Source: The Critical Investor for Streetwise Reports 04/15/2019

The Critical Investor explains how a recently acquired gold project in Nunavut may completely change the company.

1. Introduction

Sometimes you see juniors switching from metal to metal, trying to catch the flavor of the day, riding the hypes with basically worthless projects. So now diamonds are out of favor, and gold is back in vogue, could it be that Margaret Lake Diamonds Inc. (DIA:TSX.V; M85:FSE) is pulling the same trick with its latest acquisition? There are two important factors opposing this possibility in my view at least. First and foremost there is exploration legend Buddy Doyle who didn’t only discover diamond deposits but also 15 Moz of gold deposits in the past. This all-star geologist has a serious reputation to lose. Furthermore he isn’t the person to give away anything easily, as I experienced first hand when I tried in vain to assist with a financing of a UK fund at the end of 2013 for a cash-strapped Amarillo Gold, where he was the CEO at the time. The money was on the table, but he refused to surrender to the pretty tough terms. I found it to be a pretty bold action at the time, but I also have to give him credit for being adamant on the share structure.

The second factor is the new Kiyuk Lake gold project itself, located in southern Nunavut, being acquired at the moment. Although nordic and remote, not too often do you see drill results like 249m of 1.6g/t almost from surface, and a series of good results from 35–188m, meaning there could be significant open-pit potential. With Doyle as VP Exploration endorsing this project, the company seems to have a good chance of finding out what exactly this potential could be.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. The company

Margaret Lake Diamonds Inc. (TSX.V: DIA) is a Canadian junior mining company focused on mineral exploration in Canada’s most prolific nordic mining districts. The company is earning in an 80% interest in the soon-to-be flagship high-grade Kiyuk Lake Gold Property located in southern Nunavut. The company is optioning it from Cache Exploration (CAY.V), another tiny explorer, which can’t raise the necessary cash to advance it meaningfully. It also holds interests in two diamond exploration properties in the Northwest Territories, the first being the Margaret Lake project located adjacent to Mountain Province Diamond’s Kennady North project and close proximity to Gahcho Kué, the newest Canadian diamond mine owned by De Beers and Mountain Province Diamonds. The company also has a 60/40 joint venture with Arctic Star Exploration Corp. (TSX.V: ADD) to explore the Diagras property, which is composed of 23 claims totaling 18,699 hectares located in the prolific Lac de Gras diamond field. Management is fully focusing on Kiyuk Lake now, and so will I in this article.

Both jurisdictions have solid scores on the all-important Policy Perception Index (PPI) in the recently published 2018 Fraser Survey of Mining Companies. The PPI is the most important figure of this survey, as it indicates the mining friendliness of a jurisdiction, which encompasses corruption, permitting, speed of administrative processing, politics, local sentiment, etc. Nunavut scored position 16 out of 83, and Northwest Territories 14 out of 83. I do find it an interesting development that the number of jurisdictions is decreasing every year now since 2014, as before this year it was increasing.

The management team of Margaret Lake Diamonds is an interesting collection of characters. Leading the pack is new President and CEO Jared Lazerson, coming on board at December 17, 2018. I know Jared as the CEO and wild and visionary deal maker, marketing specialist, trader and money raiser of advertiser MGX Minerals. Sometimes he is a tough act to follow and MGX Minerals is going through a rough period now as it faces delays on its wastewater pilot plants, but he did raise over $30 millin for MGX in two years, so at the very least he has backing of some powerful players. One of the first things he did when coming on board was buying 4 million shares of Margaret Lake Diamonds in the market, so it is safe to say that management has skin in the game here.

As mentioned earlier, VP Exploration Buddy Doyle is somebody who doesn’t really need much introduction, but to be fair he led the team that discovered the Diavik Diamond deposits in the 1990s, and was the former exploration manager for Kennecott/Rio Tinto. Mr. Doyle is recognized by his peers in the exploration industry as an authority on diamond exploration and kimberlite geology, and has authored/co-authored numerous papers on these subjects. He was awarded the 2007 Hugo Dummitt Award for excellence in diamond exploration. Before all this, he was a key member of the team that discovered the Minifie deposits, that formed for the most part the monstrous Lihir Mine at Papua New Guinea, currently owned by Newcrest, which produced 0.955 Moz Au in FY 2018.

