently canceled but required to be 100% expensed because of IRFS rules even though they were canceled. The rest were options that were issued and are under exercise price now.”

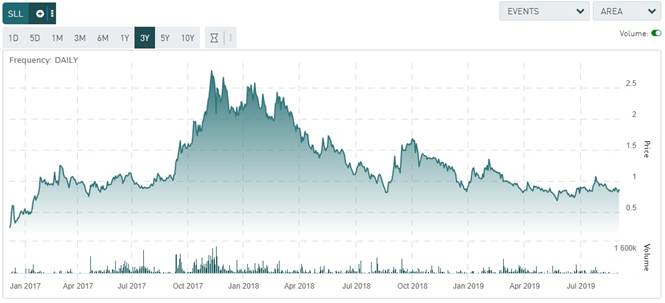

Standard’s working capital position at the end of the last reporting period, Q3 March 31, 2019, was C$9 million. In my view it is an interesting moment to enter and wait for the testing, Pre-Feasibility Study (PFS) and the Lanxess decision, as the stock seems to have bottomed out for quite a while now:

Share price; 3 year Standard Lithium, tmxmoney.com

The 2017–early 2018 peak was caused by the extremely positive lithium sentiment in those days, but the most impressive feat in my opinion is that Standard Lithium managed to carry on diligently during the downturn, especially as mentioned raising another C$11.8 million in April this year, which was a major hurdle to overcome, as it enabled it to construct the demonstration plant. All eyes are now on the testing and the upcoming PFS, which, if positive, could likely result in a construction decision by Lanxess, which will be a major catalyst in my view.

3. Lithium

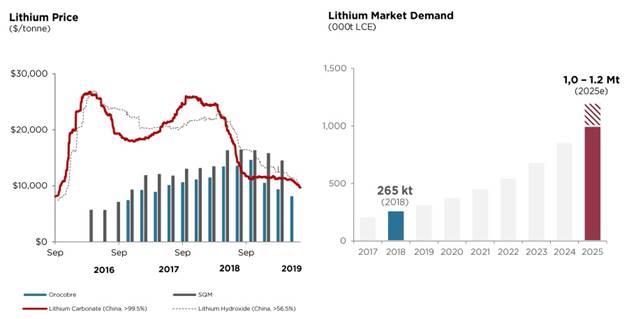

The market for lithium, and more precisely lithium products, isn’t a transparent one, as there are no central exchanges for this metal. There is a variety of contracts, ranging from spot to long term, and several organizations try to crystallize something of a credible pricing out of this. I view the long-term contract prices as most viable, as these are the large scale agreements between miners and converters (mostly in China), which is ultimately the price deck Standard Lithium will be dealing with when going into production. The best source so far for me is the presentation of Lithium Americas, combining spot and contract prices from Orocobre and SQM:

As can be seen, despite lowering lithium product prices, spot or contract, there is no lack of optimism with producers when estimating market demand, based on ongoing electrification of society, including electric vehicles. There are reasons for this.

The global market for battery chemical lithium is likely to remain fairly balanced for the next four to five years with supply rising to meet increased demand from electric vehicles. However, recent attempts by established brine producers to expand production in Chile have failed to materialize, owing to governmental, technical and environmental concerns. Recent increases in lithium chemical production have been fed by hard-rock producers in Australia, though these are currently entering a constrained growth phase, as almost all of the existing conversion capacity is being utilized.

This could be a very important aspect which Morgan Stanley, with probably the most bearish stance on lithium product pricing today, is overlooking. To be fair, the firm also brings in good points, as the likelihood of slowing down GDP growth and lower EV subsidies in China. It will be interesting to see which fundamentals will drive lithium product pricing for the next years. The durable/renewable energy paradigm shift isn’t going away anytime soon. A short note on fuel cells, which are on the rise in logistics, in case you are wondering about this (source): “hydrogen fuel cells offer a potentially very clean, energy dense and easy to recharge energy source for vehicles and other systems, but are currently complicated, expensive and dangerous to operate. In comparison, Lithium-ion batteries, although less energy dense and slower to recharge, are as clean, much cheaper, easier and safer to handle.” So it will take many years before fuel cells will solve safety issues before they can think of overtaking lithium-ion batteries, in my opinion, and potentially make a serious dent in lithium product demand. After discussing the outlook on lithium products, let’s have a look at the Lanxess project.

