Source: The Critical Investor for Streetwise Reports 02/25/2019

The Critical Investor explains why this company is one of his favorite holdings.

1. Introduction

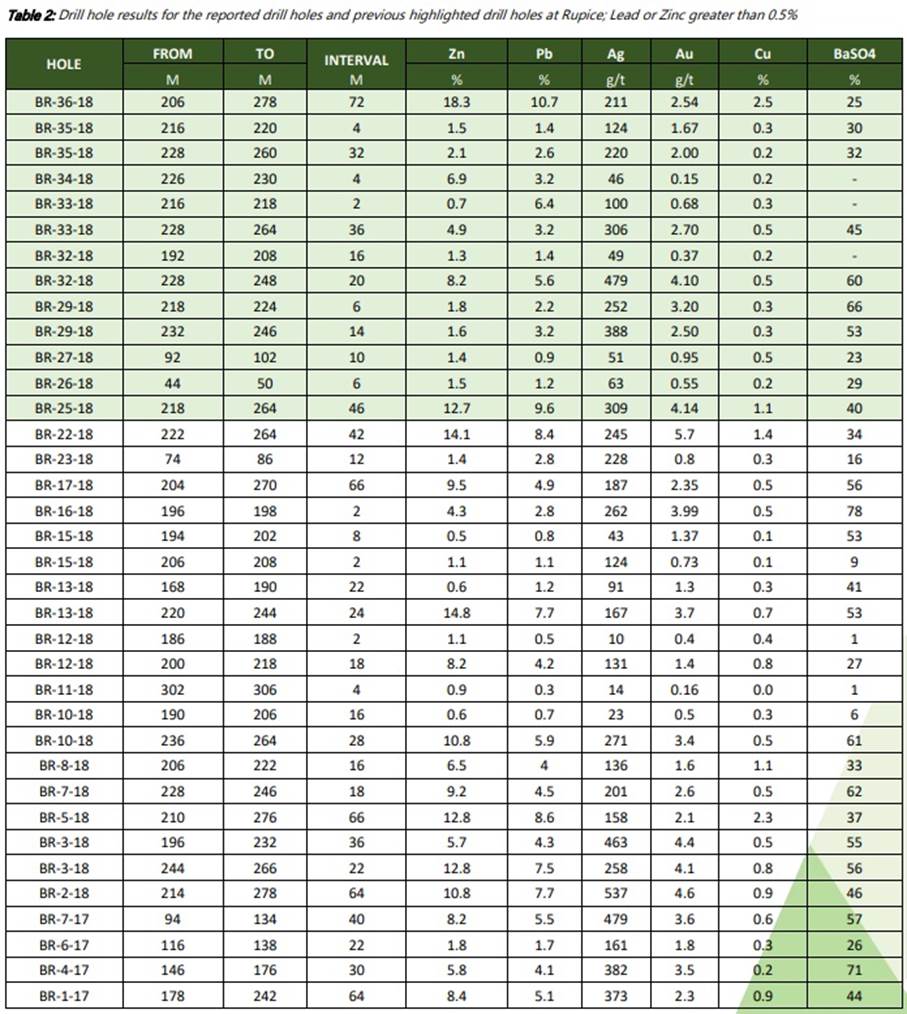

One of my favorite holdings, Adriatic Metals Plc (ADT:ASX; 3FN:FSE), is still under the radar for a lot of North American investors, being an Australia listed company. It is my strong conviction this is not really deserved, and this situation might potentially not last very long. As it is exploring Rupice, a very high-grade polymetallic project in Bosnia Herzegovina, Adriatic already produced several impressive sets of drill results during 2018. It didn’t stop there, as the company released, for example, hole BR-36-18, which intercepted a very thick zone of high-grade mineralization over 72m returning 18.3% Zn, 10.7% Pb, 211g/t Ag, 2.5/t Au, 2.5% Cu from 206m, and 46m at 25% BaSO4 from 216m on January 21, 2019.

These numbers already sound impressive just on their own for each individual metal, but the zinc equivalent at current spot prices would be a staggering 72m @ 49.5% ZnEq, and the gold equivalent an equally ridiculous 72m @ 31g/t. The gross metal value of such a hole is no less than US$1328/t. And it isn’t just one lucky strike, Adriatic has been pulling results resembling this since 2017.