Another remarkable person on the board is Don Huston, who worked for a decade in the family exploration business, and has had a 20 year long career after this in putting together and promoting mining deals for the last two decades or so, one more successful than the other. He is a director of three other junior mining companies, and lately he also has been involved in a blockchain deal called CUV Ventures, rolling out a blockchain-based credit card application on Cuba. Another director is Darryl Sittler, a former NHL player and 1989 inductee to the Hockey Hall of Fame, also director of Frontline Gold and Wallbridge Mining. From my experience, these former sport legends in business usually have an excellent, slightly different network in the circles of power and finance, and can be a real value-add. The company has appointed Dr. Michael Reimann (PhD) as CFO, which is a familiar name from MGX Minerals.

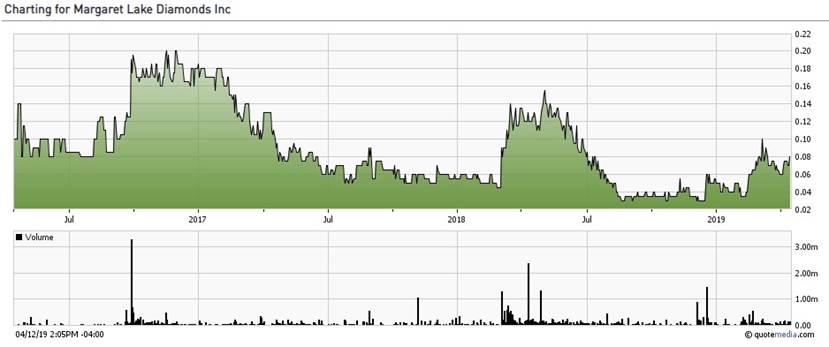

Margaret Lake Diamonds has its main listing on the main board of the TSX Venture, where it’s trading with DIA.V as its ticker symbol. With an average volume of about 53,990 shares per day, the company’s trading pattern is moderately liquid at the moment, and I expect this to improve when drilling is about to start.

The company currently has 54.69 million shares outstanding (fully diluted 63.65 million), 8,96 million warrants (C$0.20 exercise price, expiring on April 16 and May 31, 2021) and 2.05 millin options on average @ C$0.14, most of them expiring after October 1, 2021. Margaret Lake Diamonds sports a very tiny market capitalization of C$4.38 million based on the April 15, 2019 share price of C$0.08. The company is looking to do a financing very soon, looking to raise about C$2 million in order to get its exploration program for Kiyuk Lake going.

The company is basically controlled by management, as 45% is held closely by management, Board of Directors, insiders and former insiders with no intention of selling anytime soon. Former CEO Paul Brockington, who made a fortune by early investments in diamond plays like Diamet and Aber, owns directly and indirectly 11.6 million shares (21.3%), CEO Jared Lazerson owns 4 million shares (7.5%). Both are holding on to their shares, according to management.

Share price; 3 year time frame

The new gold story has slowly started to find its way to the market since mid-February as can be seen by the first uptick in the chart, and rightly so as a share price of C$0.035 isn’t very useful to raise cash. I expect several catalysts in the coming weeks/months, so this could prove to be a nice entry point, especially considering the exploration potential, which I will discuss in the next paragraph.

3. Projects

The Kiyuk Lake gold project will be the sole focus of this article as mentioned, as management does the same now. On a side note, diamond exploration is many times more difficult as the diamond hosting rocks (kimberlites) are usually present in relatively small kimberlite pipes, which have to be detected first, and after this the exploring company has to actually hit diamonds, which are of course discrete, very tiny gems, widely spread in kimberlites, needing wide diameter drilling, etc. The costs versus chances of success are much more disadvantageous compared to (precious) metal exploration, which is already difficult enough as it is, with an estimated one to three mines put into production out of every 1,000 exploration projects.