4. Lanxess Project

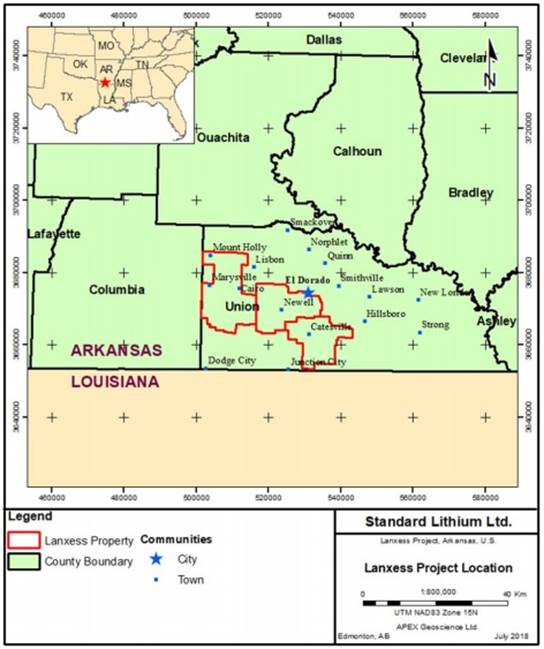

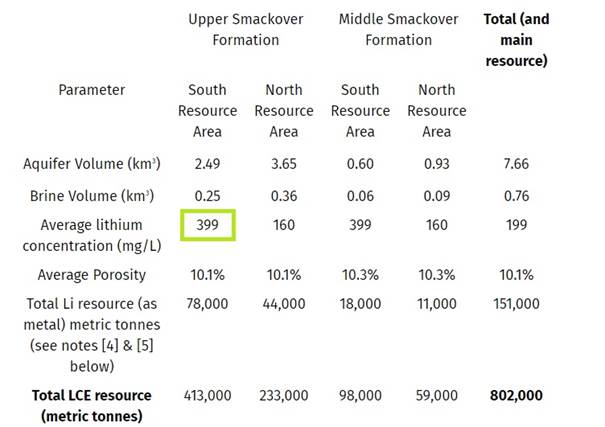

The Lanxess project is situated in southern Arkansas as part of the Smackover Formation. The Smackover Formation is a porous and permeable limestone aquifer that hosts large volumes of mineral-rich brines and hydrocarbons at great depths, starting from about 2100m, and about 50m thick on average. Its brines are currently the one of the largest sources of bromine in the world, but the brine also contains lithium—estimated to range from 150 to 500 mg/L.

The Lanxess operations consist of 150k acres land, 10k brine leases/surface agreements, 250 miles of pipelines, 61 brine supply/reinjection wells and three bromine processing plants. Around 500 people work at the plants, which produce about 6 billion gallons of brine annually. Lanxess owns the infrastructure 100%.

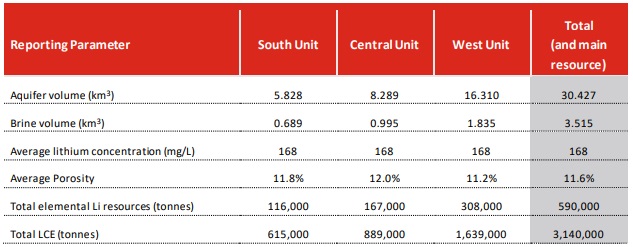

In 2017/2018 Standard Lithium conducted geochemical exploration on the land leased by Lanxess. The distribution of the brine samples collected included all brine distribution sample points (i.e., 24/26 brine supply wells, feed-brine and tail-brine from the South, Central and West bromine plants). Brine from the brine supply wells contained an average Li concentration of 164.9 mg/L Li. The main Inferred resource is estimated at 3,140kt Lithium Carbonate Equivalent (LCE) at the Indicated category.