Granted, the mineralized area isn’t very large, but the extreme grades bode well for a very economic project, potentially suited for a mid-tier producer. And the company isn’t done drilling yet. It has applied for (and was granted) a much larger area, including a potential extension of Rupice to the north, containing many large IP targets to the south. The company is awaiting approval on further drill permitting, but it is expected to be granted at the end of this month. Adriatic is fully cashed up and will explore most of these targets in 2019. What the end result will be in the form of a maiden resource estimate nobody knows yet, but I’m curious enough to do a guesstimate myself this time. It really is a gem in my view.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. Company

After the pretty extensive analysis of Kees Dekker, which I published in October 2018, I will touch just briefly on some company specifics. Adriatic Metals has its main listing on the main board of the ASX, where it is trading with ADT.AX as its ticker symbol. The company fully owns two polymetallic projects in Bosnia Herzegovina, its flagship Rupice project and the Veovaca brownfield project.

With an average volume of in excess of 228,437 shares per day, the company’s trading pattern is quite liquid. Its secondary listing is the Frankfurt listing, with 3FN.FWB for the ticker. Adriatic currently has 131 million shares outstanding (fully diluted 150.5 million), and 19.5 million options of which most are in the money, which gives it a market capitalization of A$108.36 million based on the February 22 share price of A$0.72. The company has an estimated cash position of A$14Mmillion at the moment, and has no plans to raise more cash soon. Management and the Board of Directors hold the largest position, about 30%. Director Paul Cronin is the single largest shareholder at roughly 18%.

Another meaningful shareholder (7.7%) is Sandfire Resources, a copper-gold producer from Australia. Its Degrussa mine is depleting fast without any potential of finding new ore in the vicinity, so it is looking for other assets. Apparently it has a strong focus on Adriatic now, as it tried to lift its holdings to 19.9%. Adriatic management wasn’t too pleased with this concentration of voting rights and prevented this from happening.

Share price Adriatic Metals; source company website.

As can be seen in this chart, the share price didn’t drop off after the first results in June 2018, and it took a while before it ascended further, as drill results came in slowly. But with every set of drill results confirming and expanding the very high grade mineralized envelope at Rupice, investor confidence rose further with it. The latest 10% decline didn’t have any fundamental reason, but was likely profit-taking according to Paul Cronin. Therefore, I consider this a buying opportunity.

3. Exploration

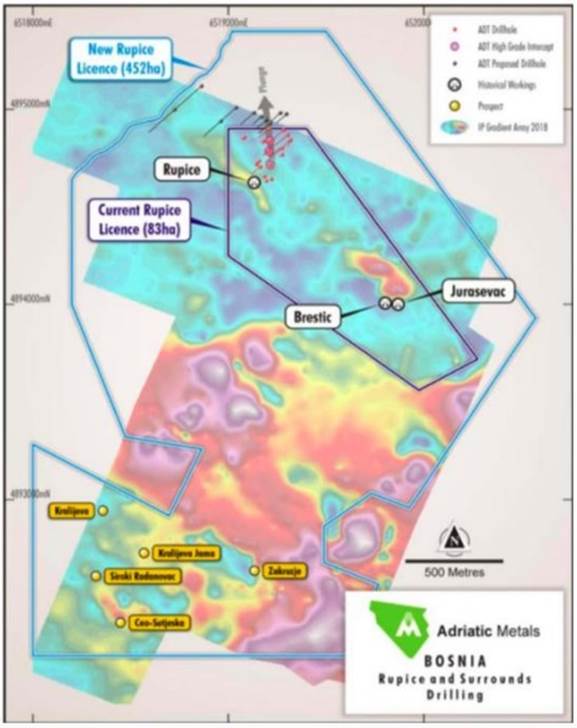

What is Adriatic exactly up to these days? The company is awaiting the extended Exploration permit for Rupice, after receiving the Urban planning permit on February 6, 2019. The Exploration permit is expected soon, within 1-2 weeks. The permitting system in Bosnia requires a scoping study or PEA for the application of an exploitation permit, which is not different from almost any other country; there has to be a mine plan. The company figured out that using its nearby Veovaca site 17km away, a currently uneconomic brownfield project hosting a former mine, would ease the application process, so eventual ore from Rupice needs to be hauled (or concentrated on site first) to an eventual mill and plant at Veovaca. A 2017 IP survey already indicated very interesting targets (red and magenta):

A deeper IP survey is planned to start in Q1 and will scan the recently expanded license to further define drilling targets on the concession for the 2019 drilling campaign. Management indicated to me that these targets will see the first drilling in May of this year. Historical data would suggest that mineralization is quite shallow but its findings from Rupice North is that shallower lower-grade mineralization is accompanied by higher grade at depth if the structural conditions indeed exist.