The Kiyuk Lake gold project is located in Nunavut, and its huge land package consists of 70 contiguous mineral claims encompassing over 59,000 hectares and offers year-round accessibility to a 35-person base camp. Although Kiyuk is situated very nordic, according to management there is no winter break needed for exploration work, and there is hardly any overburden, which makes things easier for drilling. Also important to note is the number of significant projects and mines in this region, owned by familiar names (Agnico, Auryn) and much more nordic as well, although closer to water:

Location Kiyuk Lake, Nunavut; Source: Cache Exploration

Kiyuk Lake has seen quite a bit of exploration in the past, beginning with Newmont Mining in 2008 and most recently Cache Exploration in 2017. This has resulted in over 13,000 meters of core drilling and identified four mineralized zones and five additional high priority target areas that have yet to be drill tested. Mineralization has been traced across a 13-kilometer strike length and remain open in all directions. When I looked into the history of Kiyuk Lake, I noticed a few big names and companies being involved over the years. Quinton Hennigh basically discovered it, and was the geologist handling the project for Newmont and Evolving Gold, and Hennigh and Adrian Fleming oversaw the drilling for Prosperity Goldfields, to name the most important ones. Since Prosperity Goldfields, there have been three different owners, and Margaret Lake Diamonds will be the fourth in six years’ time.

This is a bit much in my view, so you might ask yourself, as I did, are we dealing with a recycled project here, doing the rounds again in the next potential gold bull market after being under the radar for several years? Not exactly, there is more to it. Newmont sold the project in 2008 as it parted with most of its exploration projects at the time because of a change in strategy. Evolving Gold picked it up, did extremely well by the way in a raging bull market at the time, and Kiyuk Lake was spun out into Prosperity Goldfields in 2010. Prosperity was quite active with its exploration program, but it ceased drilling in 2013 as the entire resource space entered one of the most severe bear markets ever seen after 2012. After this the project changed hands two more times, as Northern Empire and Montego owned it as well. Cache Exploration came along after four years, and bought the project in 2017 as it was sitting shelved. This buying was predominantly caused by Robert Bick, VP corporate development, who knew Kiyuk Lake from his time as the CEO of Evolving Gold, and didn’t forget about it.

Cache Exploration raised some money and drilled a number of impressive drill holes, but had difficulties raising enough money to provide the amount of drilling necessary to really advance Kiyuk Lake towards a resource in a reasonable timeframe. And let’s not forget, drilling up north is expensive, to the tune of $600–750/meter, as everything has to be flown in and out at Kiyuk Lake.

I talked to a few people with close working knowledge of Kiyuk Lake, and the general message that was conveyed was the gold was there, although hardly economic yet because of the remote, nordic location with no infrastructure. The intercepts and grades so far indicated a very interesting project, and they believe it has great exploration potential. They believed for an economic project in that location, 2Moz @ 1.8-2g/t Au open pittable is necessary at current gold prices. On a side note: many people look at nordic projects like Back River from Sabina Gold & Silver (SBB.TO) with a mill feed grade of 5.7g/t Au for comparison, but let’s not forget Back River has a high strip ratio of 7.2:1 as well, and Kiyuk Lake seems to have much less than that at the Rusty Zone, although it still is early stage on just one target.

So the bottom line seems to be for Kiyuk Lake that the gold seems to be there, but it is expensive to explore, so it advances relatively slowly with each drill campaign. It is up to Margaret Lake Diamonds now to take Kiyuk a step further (and hopefully more) and deliver the first resource estimate of hopefully 1Moz Au, on its way to the coveted 2 Moz Au.

Cache Exploration CEO Jack Bal, who is a colorful character in the space, wasn’t so patient and decided to explore cannabis adventures in Q4, 2018, and went looking for a JV partner on Kiyuk Lake. As a consequence, Margaret Lake Diamonds came in to buy it as it was willing to test the exploration potential further.

Here are the highlights of the terms of the JV with Cache Exploration:

- To earn an initial 50% interest in the Property, Margaret Lake has agreed to issue 5,000,000 common shares of the company to Cache Exploration within 10 days

- To invest C$150,000 through the purchase of 3,000,000 common shares of Cache at a deemed price of $0.05 on a private placement basis within 30 days.