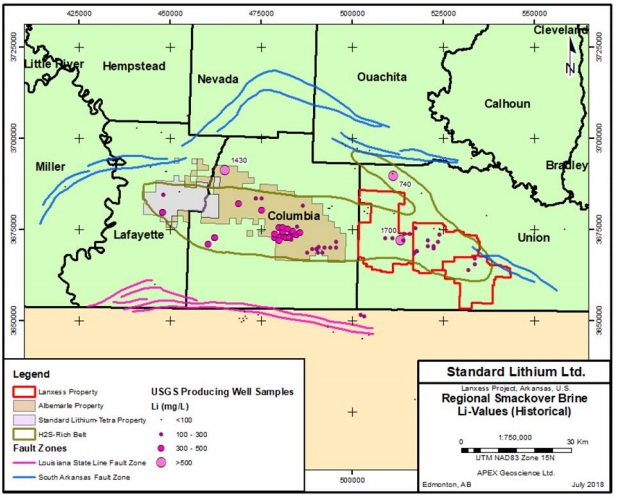

Standard Lithium has an option agreement with NYSE-listed Tetra Technologies (NYSE:TTI) on 27,000 acres of brine leases themselves; see the light pink colored area to the left at Lafayette (the red outlines are Lanxess owned):

The company has completed a maiden Inferred resource on the Tetra property of 800kt LCE, of which a large part is at a significantly higher grade compared to the Lanxess resource (168mg Li/L):

As a consequence, Standard Lithium is eager to add the best part of this resource to production after nameplate production is reached, more on this later.

Standard signed a term sheet with Lanxess in November 2018. The MOU as the basis of a potential future definitive agreement is binding until the completion of further development phases and more comprehensive agreement. Assuming the various milestones are adhered to, the MOU is exclusive and binding for a period of five years (until May 2023). Standard Lithium has paid an initial US$3 million reservation fee to Lanxess to locate and interconnect the lithium extraction pilot plant, to secure access to tail brine produced as part of Lanxess bromine extraction business and to provide logistics and other support required to operate the pilot plant with additional fees and obligations in the future (subject to certain conditions).

Compared to more traditional brine and hard rock projects, the Lanxess Project would require fewer steps in its development and especially less time given no additional drilling is needed, permitting is reduced to adjustments of existing Lanxess licensing agreements and no extensive infrastructure is needed either. Management estimates that in case of a construction decision in H2 of this year, commercial production could be achieved in H2, 2022, encompassing a total five-year timeline. This compares favorably to various other well-known projects:

- Lithium Americas – Cauchari-Olaroz: 11 Years (2009–2020) from initial resource work to estimated start of commercial production;

- Orocobre – Olaroz: 7 Years (2008–2015) from initial resource work to first commercial production; yet to achieve nameplate capacity;

- Lithium Power International/Bearing/Borda Group – Maricunga: 12+ Years (2009–2021+) from initial work to earliest production;

- Nemaska Lithium – Whabouchi: 10+ years (2009–2020); yet to finalize last part of funding

Although introducing the concept of a new recovery method in lithium operations isn’t always met with the most enthusiasm of investors as mentioned in the introduction, as commercial viability isn’t an easy feat here, Standard Lithium certainly is very serious in its endeavors. It not only put together a management and advisory team consisting of a number of heavyweights in the finance-, lithium-, lithium extraction- and development space, as mentioned earlier. Standard Lithium also raised C$43 million in the last two years, of which a bought deal of C$11.8 million in April 2019, which was in my view very impressive considering the pretty subdued sentiment for lithium since the summer of 2018.

Most of this last raise was needed to advance the construction and installation of the industrial scale demonstration plant as it needs to be called legally, in order to test the all-important economic viability and scalability of its direct lithium extraction process, which is called LiSTR. The LiSTR direct extraction process has already gone through bench scale, batch mini pilot, and continuous pilot scale, and will soon be trialed onsite at demonstration scale, where it is assembled now:

Positive test results of the LiSTR demonstration plant are the proof that Lanxess needs in order to finance and construct the entire project. Testing the process at this scale isn’t just a matter of simply scaling up the earlier used set-ups. These smaller stage pilots aren’t economic, and this last demo phase aims at turning the entire process into a commercially viable one. Of course, if there wasn’t any sight at viability when designing the method on the drawing board, there was no use going through all these steps, but Lanxess has seen enough positives to give Standard the opportunity to use its sites as one big experimenting area, and outline a potential JV.

Additionally, Standard Lithium has developed a second complementary technology called SiFT, which is a continuous fractional lithium carbonate crystallization process, the last stage of producing Li2CO3, which has already gone through bench scale and prototype pilot scale, and engineering is underway for a pilot scale plant to be built in Q4. The testing of this SiFT plant isn’t crucial for Lanxess, as conventional methods are easy to obtain and apply, at higher costs, still rendering the project viable if needed. Notwithstanding this, both Standard and Lanxess are very interested in the potential optimization this SiFT plant could provide.