Of course, this is all for the future, after a deposit has been established. This is scheduled a few months from now, well into Q2. Adriatic is currently drilling at Rupice and Veovaca. According to management, heavy snowfall last month has slowed its progress temporarily but the company expects to have all four rigs operating on the northern plunge and the new zone to the South East. Adriatic will add two more rigs at JB after it has finalized the mentioned IP survey. It will penetrate deeper than the survey from 2017 and should help identify the mineralization deeper than 200m. Management expects to drill about 20,000 meters this year. The next drill results will be out in March btw.

So, Adriatic is in the middle of delineating a resource, and as a result of the drilling so far, it seems to be able to show a good impression of potential mineralization. Here is a table with the complete results, using the very low cut-off of 1% Zn+Pb, as the company wants to include economic values of silver, gold, copper and barite as well (in my view it could just use ZnEq cut-offs to simplify things, in- or excluding barite):

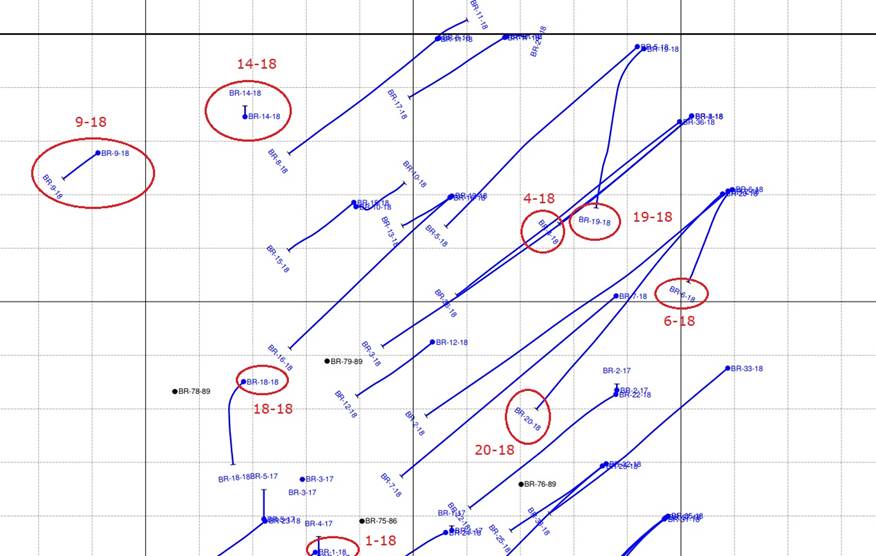

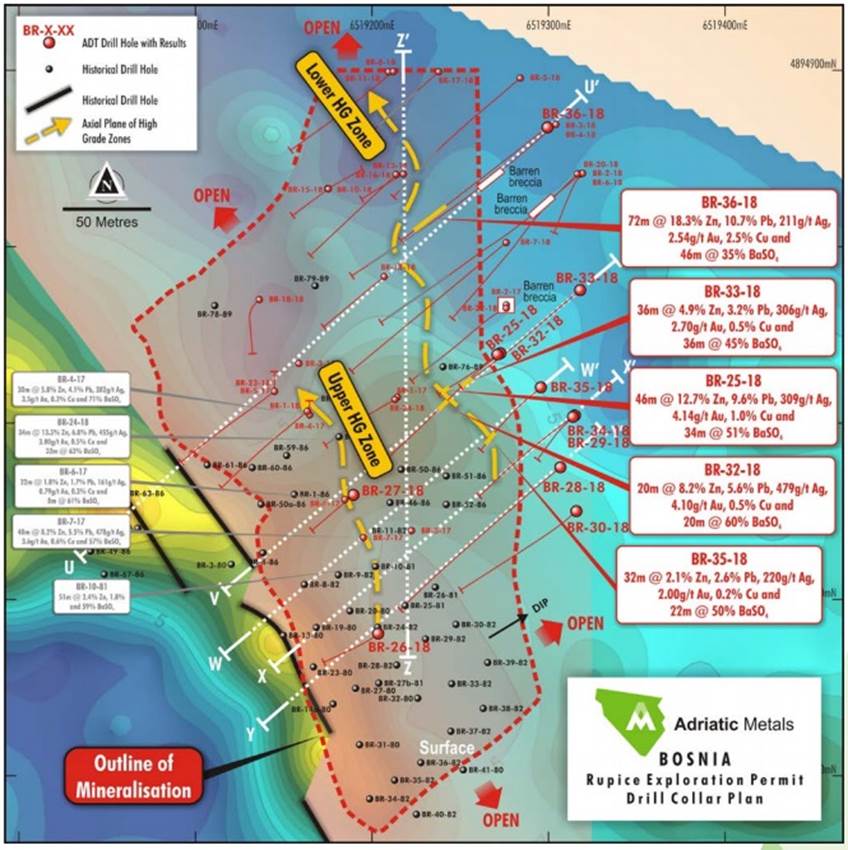

It is good to see it had not too many misses when delineating the potential resource, for last year these were holes 1, 4, 6, 9, 14, 18 to 21, 24, 28, 30 and 31. Most of these holes were to the far east across a probable fault, or to the west, where the mineralization thins out. I received this map with collar locations and directions from management to get a better impression:

Hole 4-18 and 20-18 probably missed the mineralized envelopes, and 19-18 and 6-18 probably just further defined the fault line. Hole 14-18 looked like a vertical one, going to a depth of 214.9m. It could be the western limit, but at that location it is possible that the mineralization is located just below that level, at least when looking at the long section to the north.

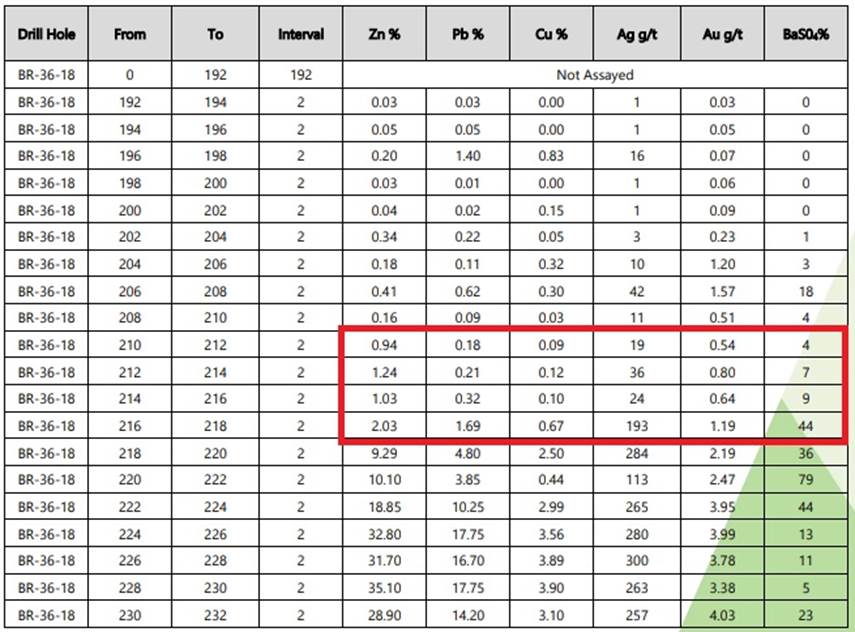

The benefits of a low cut-off can be seen in the next table, showing for example the assay intervals of hole BR-36-18, adding another 8m to the other, much higher-grade mineralization:

The mineralized envelope has been outlined in this well-known drill collar map:

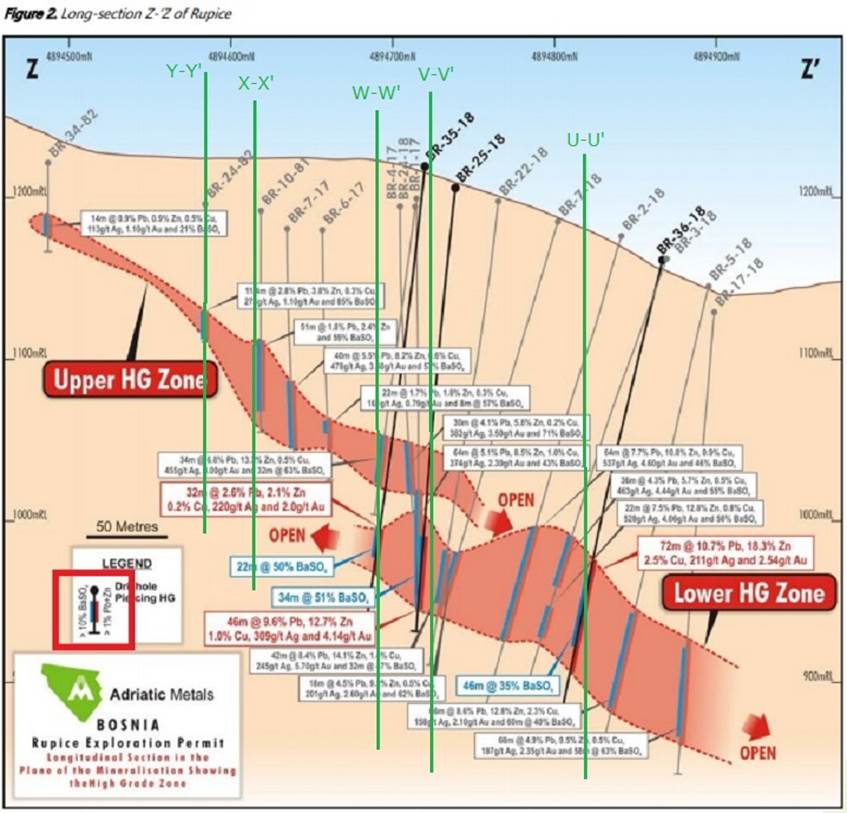

The sections will show that the mineralized intercepts get higher grade and thicker the deeper the mineralized envelope goes along strike. At the same time, the envelope is tilted, and the more near surface side (west side) of it is thinner and lower grade as well compared to the deeper side (east side). After intensive drilling around the mid-section, it appeared that there are two distinct high grade zones, the Upper HG Zone and the Lower HG Zone (projected cross sections in green):

Many of the older holes of the Upper HG Zone stopped right after the drill hit basement/non-mineralized rock, so Adriatic has to drill deeper below the Upper HG Zone to potentially establish an extension to the south (left in this section) of the Lower HG Zone. All eyes are, of course, on the Lower HG Zone at depth now, potentially extending further along strike to the north. When the Exploration permit is granted with a week or so, drilling will test this prime target.

