Source: Peter Epstein for Streetwise Reports 07/30/2019

In this interview, CEO Philip Thomas of A.I.S. Resources discusses his company’s prospects in the lithium and manganese sectors with Peter Epstein of Epstein Research.

A.I.S. Resources Ltd. (AIS:TSX.V) is a lithium brine exploration and development company with projects in Argentina, and is setting up a potentially lucrative manganese (Mn) trading operation in Peru that could generate positive cash flow this quarter and well beyond. The market seems to like the near-term cash flow aspect; the share price took off on very heavy volume on July 23 based on this press release.

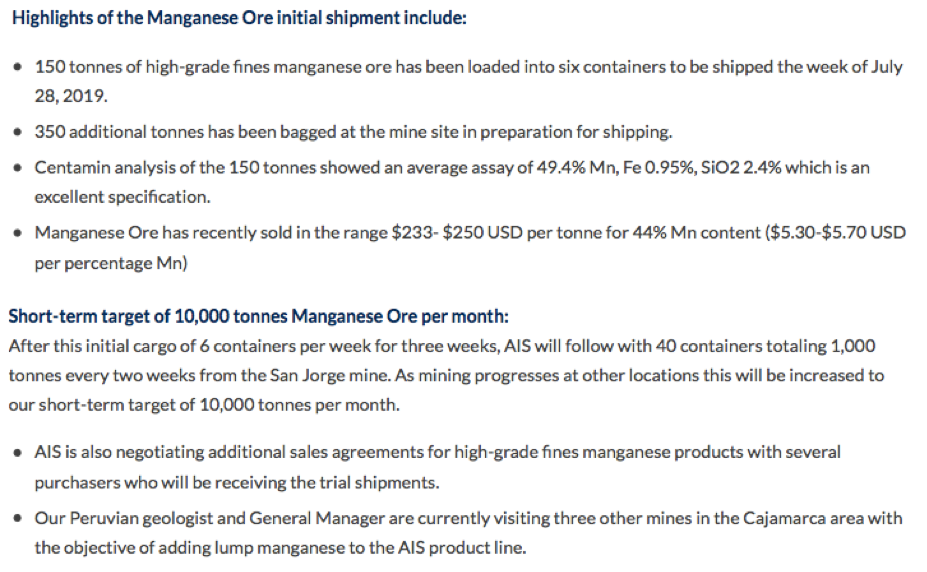

What on earth was in that release to cause a doubling in the share price to CA$0.13 per share (it has since pulled back to CA$0.09)!?! The prospects for near-term cash flow, possibly significant amounts relative to A.I.S.’ market cap, that’s what. Although just 150 tonnes of high-grade (49%) Mn fines ore has been loaded into six containers to be shipped the week of July 28, the press release discusses plans for 10,000 tonnes/month within about six to nine months.

Based on current Mn pricing and expected costs, A.I.S. should be able to make approximately US$100/tonne operating profit, or US$1 million per month (if /when selling 10,000 tonnes/month). In a sense, that’s all readers need to know. If the company can generate US$1 million per month, the current market cap of CA$7.3 million will prove to be way too cheap.

However, of course, there’s a lot of risk between a single shipment of 150 tonnes that has not even hit the water yet, and consistent delivery of 10,000 tonnes/month! For an update on the company’s lithium (Li) segment, and more on manganese trading, I spoke with CEO Philip Thomas. The following interview was conducted by phone and e-mail over an eight-day period ended July 24.

ER: Please give readers the latest update on your lithium project(s) in Argentina.

PT: We have two active locations in and around the Guayatayoc and Vilama Salars in northern Argentina, an area known as the Puna region. We sampled Vilama and obtained good surface results (145–200 parts per million [ppm] Li), but we have yet to complete geophysics or drilling.

Guayatayoc has two concessions, Guayatayoc Mina and Guayatayoc III. We received a drill permit for Guayatayoc Mina (Mina) and drilled to a depth of 407 meters (407m). A number of small aquifers were encountered and lithium at low concentrations. The magnesium and potassium ratios were in a favorable range for future production.

Four more drill holes are planned (approximately 1 kilometer apart), which should allow us to deliver a maiden resource estimate in 1H 2020. If the drill program is successful, we will redrill the holes to turn them into 25-centimeter diameter production wells, and start a feasibility report.

In addition, we are examining other salars in Salta and Catamarca provinces that might be suitable for exploration.

ER: Can you explain further why you believe the A.I.S. project is more advanced than many lithium brine projects in Argentina?

PT: The A.I.S. team has many years of experience and is one of the few that have built large pilot plants and operated them. In 2004-8, when I was CEO of Admiralty Resources we gained a lot of experience in exploration and production, building ponds and lithium production chemistry. This extensive knowledge was advanced with work in a private capacity in the Pozuelos, Salinas Grandes, Pocitos, Hombre Muerto and Incahuasi salars.