- The company will also make a cash payment of $100,000 to Cache on or before the first anniversary of the effective date of the agreement .

- To incur exploration expenditures totaling $3,000,000 on or before the third anniversary of the agreement.

- Margaret Lake also has the right to acquire an additional 30% in the property, for a total of 80%, by making a one-time cash payment of $5,000,000.

As Margaret Lake is still finalizing the agreement with Cache, and the completion of the transaction is subject to Exchange acceptance, there can be no assurance that the transaction will be completed as proposed or at all. But given the fact that both parties have known each other for many years, it seems very unlikely for this transaction not to be completed.

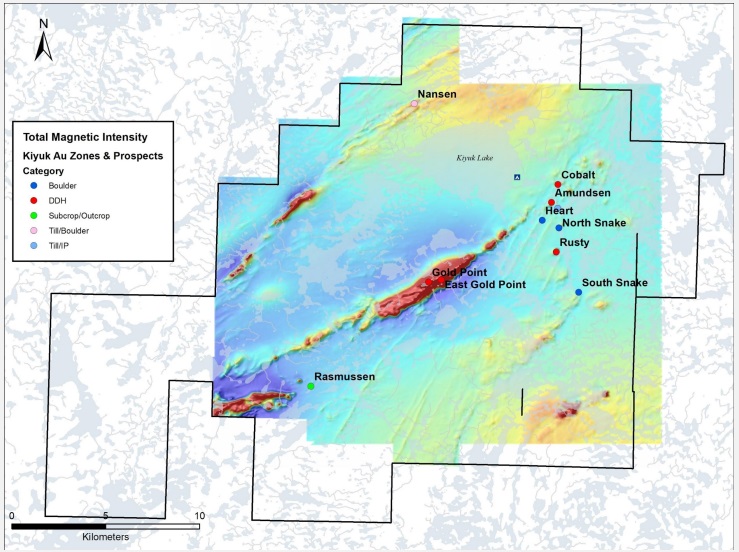

Let’s have a closer look at the project itself now. Mineralization has been found (by diamond drilling) at four zones so far, called Rusty, Gold Point/East Gold Point, Cobalt and Amundsen. Kiyuk Lake has many more targets, indicated by high grade grab samples/boulders, spread out over an area of about 20km, and leads management to believe that it is a genuine district play. The Rusty Zone has been explored the most so far. The following map showing the results of a magnetic intensity survey gives an indication of size:

Magnetics; Source Cache Exploration

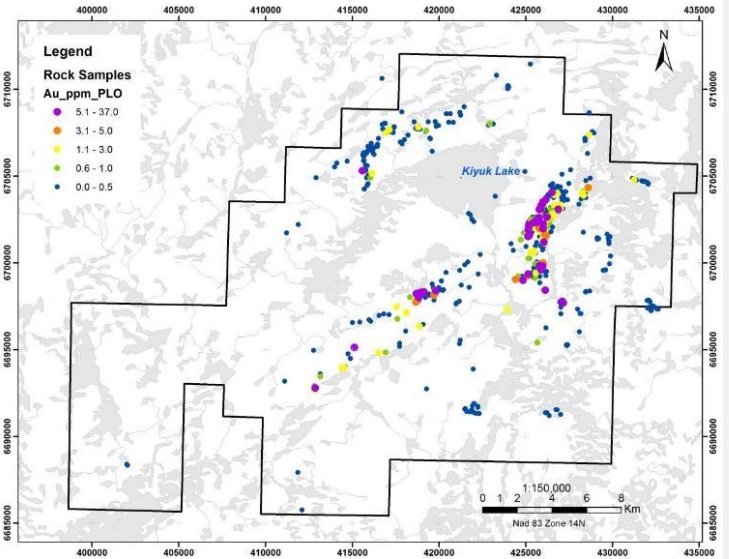

And this is a map showing the sampling results, indicating a serious amount of 5–37g/t Au samples spread out over the mentioned area of about 20km long, within this a strike length of 13km:

Sampling; Source: presentation Cache Exploration

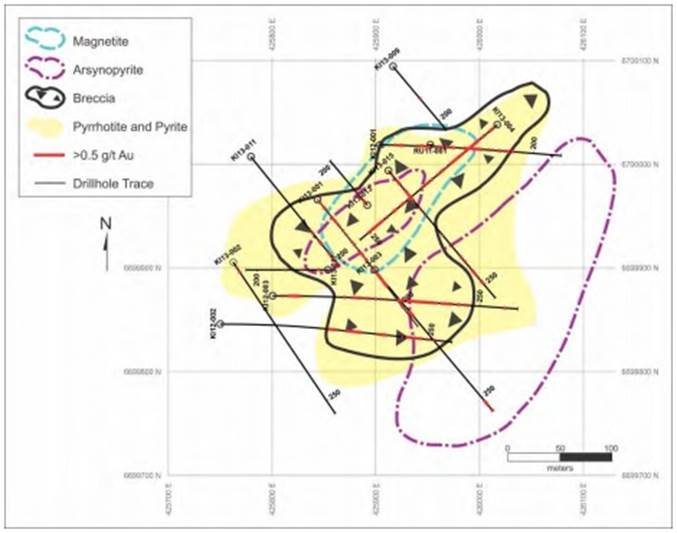

The geology of Rusty can be described as mostly pyrrhotite and magnetite, with arsenopyrite and pyrite in brecciated and altered sandstone. Most mineralization is found in vein and breccia systems. According to the internal 2013 Technical report of Prosperity Goldfields: “Gold mineralization on the property has been divided into three end members based on surface mapping and review of drill core: 1) brecciated pyrrhotite-rich sandstone (Rusty); 2) altered pyrrhotitebearing conglomerate (Cobalt, Amundsen, Airstrip, Bancroft, Rasmussen), and (3) altered pyrite and arsenopyrite-bearing polymictic conglomerate (Gold Point). ”

