Source: Rudi Fronk and Jim Anthony for Streetwise Reports 03/25/2019

Rudi Fronk and Jim Anthony, co-founders of Seabridge Gold, discuss Fed policies and what they mean for gold.

In our view, the gold story is getting much simpler and much more urgent.

Here is how we see it. The Fed cannot exit QE. QE is a failed policy. More QE is coming. Buy gold to preserve capital.

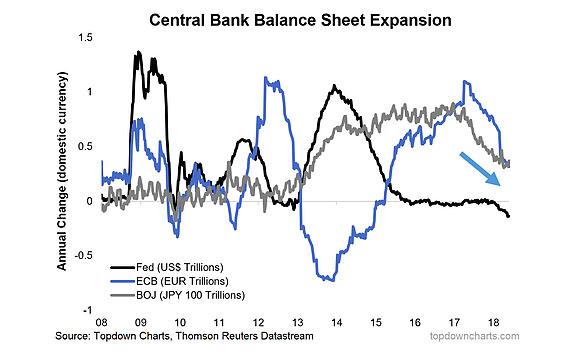

To combat the financial crisis of 2008/9, the world’s central banks created an enormous amount of new money…about $15 trillion…to restore liquidity to the banking system, stimulate demand and jump-start investment. The primary tool was QE…the purchase of financial assets with newly created money, mostly in the form of bank reserves. As central bank balance sheets have stopped growing, world markets have topped out and economies have begun to slow, clearly indicating their dependence on stimulative monetary policies.

Massive QE prevented a collapse of the financial system but the ensuing economic recovery was unusually slow as most of the new money went into speculative asset bubbles. Stocks reached historic high valuations relative to sales and GDP, interest rates went to 5,000 year lows but capital investment lagged and productivity growth fell.

The central banks knew they would eventually have to “normalize” monetary policy. The Fed began this process in December 2015, with its first of eight quarter point rate hikes…a historically slow pace of tightening….and also began reducing its balance sheet in 2017.

Last week, the Fed effectively halted its normalization policy. Three months previously, the Fed had expressed confidence that interest rates were still well below the “neutral” rate and would need to continue to rise due to the strength of the economic recovery. In December, the Fed had said its balance sheet reductions would proceed on “autopilot” at $50 billion per month. On March 20, all that was set aside. The Fed announced the end of normalization…no more rate hikes this year, the balance sheet reductions would taper beginning in May and terminate in September. This was the most abrupt policy about-face in the history of the Fed.

By any historical benchmark, the Fed’s new “normal” stance of monetary policy remains extremely stimulative. The federal-funds rate, currently between 2.25% and 2.5%, is just 0.25% when adjusted for long-term expected inflation. By comparison, the real rate was 2.75% at the end of the Fed’s last tightening cycle in 2006 and 4% at the end of the prior cycle in 2000. And the Fed will still hold more than $3.5 trillion in bonds in September, equal to 17% of gross domestic product, compared with just 6% in 2006.

What have we learned? Investors and the Fed have learned that the economy and the markets cannot cope with real normalization of monetary policy. Ten years of emergency stimulus have restructured the economy around record low interest rates and record levels of liquidity and debt. There is no going back. This was a surprise to the stock market, but not the bond market, which for months had been signalling that the economic recovery was weakening. Since March 20, Treasury rates at the long end have fallen precipitously, almost certainly forecasting a recession.

The most important lesson from this debacle is still just emerging. Not only can the Fed not exit its emergency monetary stance, but we are also now realizing that QE does not generate sustainable economic growth. In fact, it may weaken the economy while also encouraging excess debt and dangerously high asset valuations. And further, monetary easing is all the central banks know how to do; it’s their response to any and all problems.

The theory behind QE…that a higher stock market and lower rates raise demand and encourage investment…has, in our view, been conclusively refuted. We agree with Nomura’s Charlie McElligott who assesses the effects of Fed QE as follows:

- Low interest rates are (ultimately) deflationary, sustaining zombie-firms in a “liquidity-trap” that weighs on overall economic performance while also weakening investment.

- Low interest rates and QE are deflationary as you incentivize mal-investment and blow perpetual speculative-asset bubbles which (ultimately) correct and drive deleveraging—thus creating a “balance sheet recession.”

- As there is still a lot of debt-related “scar tissue,” you can’t push credit on a string. This then leads to quick “muscle memory” returns to a defensive posture: “If there is no return on capital, capital should not be deployed.”

So, what is next? The out-of-control growth in the federal budget deficit must be financed. In a world of declining trade and rising tariffs, purchases of U.S. securities by U.S. trading partners are no longer financing the U.S. budget deficit…foreigners have become net sellers. Remember that foreigners have provided the missing savings that have offset U.S. overspending. Meanwhile, the world economy is slowing rapidly, especially Europe and China, and this is beginning to affect the U.S. where corporate debt levels are now at record highs while debt quality has reached new lows.

The logic is building for a return to QE which will kill two birds with one stone…financing the budget deficit at lower rates and helping to prevent a wave of corporate bankruptcies.

Those who do not think another round of Fed QE is possible should consider the ECB, where the termination of its QE last December lasted only two months before it was announcing a return to TLTRO funding of commercial banks…QE by another name.

Imagine a new round of QE when investors know it does not support sustainable economic growth? Imagine that it is implemented to finance the Treasury and support zombie companies while Fed credibility is already at an all-time low. Where do you think the new money will go…into stocks and bonds or real goods and services and gold?

This article is the collaboration of Rudi Fronk and Jim Anthony, cofounders of Seabridge Gold, and reflects the thinking that has helped make them successful gold investors. Rudi is the current Chairman and CEO of Seabridge and Jim is one of its largest shareholders. Disclaimer: The authors are not registered or accredited as investment advisors. Information contained herein has been obtained from sources believed reliable but is not necessarily complete and accuracy is not guaranteed. Any securities mentioned on this site are not to be construed as investment or trading recommendations specifically for you. You must consult your own advisor for investment or trading advice. This article is for informational purposes only.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclosures:

1) Statements and opinions expressed are the opinions of Rudi Fronk and Jim Anthony and not of Streetwise Reports or its officers. The authors are wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the content preparation. The authors were not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the authors to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

2) Rudi Fronk and Jim Anthony: we, or members of our immediate household or family, own shares of the following companies mentioned in this article: Seabridge Gold. We personally are, or members of our immediate household or family are, paid by the following companies mentioned in this article: Seabridge Gold.

3) Seabridge Gold is a billboard sponsor of Streetwise Reports. Click here for important disclosures about sponsor fees.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.