The LiSTR demonstration plant is fully funded throughout construction via the financing this past spring with construction now completed by ZETON in Ontario, Canada, one of the global leaders in pilot plant construction, and the delivery and installation of this plant at the Arkansas project is expected late Q3 2019. The SiFT plant isn’t fully funded yet, the company estimates about C$5 million is arranged, and another C$5 million is needed, plus another C$1 million for further optimization.

This is not all, after both plants are constructed and commissioned, management estimates another C$15–20 million is needed to improve, run and test both plants for 12–18 months, as there are always teething problems, and extensive optimization programs are already designed, to potentially improve economics further. Standard aims at commissioning the demonstration plant in October this year, and believes it will have enough testing data at the end of Q1 2020 to complete a Pre-Feasibility Study (PFS) in Q2, 2020. Lanxess will base a construction decision on this PFS, and this is planned for Q3, 2020, with construction following shortly afterwards.

Standard Lithium takes on the risks and cost of all process construction, testing, optimization and viability, the economic studies including recently announced Preliminary Economic Assessment (PEA) and the mentioned PFS, and also brings in 27,000 acres of greenfield brine leases it holds an option to in southern Arkansas to the JV. Lanxess brings in 150,000 acres of brine leases, three operating chemical plants, hundreds of miles of pipelines and dozens of production and disposal wells, permits, and most importantly has announced it will finance, build and operate the final commercial processing plants, and has committed to a 100% off-take agreement. Final terms of the JV are not yet announced, as they still need to be negotiated, depending on the test results and PFS. When all the terms and conditions are met for a commercial build and going into production, Standard Lithium is entitled to a 30% interest in the JV, meaning it will receive 30% of future net cash flows. Standard also has the potential to increase its JV ownership to 40% based upon achieving certain milestones.

On June 19, 2019, the company announced the results of its PEA at the flagship project. The project has a staged build-out (three phases in five years planned), and aims at full nameplate production of 20,900t LCE annually. The final product lithium recovery is about 90%. Standard Lithium plans to produce battery-quality lithium carbonate as well, which sets them apart from a number of competitors that only manage to produce technical quality lithium carbonate. The economics indicate a pretty robust project, at a capex of US$437 million an operation can be constructed with an after-tax NPV8 of US$989 million and an after-tax IRR of 36%, based on an average long term LCE price of US$13,550/t. I viewed this base case price as high, as it was based on a three-year average, which is not very realistic in the lithium product realm. However, based on current LCE spot prices of about average US$11,500/t, after-tax figures would still come in economic, as I will show later on, and convinced me of the robustness of economics. Depending on successful testing, of course.

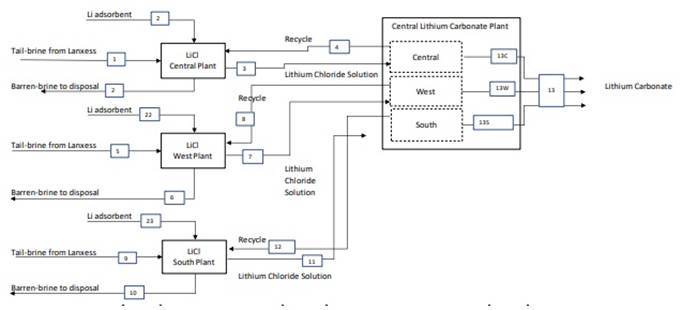

Standard Lithium’s objective is to produce battery-grade lithium carbonate from the tail-brine that exits the LANXESS bromine extraction operations. There are three bromine extraction operations that will be used for lithium extraction (South, Central and West). Each facility will have its own primary lithium chloride extraction plant, which will produce purified and concentrated lithium chloride solutions. These solutions will be conveyed, via pipelines, to one location (Central Plant) for further processing to the final product, which is lithium carbonate.

The tail brine is produced as part of Lanxess’ bromine extraction business. The brine is extracted from wells and the brine is transported to three processing plants through a network of pipelines. The spent de-brominated brine is then pumped back down into the ground through reinjection wells:

The project focuses on the 150k acres part of Lanxess’ land operations. The region is home to North America’s largest brine production and processing fairway. Southern Arkansas is seen as a business-friendly jurisdiction to be developing this project given its well-documented resource, large existing commercial brine production and ideal location with significant infrastructure, power, water, a skilled workforce and easy access to the Gulf of Mexico.