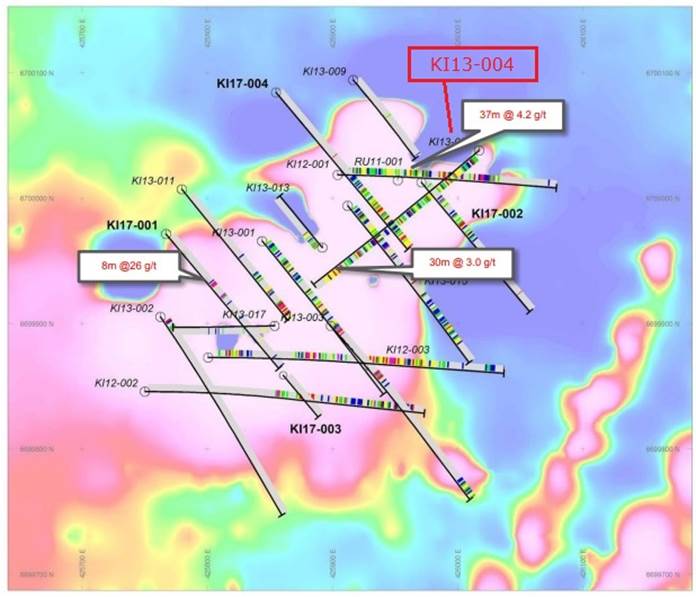

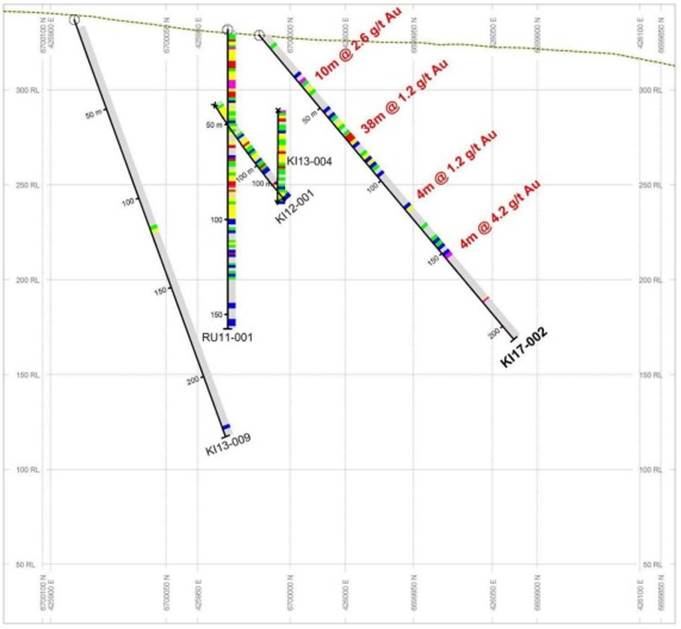

As most drilling hit substantial mineralization at relatively shallow depth, and grade didn’t increase sufficiently at depth to be economic so far, drilling never went deeper than 300m, although regularly drilling ended in mineralization. The highlights from the 2017 campaign of Cache Exploration delivered impressive results:

- 8m @ 26.48 g/t gold (Au) from 108m, including 2m @92.76 g/t Au from 110m, in DDH KI17-001

- 38m @ 1.16 g/t Au from 58m, including 8m @ 3.98 g/t Au from 68m, in DDH KI17-002

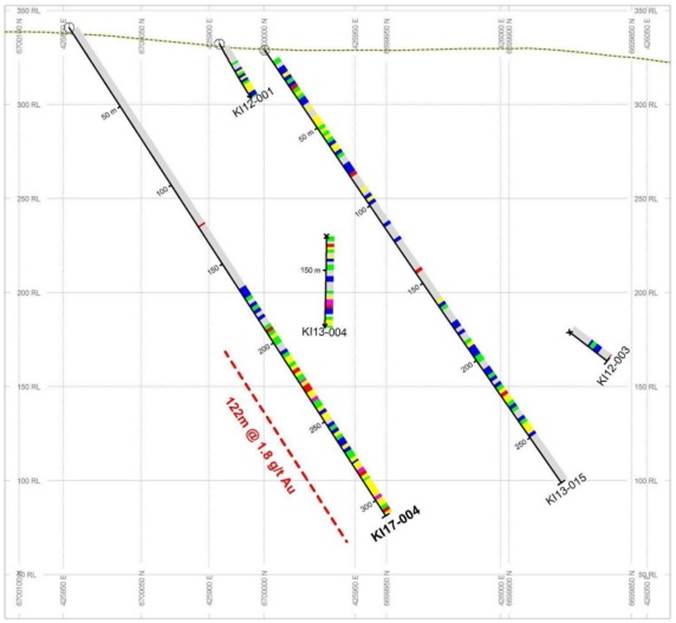

- 122m @ 1.82 g/t Au from 188m, including 15m @ 3.34 g/t Au from 294m, in DDH KI17-004

And an older hole from 2013 was also indicating potential:

- 249m @ 1.6 g/t Au from 8.2m in DDH KI13-004 (no cut-off)

Other 2017 results include 38m @ 4.2 g/t Au from surface and 36m @ 4.95 g/t Au from 134m. Historic results also have interesting highlights:

- 52.4m @3.27g/t Au from surface

- 35.9m @ 4.95g/t Au from 134.1m

- 61.5m @ 3.3g/t Au from 159m

- 24.1m @ 3.4g/t Au from 34m

According to the relevant news releases, these intercepts are not true width, and have not been verified recently by a qualified person as per NI 43-101 regulations. Notwithstanding this, there is no denying that these are all very interesting drill results, indicating solid resource potential. Considering the average grade, we should look at open pit potential, and this is usually limited to a depth of 200–250m. Economic open pit grade usually begins at 1–1.5g/t Au, and I can see this going to 2–2.5g/t for Nunavut like nordic regions. The geologists I talked to see 2g/t as a minimum grade for Kiyuk as well. Besides this, for underground mining, economic grade starts at 6–7g/t at US$1300/oz Au, and this far north it could go to 9–12g/t.