At Guayatayoc we have processed enough brine in a pilot plant to produce 99.2% ithium carbonate at 77-82% yields, which has proven difficult for most other players. We have a complete capex and opex budget for a 10,000 tonne/year plant. Now we need to prove a lithium flow rate of 700 liters per minute and an average lithium grade of 250 ppm or higher.

ER: When is your final US$2.25 million payment due? How do you plan on paying that considerable amount?

PT: We are currently negotiating with Ekeko SA for an extension of the option on Mina and Guayatayoc III until February 2020. Between now and then, we are hopeful that our manganese business will accelerate so that we can generate cash flow to fund the $2.25 million payment and exploration to feasibility stage.

ER: Turning to manganese, why manganese and why Mn trading?

PT: Ninety-three percent of Mn is used in steel applications, but that number is slowly declining as lithium-ion batteries use more and more manganese. Mn is cheaper than cobalt and due to its multiple oxide states, it offers superior performance. Mn is prolific in Peru, where there is the ideal volcanic and sedimentary environment to host high-grade deposits.

In Peru, we are looking for Mn miners of a reasonable size and we are assisting them with mine engineering, sales, documentation (which is exceptionally complex in Peru) and logistics support.

ER: Can you discuss at a high level what approximate tonnage you might be able to move and the potential economics of the operation?

PT: The main drivers of profitability are:

(1) Grade of manganese—the global benchmarks are 37% and 44%, as measured by Platts

(2) Lumps, chips or fines

(3) Transport—vessels (break bulk 10,000+ tonnes) or containers

(4) Impurities (less than 5% iron (Fe); 10% SiO2; carbonates)

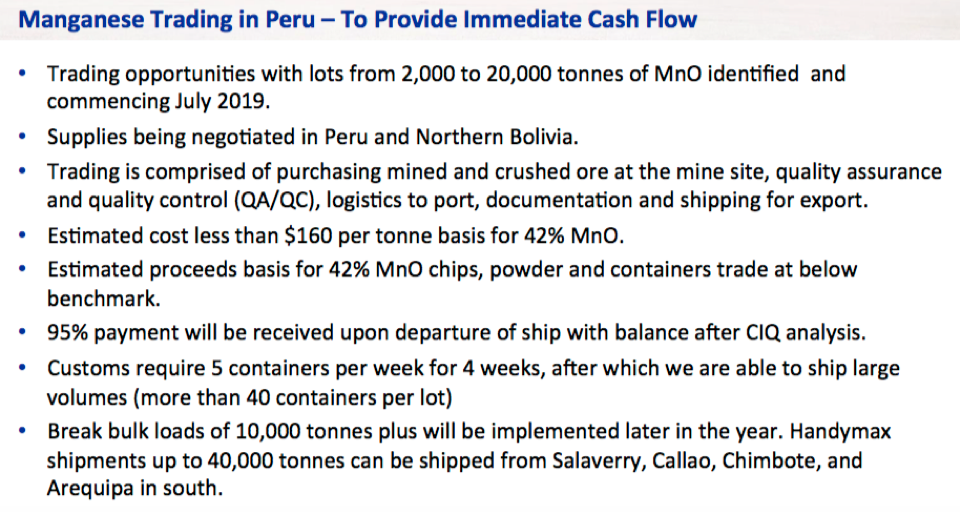

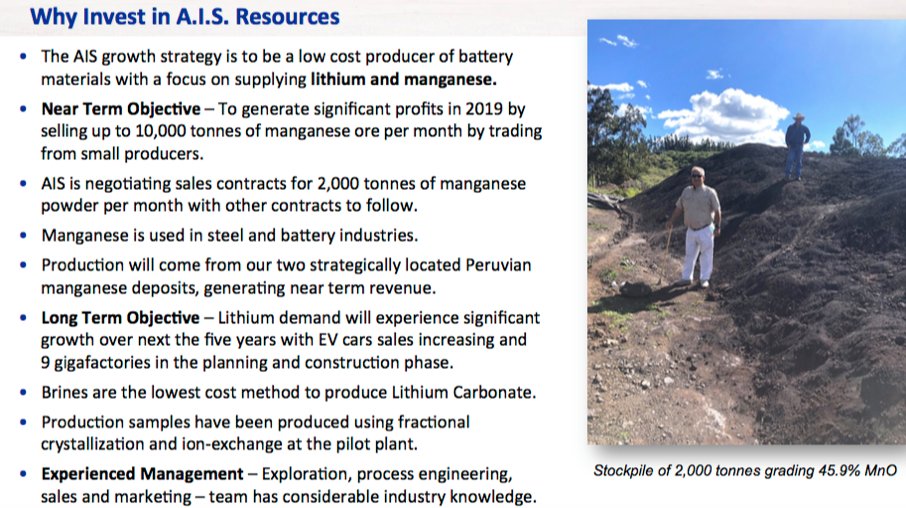

Our latest press release reported that we delivered 49% Mn. At the San Jorge mine in Peru our contract miner now has two open pits with the objective of opening six. Production is ~500 tonnes/week, per pit. We are also reviewing additional properties under contract mining, joint venture (JV), or operating ourselves scenarios in the Cajamarca region. The aim is to take monthly lump production up to 5,000 tonnes per month, transported in break bulk vessels, and then 10,000 tonnes per month within about six to nine months.