The lithium extraction process takes advantage of the fact that the brine leaves the bromine process heated at approximately 70°C. This means that no additional energy is required. The process can reduce the time required for lithium extraction from 12–18 months (compared with the evaporation ponds) to hours and is capable of producing a high-purity lithium chloride (LiCl) solution for further processing towards battery-quality lithium carbonate. The combination of these unit operations represents a novel flowsheet with its inherent risks, of course.

Here is the technical description of the process taken from the PEA, for readers with interest in recovery tech:

“17.1.2 Lithium Extraction Process The key element of the production of purified lithium chloride solution is the selective lithium extraction process. The process includes mixing of the pre-treated tail-brine with a fine-grained, solid, ceramic powder adsorbent that selectively adsorbs lithium ions from the tail-brine. The adsorption process is carried out in two sequential loading reactors. Additional base (caustic or ammonia) is added to the loading reactors during the lithium extraction process to maintain the desired pH conditions. The lithium-depleted barren brine is separated from the loaded adsorbent slurry using submerged microfiltration (0.1 to 10 μm) membrane units. The lithium-loaded adsorbent solids are continuously removed as a slurry from the loading reactor. The adsorbent is washed with water in three (3) stages of counter-current decantation thickeners. The washed and thickened adsorbent is pumped as a slurry to a stripping operation.

17.1.3 Lithium Adsorbent Stripping and Regeneration Process Lithium loaded, and washed adsorbent is contacted with dilute hydrochloric acid in a stripping reactor. The stripping process generates lithium pregnant strip solution (PSS). The PSS is separated from the barren adsorbent in a thickener. The adsorbent is washed with fresh water in three (3) stages of countercurrent decantation thickeners. The washed adsorbent is recycled back to the lithium loading stage. After washing, the PSS has a high ratio of lithium to the sum of the other dissolved metals and contains 3-5 g/L of lithium. This lithium chloride solution is sent to further purification.”

Standard Lithium recognizes the aspect of risks accompanying the development of new recovery methods, and I asked CEO Mintak a few questions, in order to get a better understanding of things. First up was why he thought he would be successful with his new process, after Tenova and POSCO more or less have been testing into eternity.

Mintak: “We have successfully tested and scaled our direct extraction process at lab/bench scale >100x to a batch, and then continuous operating mini-pilot > now beginning installation of a 100X larger continuous operating industrial-scale demonstration plant (1/100 commercial scale). Both my partner Dr. Andy Robinson and I were with Pure Energy previously and have been working on direct extraction processing for a number of years. Without going into a long diatribe, the fundamental challenge overlooked by technology developers is they are trying to force a process on to the project. Our approach is that project drives the process. We have had the luxury of unlimited access to brine and production data since we started the project as Lanxess processes and reinjects approximately 20 million gallons of brine every day. We have been able to take thousands of gallons of brine to do process testing without the expense of exploration or permitting.

“We take a wholly different approach than Tenova Bateman, POSCO or any of the other extraction developers. Our core philosophy is again the project drives the process. Lithium extraction from brine is not the challenge, there are a number of ways that work but the project drives the selection of the appropriate process. Brine chemistry, access to water, cost of chemical reagents, permitting and re-injection, access to power and if required natural gas, just to name a few. We are also using equipment and processes already in use around the world (even at very large commercial-scale), so fortunately it is not all that experimental.”

I was wondering what the most likely scenario would be for Standard Lithium in the long run, could Lanxess choose to buy Standard outright after successful testing and an economic PFS satisfies their demands?

Mintak: “The JV as currently agreed between LXS and SLL is 70/30 in favor of LXS, with an option, subject to certain milestones, for SLL to achieve up to a 40% ownership. LXS has committed to project finance, no dilution for SLL. LXS has also committed to 100% of off-take. LXS will build and operate the plants. The likely scenario, if we are successful, is that LXS will choose to make more niche lithium compounds that may produce higher margins. The JV and MoU we have signed are built on battery quality lithium carbonate.

“We are proceeding on the project focused on successfully achieving the proof of concept on the LiSTR extraction process and delivering a positive PFS in a timely manner, which will then allow us to complete a definitive agreement and form the joint venture for commercial development. Of course along the way, as a publicly traded company, the acquisition of Standard Lithium is another scenario that could occur. But I would caution that it is upon us to demonstrate the LiSTR process works as we believe and at a competitive level near or better than our peers.”