Next up is another magnetics map of Rusty, containing most drill holes at this zone (each coordinate is on a 100m grid to indicate size):

Source: presentation Cache Exploration

It can be concluded that mineralization is confined to a horizontally fairly limited envelope, predominantly within the borders of the magnetic anomaly. The following sections give an indication of presence of mineralization versus depth:

Source: presentation Cache Exploration

And:

Source: presentation Cache Exploration

According to the next schematic map it seems that the structure or stratigraphy is complex as in that many rock types come together at the mineralized zones. Mineralization however seems reasonably continuous:

Source: Internal Technical Report Cache Exploration/Prosperity Goldfields

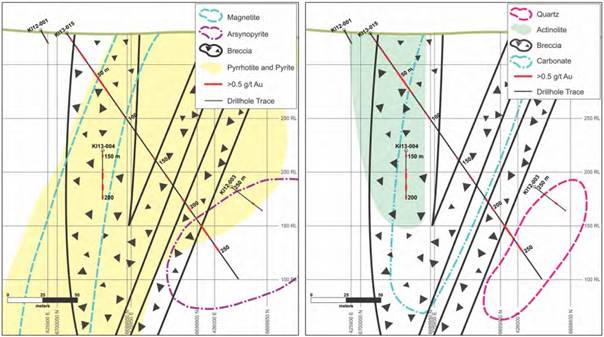

Figure 60 – Conceptual cartoon, based on core logging information, of the Rusty Zone outlining magnetite and sulphide zonation with respect to gold values. Arsenopyrite is found in the core of the gold zone but primarily on the outer edge of gold mineralization and out into the magnetic low to the east of the Rusty Zone. The breccia zone encompasses a majority of gold intersections. Magnetite makes of the core of the zone with a sulphide halo extending around the magnetite core.

It can be seen that most mineralization is confined to the breccia zone. Breccias usually have something of a pipe shaped envelope, and often occur multiple times in the same area forming a cluster, like VMS deposits. So far exploration has defined one, at Rusty.

Source: Internal Technical Report Cache Exploration/Prosperity Goldfields

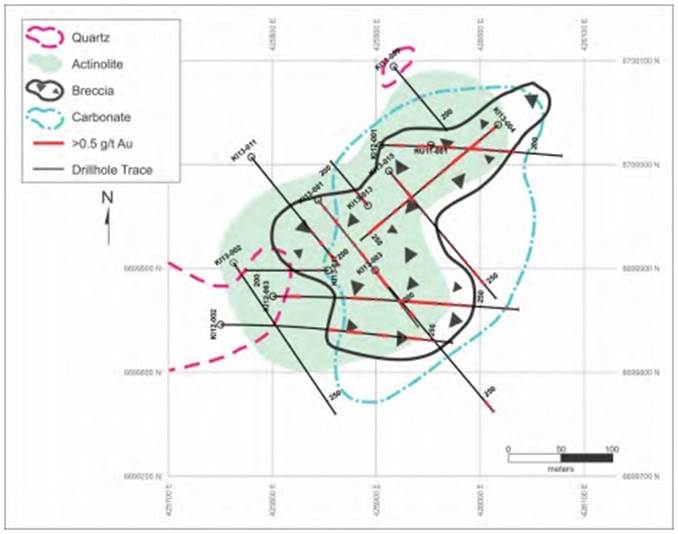

Figure 61 – The core of gold mineralization in the Rusty Zone is defined by actinolite and carbonate alteration as seen in this conceptual cartoon based on core logging. Quartz alteration and veining is found on the periphery of the Rusty Zone.

Source: Internal Technical Report Cache Exploration/Prosperity Goldfields

Figure 62 – Cross sections showing mineralization and alteration zonation in the Rusty Zone with respect to gold grades above 0.5 g/t Au. Breccia zones are important for gold mineralization and show a strong correlation in this cross section. The sulphide halo surrounding the magnetite core can be seen. Gold occurs in both the magnetite and sulphide zones. Arsenopyrite is often found in the magnetic low to the east of the main Rusty zone. Gold is intersected in these zones rich in arsenopyrite. However, grades are commonly below 0.5 g/t Au. Actinolite and carbonate alteration make up the primary alteration minerals seen in gold zones. Carbonate (calcite and dolomite) does have a broader alteration halo as shown in the cross-section. Quartz alteration is seen distal to the main breccia bodies and gold zones.