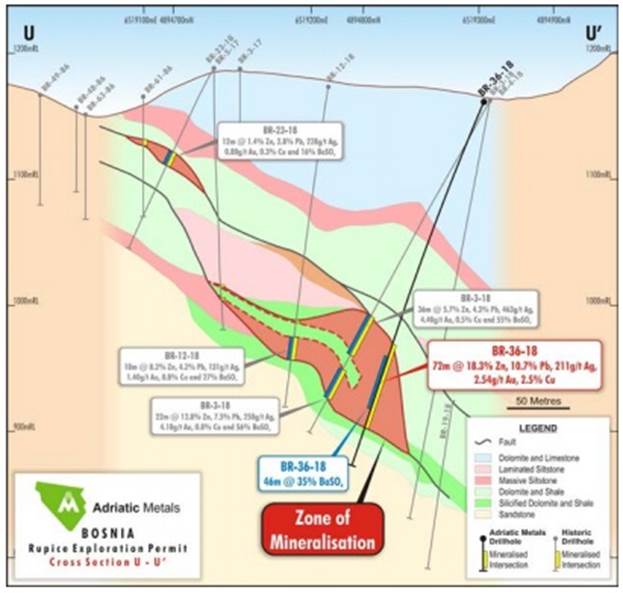

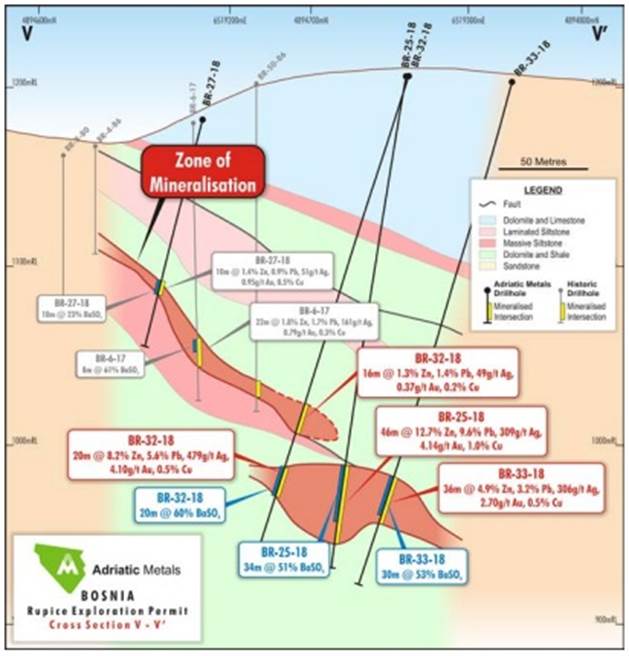

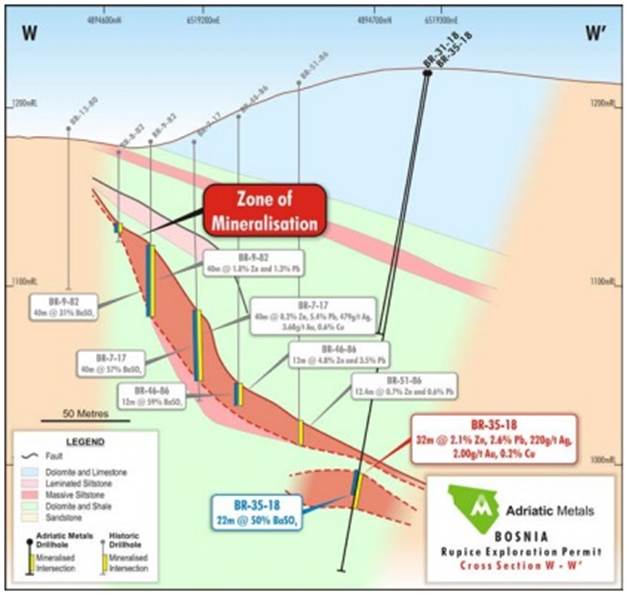

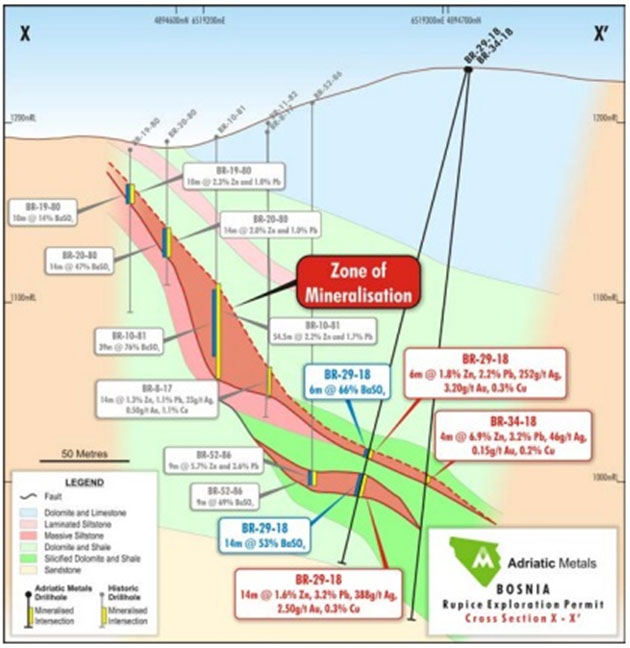

The following set of cross sections gives a good indication of the variable shapes of mineralization, and true width of many drill results:

<>

Cross section X-X’ is the one that I don’t exactly follow, as the long section doesn’t indicate this second, deeper located mineralized layer, but the long section probably stays west of it, close to hole BR-10-81, missing this layer in this section.

