Source: Michael Ballanger for Streetwise Reports 08/30/2018

Sector expert Michael Ballanger offers his investment thesis for this Colorado-based energy metals miner.

In June, I talked about a pending private placement being offered by Colorado-based Western Uranium Corp. (WUC:CSE; WSTRF:OTCQX) at $0.68 per unit (half-warrant at $1.15) and suggested that the deeply discounted market capitalization/pound of uranium/vanadium was being addressed by way of a joint venture with Australia-based Battery Metals Resources Ltd. (BMR).

I followed up with an e-mail two days later introducing BMR, which had just announced a $25 million initial public offering (IPO) with a concurrent $50 million secondary as a tagalong, with BMO Capital Markets as lead underwriter. These two e-mails were intended to provide a chance to either average down on the 2016 $1.70 funding or at the very least initiate new positions in the deal by way of the $0.68 unit, which was being raised as the share price cruised along in the $0.85-1.05 range during most of the marketing period.

Since then, the company has closed over $3.6 million and has completed a name change to Western Uranium and Vanadium Corp., and has released news regarding developments surrounding the 5 Mlb vanadium resource contained in the Sage Mine located in Colorado. WUC entered into a joint venture agreement with BMR pertaining to the exploitation of the Sage deposit, which was announced on June 6; it was this announcement that triggered my immediate interest in revisiting the opportunity after experiencing such dire disappointment in early 2017. The arrival of an Aussie group that knows mining and appears eager to advance and exploit the vanadium assets is a welcome development for WUC, and one that has resulted in my adding an additional chunk of stock to my portfolio. After participating in 2016 with a purchase of $1.70 unit deal, I have added triple the dollar amount in the most recent placement and now have an adjusted cost base of CA$0.80. With the stock at CA$1.55, a problematic situation has been rectified, with further developments on the very near horizon enhancing the near-term upside potential.

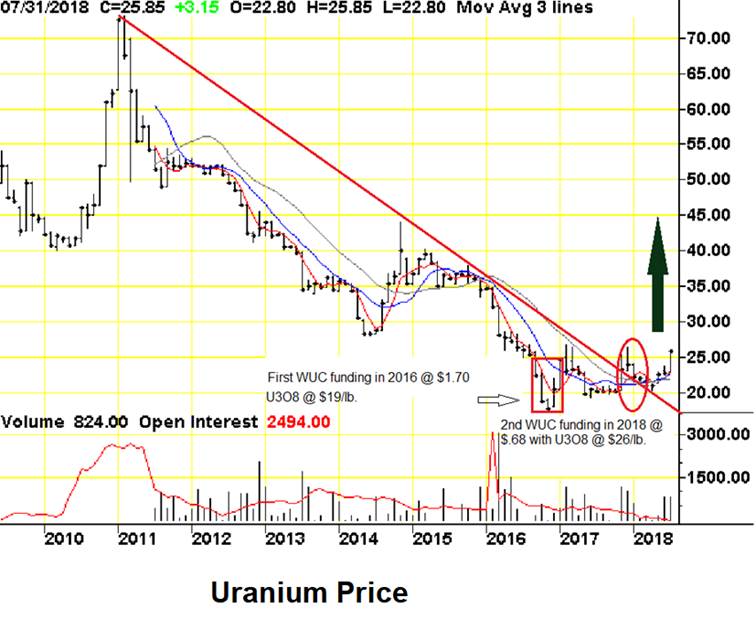

Technically, WUC has clawed its way back above the downtrend line from the $5.00 peak in 2015 and the $2.75 peak in 2017. RSI and MACD are in recovery mode and volumes are respectable.

Investing in uranium deals has been a nightmare since the late 2010 top, north of $75/lb, with all rallies being sold unmercifully and dips rarely advantaged. Rarely, if ever, treated as “green” energy, the U2O3 stocks have been treated like Japanese whaling ships at a Greenpeace convention. They are seen as “weaponry” by the masses, as opposed to the cleanest form of energy on the planet and one which has an extremely long shelf life. Vanadium stocks, by contrast, are beloved by the electric vehicle (EV) tribe, with many exploration issues having participated in the recent price advance.

Vanadium has been the superstar of the battery metals group, having outperformed lithium, cobalt and graphite since 2015. To understand the history of industrial applications for the metal, this link will take you to an excellent article from BBC World News.

Valuation

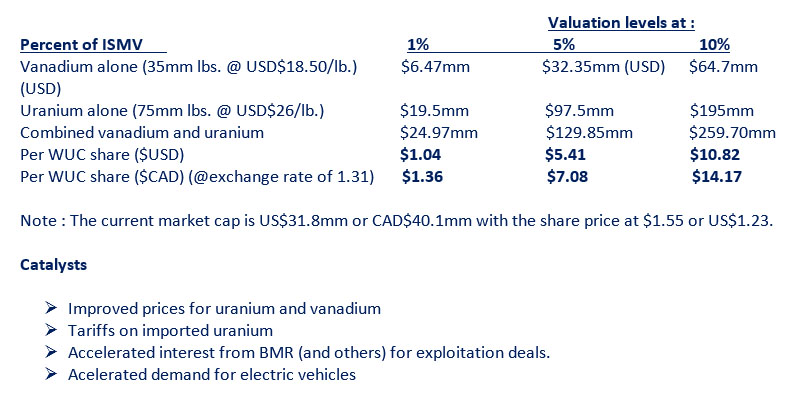

The company has four main properties, which are estimated to contain a total estimated resource of 75 million pounds of uranium. In addition, three of the four properties contain 35 million aggregate pounds of vanadium, with an implied value of US$647 million. At the current price of $1.55 per WUC share, the company carries a market capitalization of US$31.6 million, which represents 4.88% of the in situ metal value (ISMV) of the vanadium alone. Combining the in situ metal value of the 75 million pounds of uranium (@ US$26/lb) worth US$1.95 billion, you arrive at a combined (uranium and vanadium) in situ metal value of US$2.475 billion, such that Western Uranium is trading at 1.27% of the value of all historic resources.

The Opportunity

Most developers in the mining space will carry market caps in the 5-15% range depending on location (geopolitical and geographic).

Conclusion

When you view Western Uranium and Vanadium Corp. and attempt to conduct the normal-course due diligence so greatly required in today’s world, you are taken aback by the numbers I have provided above. How can a company with assets this good be completely ignored by investors? How can an investment story so compelling be so completely dismissed, from 2015 at CA$5.00 all the way to CA$0.66 in 2018? The answer lies in management. George Glasier is a friend of mine and one of the senior statesmen of the North American uranium industry. He can tell you more about the uranium space than any person I have met in all of my years in the resource business. However, George operates his business from a technical perspective, and that includes language the vast majority of investors do not exactly comprehend. In my discussions with George, I committed to assist him in the marketing of the WUC story so as to ensure the maximization of shareholder value by way of the clarification of exactly how what George does will, in due course, result in a higher share price. And that is what I am trying to do today. Pretty simple math.

In my 41 years in the investment industry, I learned by way of pain and suffering that many great investment opportunities arise from the ashes of the “resistance to promote” by the managers of projects that are technically sound but either “early” or “late,” and WUC is just one of those opportunities.

If, by chance, the vanadium story is a “late-to-the-party” facet of the WUC attraction, then the majorasset, uranium, will be the fallback position because of its unenviable role as a major bear market disaster story. If the uranium space suddenly ignites, then the aggregate package is going to be revalued in short order, and it is important that both assets are strategic assets in …read more

From:: The Energy Report