The gold mineralization starts at surface at Rusty, more to the northeast of the drilling area (see magnetics map), and seems to continue at depth. When looking at the drill results, maps and sections, I guesstimate a global mineralized envelope of 4.5–5 million cubic meters (m3), with a specific gravity of 2.85t/m3 (per the internal technical report, p. 119) this results in 12.8–14.25Mt tonnage. At a conservatively estimated average grade of 1.6g/t Au, this would result into 0.66–0.74 Moz Au, every increase in average grade of 0.2g/t Au this would add 0.08-0.09 Moz Au. Margaret Lake Diamonds is aiming at 1 Moz Au for starters, and this doesn’t seem unrealistic. An average grade of 2g/t Au would be a good thing, and they are fortunate not to have a high strip ratio. I estimate this at 3-4:1 which is good, as the usual open pit strip ratio is more like 4-5:1. If the company does manage to get to a 1Moz @2g/t resource, I believe it has a solid base to build on from there.

And let’s not forget this is just the Rusty Zone, there are many more targets at Kiyuk Lake, some have seen some drilling, others haven’t. For example, at Gold Point/East Gold Point, the company also hit mineralization, although not as much as at Rusty, but still a good start:

- 64m @ 1.46 g/t Au from 35m, including 14m @ 3.12 g/t Au from 37m, and 10m @ 6.51 g/t Au from 248m in DDH KI17-005

And from historical drilling:

- 63.6m @ 2.84g/t Au from 148m

- 12m @ 2.4g/t Au from 120m

- 12m @ 3.9g/t Au from 163.5m

The Cobalt Zone also returned interesting first results, with a highlight of 21.3m @ 2.15g/t in DDH CS11-002. The Amundsen Zone was drilled by just one hole, and this generated 42m @0.97g/t from 170m. So there seems to be gold everywhere, it is more a case of finding the economic mineralized envelopes.

It is up to Buddy Doyle and his team now to plan an exploration program. CEO Jared Lazerson is raising money at the moment, and has applied for a Land Use Permit at its Kiyuk Lake Gold project located in southern Nunavut. Currently, Kiyuk Lake has a Type B water license that is valid until June 2022. The Type B license allows the company to access local water sources for camp and drilling use.

Upon receipt of the permit, the company plans to revitalize the existing exploration camp in April followed by up to 5,000 meters of diamond core drilling in the spring of this year. Ground magnetic surveys to further define high priority drill targets are also being planned. The drill program will focus on expanding the high-grade Rusty zone along strike and to depth as well as testing the highest priority drill targets.

6. Conclusion

Margaret Lake Diamonds finally switched from diamonds to gold with its new flagship Kiyuk Lake Gold project in Nunavut, and it might be a game-changing event. Incoming CEO Jared Lazerson knows he has quite a task on his hand up north, but he loves to explore and he told me he missed the adventurous exploration times in the bush with his dog and the helicopters, so he was eager to acquire the Kiyuk Lake Gold project and make plans with Buddy Doyle and the team. 1 Moz Au is a clear target for the maiden resource estimate, and doesn’t seem unrealistic at all considering the earlier results. Let’s not forget the very tiny market cap of C$4.38 million, even if not economic at the moment, a potential 1 Moz asset would be very unusual for such a low valuation, even as a leveraged play on gold, and there seems to be much more exploration potential at Kiyuk Lake. I am a curious follower of this interesting story.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclaimer:

The author is not a registered investment advisor, and currently has a long position in this stock. Margaret Lake Diamonds is a sponsoring company. All facts are to be checked by the reader. For more information go to www.margaretdiamonds.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor’s disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

( Companies Mentioned: DIA:TSX.V; M85:FSE,

)