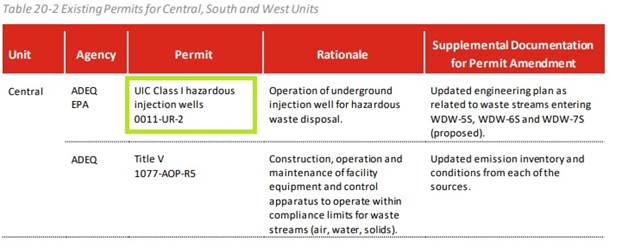

Could there be any issues with permitting, despite being planned as an integrated part of Lanxess operations, located on their facilities?

Mintak: “As the project is by and large already fully permitted for commercial brine production and chemical processing, we expect to face little in the way of permits other than construction permits like electrical, storm water etc. Water and extraction rights are all in place with Lanxess. The project has been in production for more than 50 years.

“The contemplated commercial build of the project would fall largely under the existing permits held by LXS and by and large be within the fence of their existing operations. The brine is already flowing at a commercial scale, 6 billion gallons annually. Water for processing and other industrial use is already allocated under existing rights held by LXS. All three existing production facilities are located outside nearby city limits and are not subject to local planning and zoning ordinances. Union County does not regulate industrial siting and construction activities. Any modifications required to existing permits we anticipate no longer than 3–6 months. A fraction of the time an EIS or EA take.”

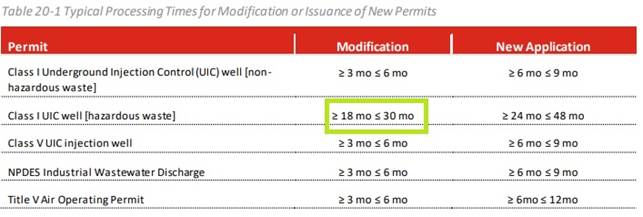

However, the PEA mentioned the following tables:

With the following modification periods:

CEO Mintak had the following to say about this, as there appears to be a few UIC Class I hazardous injection wells:

Mintak: “We do not foresee any modification to the hazardous waste permit as the extraction process is not introducing any new materials/chemicals to the final tail brine. Analysis from the demo plant brine post lithium extraction will be used to confirm this.”

We also talked about the optimization of brine for lithium, when will this take place and into how much improvement could this potentially result regarding economics?

Mintak: “The first stage of optimization will be on the extraction process, to optimize the opex and find efficiencies there. Once a PFS on the tail brine model has been completed and FEED (= optimization) work is underway we would look at the brine feed and well field optimization. We wouldn’t necessarily chase better economics, rather opportunities for a significant path to increased production as it could generate more cash flow.”

So the extraction optimization will be included in the PFS? If Lanxess makes a capex budgeting and construction decision based on the PFS, doesn’t mean increasing production afterwards that capex will need to be increased too?

Mintak: “Increased production would likely be a linear capex increase.”

You talked about increased brine production on the Lanxess claims, how much more production could be feasible if you can disclose? When could the Standard 27,000 acres come into play here, will this be at the end of LOM or before that, increasing production and increasing NPV?

Mintak: “The PEA considers a three-stage build out of a commercial operation over five years, So the earliest that the 27,000 acres of leases would be added for production would be at least five years. We will, however, be advancing the 27,000 acres with a PEA ourselves, then a PFS afterwards, likely reflecting an increased NPV. I would be speaking outside of my comfort zone by adding a certain number of tonnes to the total without a PEA on the 27,000 acres but 50% additional capacity would be a starting target point for us.”

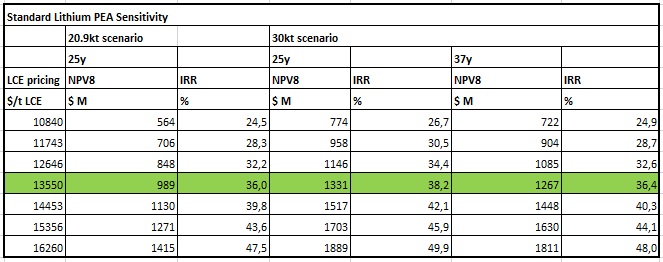

As a newsletter writer I am not constrained by legal limitations on forward looking statements, and took the liberty to estimate calculations on an additional 9,100t LCE to come up with a rounded 30kt LOM annual production, in two scenarios: a prolonged one and one with increased production and linear increased capex:

In my estimates the larger operation is slightly more economic for IRR, as the additional cash flow in the early years (less discounted) is offset by the additional capex, compared to the no capex longer LOM, with larger discounts in the additional years of production. I have been very conservative with the NPV8, taking into account that management indicated to me that they expect a lot from optimization programs for brine and processing. As can be seen, the project economics hold up at current LCE prices of about US$11,500/t, but also at a US$10840/t LCE price, as I consider about 25% after-tax IRR as a minimum for lithium projects.