The economics are simple—it costs US$140–160 a tonne to buy the ore, transport it to Lima, and ship it to Tianjin or Qinzhou in China. The Platts benchmark for 44% Mn—lumps in break bulk, CFR Tianjin, is US$5.90 per 1%. For fines in containers and bags it’s US$5.35 per 1%. So, at a 49% Mn grade, we receive $262 per tonne, less costs of say $160/tonne = ~$100/tonne operating profit. The larger the tonnage exported, the lower the cost/tonne as wages get spread over a larger production base.

ER: Is manganese trading a relatively short-term opportunity, or potentially a medium- to longer-term play?

PT: Good question. It’s a longer-term play. Initially we will be focused on the steel industry, but we will be ready to move to the battery industry as the opportunity arises. We have the chemical expertise to build electrolyte and cathode Mn materials, or contribution materials such as Mn sulphate used in cathode manufacture. Although only 10% of the global Mn market by volume, high-purity Mn makes up about 40% of global market value. It’s used in batteries, series 200 stainless steel, specialty alloys, fertilizers and trace nutrients.

ER: You are operating in a country (Peru) that many readers may not be familiar with. What can you tell us about working in Peru?

PT: Peru is probably the most advanced mining country in Latin America. Unlike Argentina, it has a single mine concession approval system and a well-documented system for dealing with approvals for water, roads etc. Peruvian people are very work-orientated and want to get things done rather than mañana (I’ll get to it tomorrow).

ER: You have described to me how important it is, both morally and ethically, and for sound business reasons, to hire local laborers and managers. Can you talk about that?

PT: Poverty is common in rural areas. In the Cajamarca region (population 200,000), while the town is flourishing, workers in surrounding towns are subsistence farmers. Therefore, if the men can secure work in the mines, it significantly supplements their family’s otherwise small income.

By maximizing local employment, we minimize local issues such as water, dust, noise, etc., because everybody buys into the project. We have seen investors from Asian countries who didn’t understand the cultural significance get banned from mines, kicked out of the country.

ER: What are the biggest risks to achieving the meaningful cash flow from manganese trading that A.I.S. is expecting?

PT: Having spent 17 years working in Latin America, and having first worked in Peru in 2012, I have a good understanding of the risks.

We have analyzed our main risks as follows:

• Product pricing: we have a production contract for fines and soon will have extended the product range to include lump. This will improve the price we receive and allow us to target new customers. The Mn ore 44% lump bulk product was as high as US$10 per 1% of grade in April 2018 and as low as US$7 this month. Oversupply is something we need to keep an eye on. However, we have the ability to change production volumes on a week to week basis, so we can react quickly with no penalties.

• Product Supply: we have one contract miner and several other negotiations and due diligence programs running to ensure that we meet our production target of 10,000 tonnes a month within six to nine months. Then, in 2H 2020/2021, a significant increase above 10,000 tonnes.

• Product Sales: There’s significant interest from new suppliers in the market. We may have to discount our product until we prove our ability to deliver, but the discount will be modest. We are having discussions with Chinese, Korean and other buyers.

ER: Why should investors consider buying shares of A.I.S. Resources?

PT: The company has adopted a low capital investment approach to mining and is focused on growing its retained earnings. As you are aware, we expended a lot of capital in Guayatayoc to build an asset, yet fell afoul of the administrative approval system in Jujuy province, leading to a delay in getting our drilling approved.

The board has supported my approach to being innovative in terms of trading and having a focus on cash flow. As we grow our cash flow from Mn trading we can redeploy it in Peru or, if sentiment in the lithium market improves, we can get busy again in Argentina. Mn trading gives us a lot of flexibility and will hopefully enable us to make that final $2.25 million payment.

If readers believe my math—that A.I.S. Resources can potentially generate about $100/tonne of Mn traded—then it all comes down to volume, logistics and timing. If we can ramp up to 5,000 tonnes/month next quarter, on our way to 10,000 tonnes, then our current valuation is very attractive. (July corporate presentation. Latest press releases).

ER: Thank you Philip, very interesting update. Good luck with your new Mn venture. I will follow up with you and your team next month.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about A.I.S. Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of A.I.S. Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned no shares of A.I.S. Resources and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts, financial calculations, etc., or for the completeness of this interview or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein’s disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Graphics provided by the author.

( Companies Mentioned: AIS:TSX.V,

)