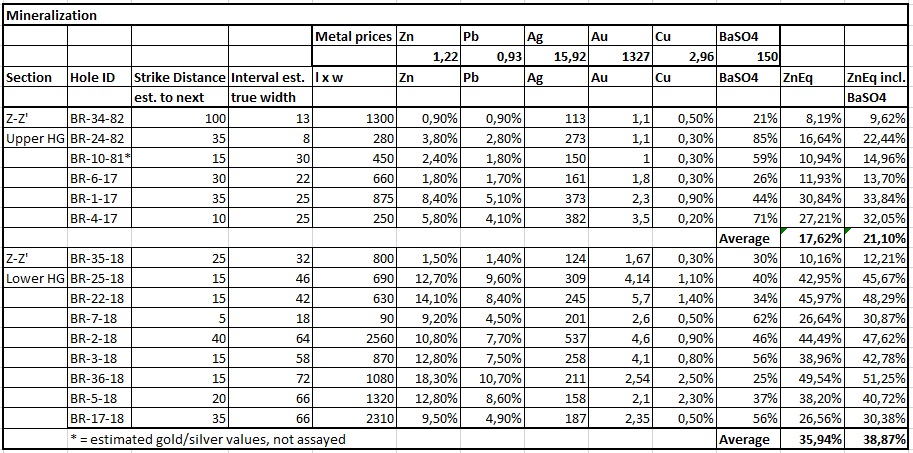

The mineralized envelopes vary a lot in size and shape, but the good news is they seem to be fairly continuous, as seems the long section. When sequencing the sections, it appears that the Upper and Lower HG Zone start out as one, then diverge into two separate zones, of which the Upper HG Zone seems to end close to cross section U-U’ and the Lower HG Zone seems to continue at the north. I am contemplating buying an affordable piece of geo software in order to assist me with estimating envelopes, but for now calculations by hand are my approach. I started with the long section, averaged grades, looked for true widths, and this is the kind of first table as a result:

This exercise was repeated for all cross sections as well, giving me something of a starting point to work with. Determining an average width and height of the envelopes in between the sections wasn’t easy as there is not enough data, and I couldn’t average too much on the grades as it should actually be a weighted average. Nevertheless, I estimated a conservative envelope for the Upper HG Zone of 0.45M m3, and 0.7M m3 for the Lower HG Zone, which, assuming a conservative average gravity of 3.6t/m3, leads us to 4.1Mt. I am not sure how much Adriatic is dealing with sedimentary host rock, which would bring down the barite (4.5t/m3) and sulphide gravity (3.6 to 4.4t/m3).

Some info on specific gravity (density) of host rock:

“Sulphide ore minerals have high densities that range generally from about 4.0 g/cm3 for sphalerite to 4.62 g/cm3 for pyrrhotite. Galena attains an exceptionally high value of 7.50 g/cm3. Associated minerals pyrite, magnetite and hematite have densities of 5.02, 5.18 and 5.26 g/cm3, respectively. A sample of densities of massive sulphides in the Bathurst camp, determined from measurements on drill core from several sites, indicates that they range from about 3.80 to 4.40 g/cm3. Those of semi-massive sulphides range from about 3.60 to 3.85 g/cm3. By comparison, a sample of density measurements made on fine-grained sedimentary and felsic volcanic host rocks indicates densities ranging generally from about 2.70 to 2.85 g/cm3.”

With the corporate tax in Bosnia Herzegovina standing at a very cheap 10%, and a potential operation dealing with small tonnage and thus low capex, there is no doubt in my mind that this could be a very profitable mine someday. If I would take a 4Mt resource for the entire mineralized envelope, conservative recoveries and payability, and using an average small-scale underground capex/tpd of US$80,000/tpd, the total capex would come in at US$90 million. Let’s use some margin of error, and take US$100 million and US$60/t opex. This would result in a hypothetical post-tax NPV8 of US$175 million and likely a very high post-tax IRR. This is all conservative, and considering the current market cap of about US$80 million and exploration ongoing there is a lot of upside.

4. Conclusion

By now it will hopefully be clear why I think Adriatic Metals is already a pretty interesting exploration story, with lots of further upside potentially in the making on its recently expanded licenses. If the maiden resource estimate, which is expected in Q2, 2019, can indeed get to 4Mt or more, hypothetical PEA economics might be spectacular. With a very low hypothetical capex this project will be easily fundable for a wide range of parties, and will probably attract more interest after the resource estimate comes out and metallurgy proves to be fine. It is one of the most exciting exploration stories around at the moment, far from nearing the end, and as a shareholder I keep tracking them at close range with extra interest. Have a look.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Disclaimer:

The author is not a registered investment advisor, and currently has a long position in Adriatic Metals. All facts are to be checked by the reader. For more information go to the websites of the mentioned companies and read the available company information and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor’s disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

( Companies Mentioned: ADT:ASX; 3FN:FSE,

)