Notwithstanding these simple scenarios, there is more to this expansion concept, leaving some question marks.

Who will be paying which part of capex? What is the difference between the Lanxess acres and the Standard acres for economics? Do the JV terms also apply for the Standard acres? Aren’t these Standard acres more difficult to develop as they aren’t part of the current Lanxess production area, and need new wells, infrastructure, etc.? As a consequence, isn’t the Lanxess resource, despite the lower grade, much more efficient to add as a bolt on PFS scenario?

Mintak: “Upon the formation of the JV (subject to the proof of concept and positive PFS) the JV will assume all costs, with Lanxess having committed to funding the JV at the initial Lanxess project (150,000 acres). The future expanded production would be the responsibility of the JV company. Whether LXS continues to fund the JV for production at that point has not been discussed in detail yet and is at least five years out.

The 27,000 acres are greenfield and will involve drilling wells and installing the infrastructure, so capex would shift from piggybacking on the existing brine production but adding brine volume with higher-grade lithium will also improve opex, those numbers need to be quantified and qualified in a PEA, but we will be able to do that with the demonstration plant as we have access to significant volumes of brine from the area through agreements with regional oil and gas producers that have wells that perforate the Smackover formation.”

So it seems to be the same concept, except that Standard probably has to come to an agreement with Lanxess on land ownership and future additional infrastructure to transport any future LiCl to the central plant.

On a final note, I always like to see for myself where the subject of analysis stands regarding their peers, not in the least for determining future valuations. In this case, Standard Lithium doesn’t really have comparable peers in the mining field as it is more of a technical/chemical company, but most inputs for such a comparison are valid across the field of lithium juniors, so this resulted in the following tables:

And:

As can be seen, Standard Lithium already has quite a high market cap/attributable NPV ratio at the moment despite having completed just a PEA when comparing to others, but this can be explained by Standard having a far lower capex obligation in the JV (zero), being future part of a much larger operation, and them being relatively close to a financing decision, combined with strong funding efforts for their pilot/demonstration plants. Accounting for the staged development, they are actually priced for perfection at the moment in my view, as at US$11,500/t LCE the NPV8 for Standard is US$212 million, which is C$282 million.

The current market cap is C$71 million, which means about 25% of NPV8 at PEA stage, although I would like to discount for the staged development, meaning it will take a while until the project is at nameplate capacity and cash flows. Also take into account the C$15–20 million that needs to be raised in the not-too-distant future. Therefore I view the current valuation at 50% of NPV8, which seems high for a PEA project when comparing to peers, but is in my view adequately representing the risk of a new recovery method combined with very low funding requirements for Standard, a very strong partner, good jurisdiction, short timeline to funding decision, and upside from optimization and more resources. The Standard Lithium thesis is all about the new recovery method in my view. If they succeed, and in this case it seems they have a significant chance, Lanxess will likely take care of everything else, and I can see this double from here when construction is on its way a year from now as the main risk has been taken away in that case.

6. Conclusion

Standard Lithium is a special case, as it takes on a new recovery method for lithium, something that has been tried for many years by large industrial players. However, considering its novel and research-driven academic approach and apparent ease regarding raising capital and arranging a JV with giant Lanxess, it seems something is different here. If the company manages to derisk this new method by successful testing and completing a positive PFS, Lanxess will probably not hesitate too long and fund construction. With Standard having more of a technical/chemical project, being in the backyard of Lanxess itself, it is likely that the project will see less extensive timelines and ramp-up issues compared to conventional brine operations. The upside isn’t huge but pretty decent in my view, but in about six months’ time we will see if it will be derisked significantly or not, and if so, barring a stock market crash or LCE prices dropping way below US$10,000/t, we are likely in for a re-rating. I like my chances here.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

The Critical Investor Disclaimer:

The author is not a registered investment advisor, and currently has a long position in this stock. Standard Lithium is a sponsoring company. All facts are to be checked by the reader. For more information go to www.standardlithium.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor’s disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

( Companies Mentioned: SLL:TSX.V; STLHF:OTCQX,

)